Category: News

Stablecoin Yields Won’t Harm Banks, White House Economists Say

Stablecoin Yields Won’t Harm Banks, White House Economists Say

Authored by Amin Haqshanas via CoinTelegraph.com,

A White House report found that banning yield on stablecoins would have a marginal impact on bank lending while creating clear economic downsides.

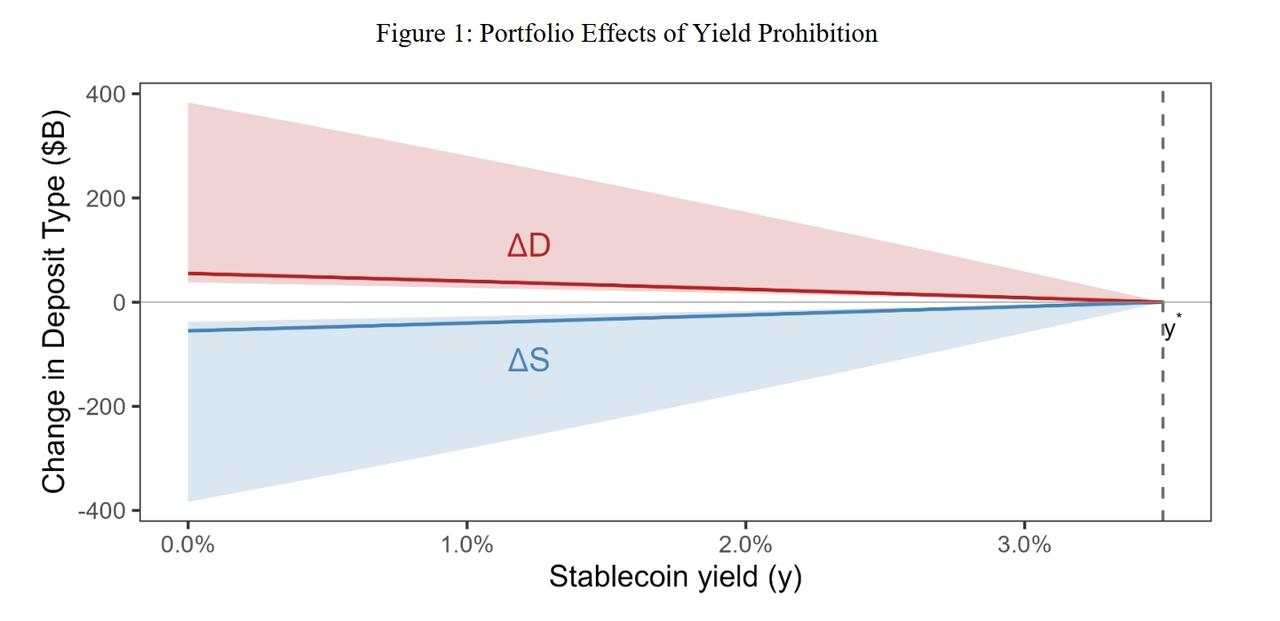

According to the Council of Economic Advisers, a three-member agency within the Executive Office of the President tasked to offer the president economic advice, moving funds from stablecoins back into bank deposits would not translate into significant new lending. Under its baseline scenario, total bank lending would increase by about $2.1 billion, roughly 0.02% of the $12 trillion loan market.

The report, published Wednesday, says that community banks would see even smaller gains. Lending at these institutions would increase by roughly $500 million, or about 0.026%.

The findings come amid an ongoing clash between banks and the crypto industry over stablecoin yields. Banking organizations, including the Independent Community Bankers of America, have warned that stablecoin yields could significantly reduce bank lending, while crypto groups have rejected the claim.

Stablecoin lending ban could cost $800 million per year

However, banning stablecoin rewards could carry a greater cost. The report estimates a net welfare loss of around $800 million per year, mainly because users would lose access to yield on stablecoins. The cost-benefit ratio is about 6.6, meaning the economic costs would far exceed any gains in lending.

“Producing lending effects in the hundreds of billions requires simultaneously assuming the stablecoin share sextuples, all reserves shift into segregated deposits, and the Federal Reserve abandons its ample-reserves framework,” the report concludes.

Portfolio effects of the yield ban. Source: White House

In July 2025, President Donald Trump signed the GENIUS Act into law. The law prohibits stablecoin issuers from paying interest or yield to holders, but third-party platforms (like exchanges) can still offer yield on stablecoins. The proposed Digital Asset Market Clarity Act could close that gap by clarifying whether yield should be restricted across the board or allowed under certain conditions.

CLARITY Act nearing Senate markup hearing

The US House of Representatives passed the CLARITY Act on July 17, 2025. In January, Senate Banking Committee Chair Tim Scott delayed a planned markup, which has yet to be rescheduled.

Last week, Coinbase chief legal officer Paul Grewal said the CLARITY Act could be nearing a markup hearing in the US Senate Banking Committee, with lawmakers close to agreement on key provisions. He noted that progress hinges on resolving disagreements over stablecoin yield.

Tyler Durden

Wed, 04/08/2026 – 15:45

https://www.zerohedge.com/crypto/stablecoin-yields-wont-harm-banks-white-house-economists-say

Mexico Truckers Block Key Freight Routes In Nationwide Strike

Mexico Truckers Block Key Freight Routes In Nationwide Strike

By Noi Mahoney of FreightWaves,

A nationwide strike by Mexican truckers and farmers blocked major highways and freight corridors across Mexico on Monday, disrupting access to Mexico City, industrial zones and several U.S.-Mexico border crossings.

The protest, organized by the National Association of Transporters (ANTAC) and the National Front for the Rescue of the Mexican Countryside (FNRCM), included road blockades in at least 20 states and began around 7 a.m. CST, with disruptions expected to last several hours or longer in some areas.

The groups say the strike is in response to rising cargo crime, high diesel and operating costs, deteriorating road infrastructure and a lack of progress on agreements with the federal government related to highway security and extortion.

Major freight corridors affected

According to Mexican media reports, blockades were reported on several of Mexico’s most important freight routes, including:

Mexico–Querétaro

Mexico–Puebla

Mexico–Pachuca

Mexico–Cuernavaca

Federal Highway 45 in the Bajío region

Culiacán–Mazatlán corridor

Guadalajara–Colima and Mexico–Guadalajara routes

Access roads to Mexico City

Border crossings in Ciudad Juárez, Tijuana and Mexicali

These corridors connect Mexico’s manufacturing hubs, ports and border crossings, making them critical for domestic distribution and cross-border trade.

The strike is affecting access to industrial corridors, customs facilities and toll roads, similar to protests in November 2025 that disrupted more than 40 highways and access to industrial zones and customs facilities.

Security and costs drive protests

Transport and agricultural groups say insecurity remains one of the biggest issues facing freight operators in Mexico.

Official government data shows 6,263 investigations into cargo truck robberies were opened in 2025, but industry groups estimate the true number of cargo theft incidents — including unreported cases — exceeded 16,000, with losses topping 7 billion pesos annually.

Protesters are demanding:

Increased National Guard presence on highways

Action against extortion and corruption at checkpoints

Lower operating costs, including diesel

Support programs and policy changes for agricultural producers

Farmers joining the strike say insecurity, high fuel costs and agricultural pricing pressures are hurting rural producers and transport operators alike.

Government pushes back

Mexico’s Interior Ministry said the government has held multiple meetings with transport and agricultural groups and has provided billions of pesos in support to farmers, arguing there is “no reason” for the protests and warning that blockades affect third parties and the broader economy, according to Omnia.

Still, organizers say the strike could continue if no agreements are reached, raising the risk of ongoing disruptions to supply chains and freight movement across Mexico.

Tyler Durden

Wed, 04/08/2026 – 15:05

https://www.zerohedge.com/economics/mexico-truckers-block-key-freight-routes-nationwide-strike

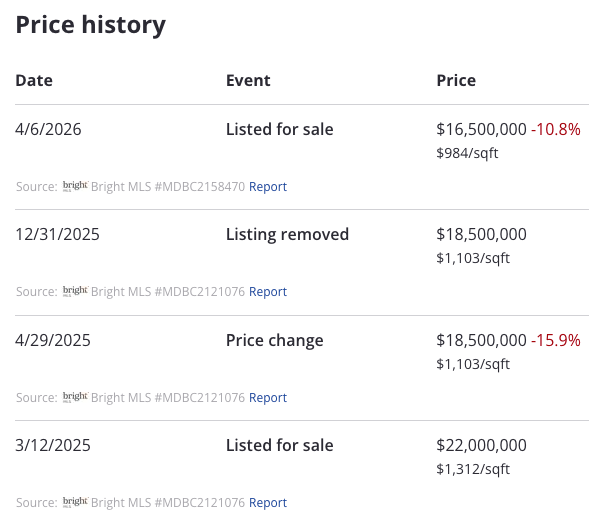

Kevin Plank’s Unsellable Thoroughbred Race Farm Sees Another Deep Price Cut

Kevin Plank’s Unsellable Thoroughbred Race Farm Sees Another Deep Price Cut

Under Armour CEO Kevin Plank has once again cut the asking price on his massive thoroughbred racing farm in northern Baltimore County, Maryland, as the historic farm – once owned by the Vanderbilt family – continues to sit on the market amid a series of deep price cuts.

Plank has been winding down his sprawling real estate portfolio, offloading everything from multiple residential properties to a luxury hotel in Baltimore City in recent years. Among his crown jewels – alongside the Baltimore Peninsula – is Sagamore Farm, a 404-acre thoroughbred racing operation he has been trying to sell for years.

The latest data from multiple listing service provider MLS Bright shows that Plank likely instructed his listing agent, Christina Giffin of Monument Sotheby’s International Realty, to pursue another price cut.

MLS Bright data shows Sagamore’s current listing price is around $16.5 million. This represents a 15% cut from the late-2025 listing of $18.5 million and an overall decline of about 25% from the original $22 million listing in March 2025. The farm appears to have been on and off the market.

We’ve outlined the mounting challenges for Plank as UA’s brand momentum trended downward for years, but only in recent quarters have we begun focusing on UBS analyst Jay Sole, who is attempting to call a bottom in the stock. Also, the “Warren Buffett of Canada” piled into the stock earlier this year as management raised its outlook.

Plank is still dealing with the “ghost town” of Baltimore Peninsula amid the city’s declining population, which has fallen to a 100-year low under the far-left leadership of Mayor Brandon Scott. Statewide, Maryland’s financial profile is deteriorating under left-wing Governor Wes Moore, with high taxes, crime, a growing fiscal deficit, rising power bills, prioritizing all things woke, significant outbound migration, and other mounting challenges. This is what you get under one-party Democratic rule of kings and queens that have ignited a fire in the state and city under backfiring DEI policies.

Plank should focus on advocating for political change in Baltimore City. At least one other billionaire is already involved in such efforts. If Plank wants his “city within a city” to thrive, negative net migration trends must reverse, and both the city and the state will need to improve their overall financial profiles. Certaintly Democrats show zero interest in fostering a thriving state.

Tyler Durden

Wed, 04/08/2026 – 14:45

FOMC Minutes Signal Fed Saw “Dual Sided” Risks From Iran War

FOMC Minutes Signal Fed Saw “Dual Sided” Risks From Iran War

Since the last FOMC meeting (March 18th), a lot has happened (war, more war, and now less war), and rate-change expectations hawkishly surged, then dovishly normalized today…

And given the last 24 hours, perhaps this information is more useful now, as we return to macro-fundamentals from geopolitical chaos running markets.

The minutes, released three weeks after the meeting, underscore the Fed’s dilemma as it seeks to fill its congressional mandates of low inflation and maximum employment.

Fed officials wrestled with starkly differing scenarios for the US economy following the outbreak of the Iran war, including one that called for interest-rate cuts and another that would require raising rates.

Key Highlights (via Bloomberg):

*FED: MOST SAID PROTRACTED WAR COULD HIT JOBS, WARRANT CUTS

*FED: SOME SAW `STRONG CASE’ FOR TWO-SIDED LANGUAGE ON RATE PATH

*FED: TARIFF EFFECTS ON GOODS PRICES HAD BECOME MORE UNCERTAIN

*FED: MANY SAID INFLATION HIGHER FOR LONGER COULD CALL FOR HIKES

*FED: VAST MAJORITY SAID INFLATION PROGRESS COULD BE SLOWER

*FED: VAST MAJORITY SAW EMPLOYMENT RISKS AS SKEWED TO DOWNSIDE

*MOST JUDGED RECENT DATA SHOWED LABOR `BROADLY IN BALANCE’

Minutes of the meeting showed most officials worried the war could hurt the labor market and warrant lower interest rates.

Fed officials acknowledged that the Iran conflict could also force households to cut back spending to offset higher gas prices, which would slow growth and raise unemployment.

At the same time, many policymakers highlighted the risk to inflation that might ultimately warrant rate increases.

“Partly as a result of these factors, the vast majority of participants noted that progress toward the Committee’s 2 percent objective could be slower than previously expected,” according to the minutes.

The record of the meeting also showed that a growing number of officials urged their colleagues to consider language in the committee’s statement raising the scenario of hiking interest rates under certain conditions.

“Some participants judged that there was a strong case for a two-sided description of the committee’s future interest-rate decisions in the post-meeting statement, reflecting the possibility that upward adjustments to the target range for the federal funds rate could be appropriate if inflation were to remain at above-target levels,” the minutes said.

As a reminder, The Fed kept its key rate unchanged at about 3.6% with Powell saying that another reduction depended on underlying inflation cooling steadily this year:

“If we don’t see that progress then you won’t see the rate cut,” he said then.

Will the ceasefire slow inflation or is the damage already done and yet to flow through global supply chains?

Read the full Minutes below:

Tyler Durden

Wed, 04/08/2026 – 14:10

https://www.zerohedge.com/markets/fomc-minutes-signal-fed-saw-dual-sided-risks-iran-war

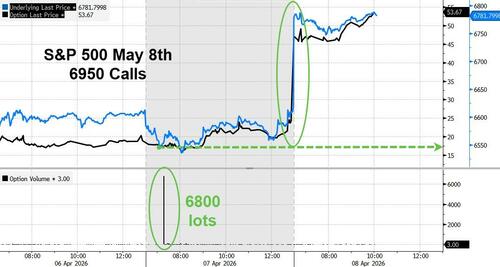

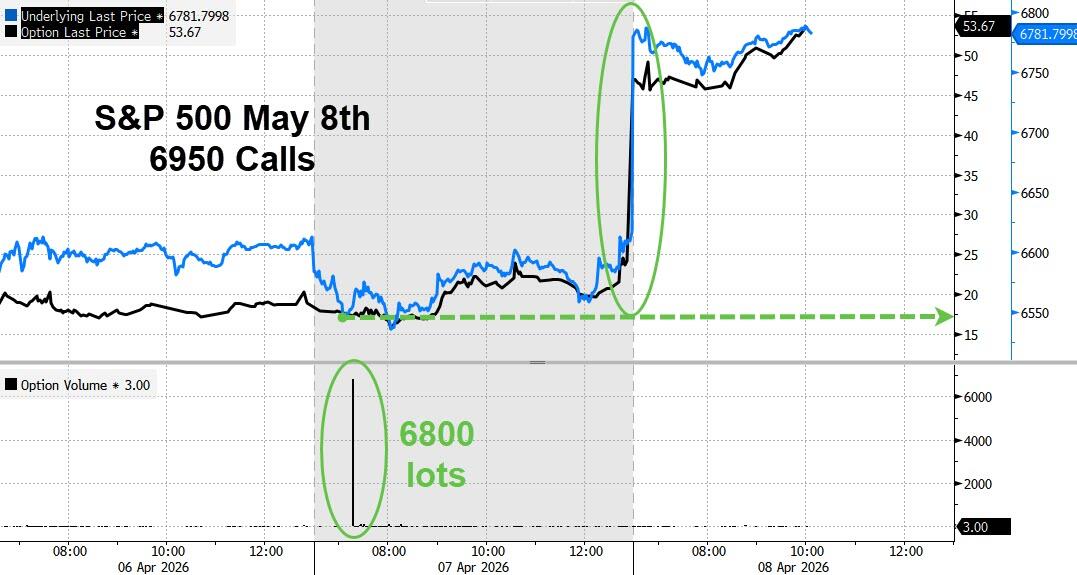

Trader Makes $23 Million In One Day With Massive S&P Call Purchase Hours Before Ceasefire

Trader Makes $23 Million In One Day With Massive S&P Call Purchase Hours Before Ceasefire

A trader who made a large bet on a stocks rocketing in the coming weeks is up about $23 million in paper profit today, according to Bloomberg.

The unknown trader spent $12 million premium on 6800 lots of 6950 S&P 500 Index Options (SPX) calls for May 8 expiry, when the index was at 6556.21; the trade was executed around 10:20 a.m. Eastern on Tuesday, just hours before Trump’s announcement of a 2-week ceasefire which sent stocks soaring.

The trade was an “example of upside chasing on hopes of an imminent peace deal”, said Chris Murphy, co-head of derivatives intelligence, in an email Tuesday.

Following the ceasefire deal last night, stocks surged, with the long SPX 6950 position now trading at $50, Bloomberg pricing data indicates.

That makes the position worth $35 million as of noon on April 8, with the S&P 500 at 6773, or a $23 million profit net of the premium paid.

Tyler Durden

Wed, 04/08/2026 – 14:00

The Apple AI Strategy: Discipline Over Hype

The Apple AI Strategy: Discipline Over Hype

Authored by Michael Lebowtiz via RealInvestmentAdvice.com,

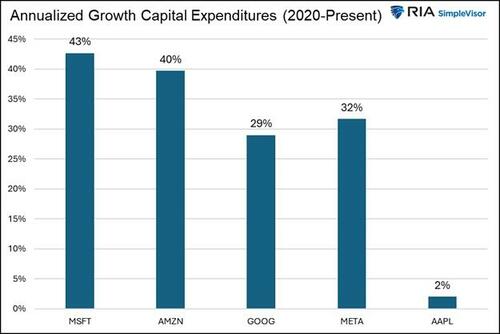

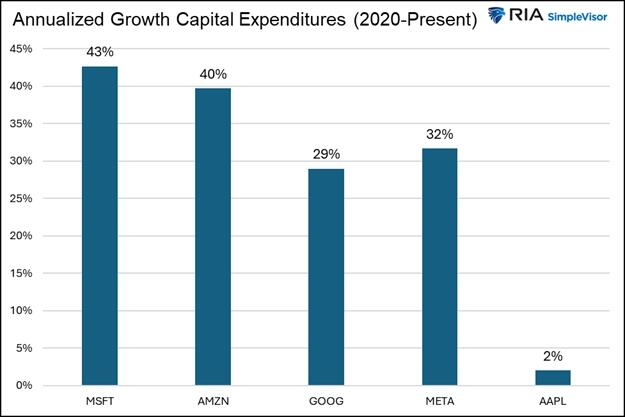

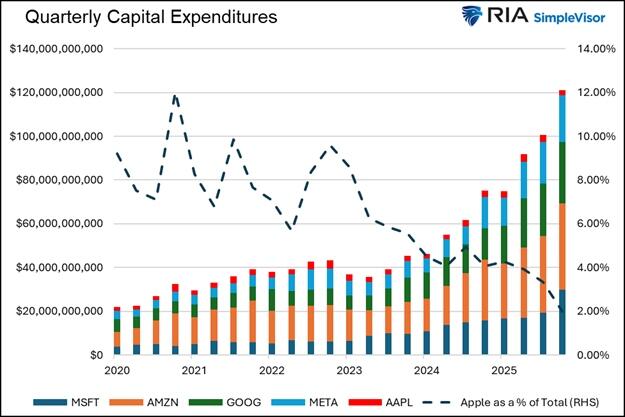

While tech giants invest billions in AI, Apple executives are quietly sitting on their hands and a mountain of cash. Given the massive growth in AI investments, as shown in the graphs below, executives of leading companies at the forefront of AI development must be ecstatic about the prospect of AI significantly boosting their bottom lines.

The puzzling question, however, is why Apple isn’t following suit. Or could they be taking a different approach to winning the AI arms race?

Apple Avoids The AI Spending Boom

Apple is one of the world’s most profitable companies. Over the last four quarters, they reported over $400 billion in annual revenue and nearly $100 billion of free cash flow. Furthermore, the company holds $65 billion in cash and cash equivalents and $77 billion in marketable securities. The bottom line is that Apple can easily self-fund AI innovation on a massive scale, as its competitors are doing. Yet it hasn’t.

Rather than mimicking its peers, Apple appears content to let the AI landscape mature before committing significant capital. Restraint may seem like complacency or even negligence. However, Apple has a long and extremely successful history of deploying capital at the right time; when the profit outlook is clear, the technology is established, and the customer value proposition is well-defined.

This approach may be frustrating for Apple shareholders in the short term, but history and the chart below, comparing Apple to the S&P 500, suggest it has served them extremely well.

Apple’s Historical Playbook

Apple has rarely been first to introduce a new product. It was not the first personal computer company, the first smartphone maker, or the first to launch wireless earbuds, smartwatches, or VR headsets. In nearly every case, Apple waited while other companies experimented and helped define the product and the market.

Apple waited to understand what consumers wanted in a product. Only after the uses of a new product became obvious and consumer demand was proven did Apple step in with well-designed products that emphasized reliability, usability, and profitability. Their goal has always been not to be the biggest producer of a product but to be the best. In most cases, they have lived up to that lofty goal.

The timeline below shows the various smartphones that preceded Apple’s iPhone. Given the smartphone landscape today and the fate of the products that preceded the iPhone, it’s fair to say that Apple’s patience was well rewarded.

Discipline May Win The AI Game

Today’s generative AI ecosystem is still in its experimental phase. Training costs are enormous, inference costs remain high, and business models are largely unproven. Many AI products may be impressive, but have produced limited revenue.

Instead of competing with the likes of Microsoft, Meta, and Google, Apple appears to be integrating AI incrementally. They are embedding AI into existing hardware, operating systems, and services rather than creating standalone, capital-intensive platforms. This allows its products to stay competitive without fundamentally altering its cost structure.

This approach takes Apple out of the AI limelight, which has at times weighed on the stock price.

Waiting For Clarity

There are good reasons to wait for AI to better define itself before Apple spends hundreds of billions on strategies that may not prove profitable. For example:

Monetization: While AI can clearly improve productivity and user engagement, it remains unclear how much consumers are willing to pay for it directly.

Legal/regulatory: Data privacy, intellectual property disputes, model accountability, and regulatory limitations are evolving areas of law and public policy. Apple, whose brand is closely tied to trust and privacy, could lose more than most companies from missteps in these areas.

Capital flexibility: By not locking itself into massive investments today, Apple retains the capital flexibility to invest rapidly once AI technology better defines itself and the economics become more apparent.

The Long View

For the impatient investor or trader, Apple’s approach probably feels underwhelming, especially amongst the daily headlines proclaiming AI innovation and trillion-dollar opportunities. But, for investors with patience, history suggests that Apple’s greatest successes have come not from being first, but from entering markets when technology, consumer readiness, and profitability align.

In our article, AI Bubble: History Says Caution Is Warranted, we discussed how many game-changing innovations, such as AI, are often accompanied by a financial bubble. Furthermore, for understanding Apple’s AI strategy, it has historically been far from certain that the front-runners, initially touted as the biggest beneficiaries of the innovation, will be the long-term winners. To wit:

In 1999, few, if any, investors had ever heard of Google. The term for an internet search, “Googling,” was not yet a thing. Today, Google has a 90+% share of the search engine volume, and many of its early competitors no longer exist.

Might Apple be taking a page out of Google’s playbook and waiting in the weeds for the AI industry to mature?

Might Apple be the next Google?

Summary

In the early stages of a technology buildout, infrastructure tends to capture the most value. This time appears similar, with the chipmaker Nvidia posting extraordinary returns and investors fawning over the big data center players like Microsoft, Amazon, Meta, and Google. However, over time, value typically migrates toward the technology’s application. Understanding where we are in that migration from infrastructure to application is important.

In our opening section, we asked if Apple executives share the same enthusiasm for AI as their chief competitors. The answer may be that Apple executives understand something their peers do not; the race rarely goes to whoever is first out of the gate.

Tyler Durden

Wed, 04/08/2026 – 13:40

https://www.zerohedge.com/ai/apple-ai-strategy-discipline-over-hype

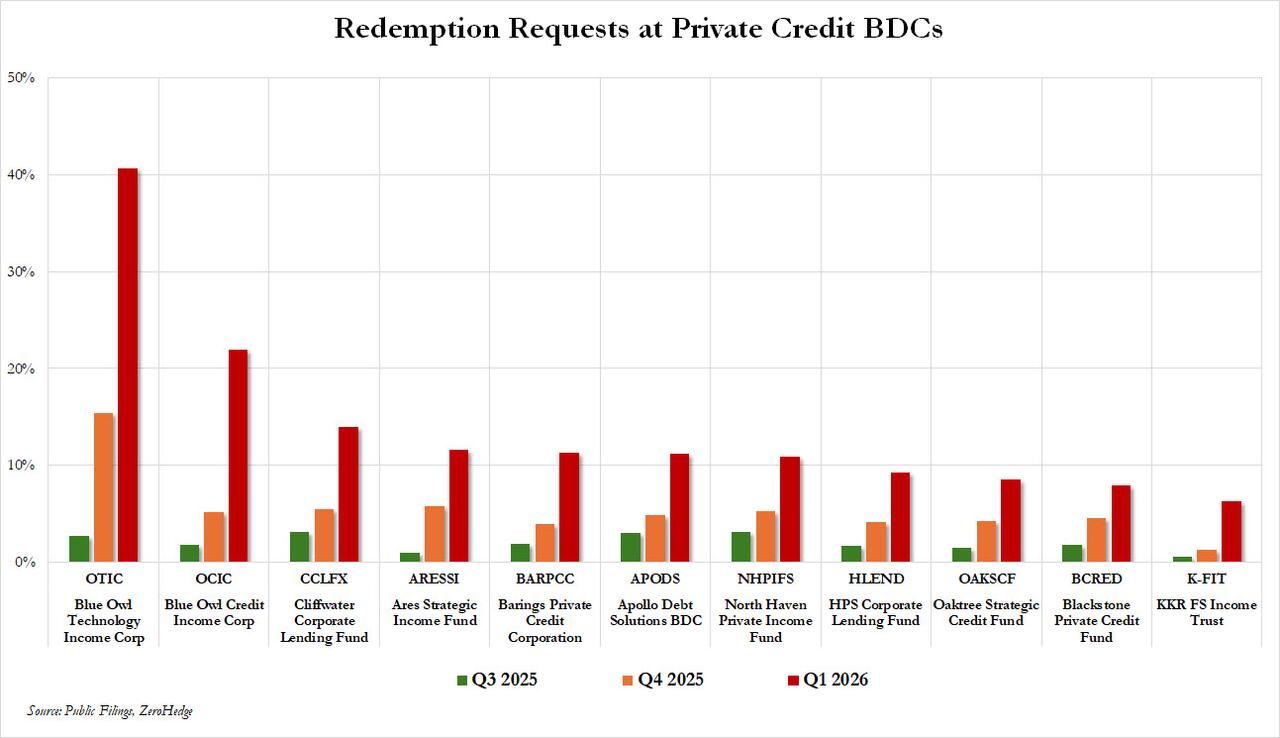

Blue Owl Stock Slides After Moody’s Cuts Outlook To “Negative” On Surging Redemption Requests

Blue Owl Stock Slides After Moody’s Cuts Outlook To “Negative” On Surging Redemption Requests

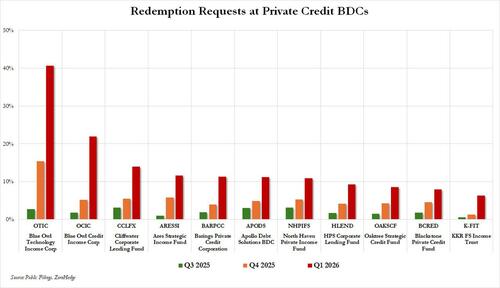

Blue Owl stocks is getting slammed this morning, erasing all early gains, after Moody’s Ratings cut its outlook on a $36-billion Blue Owl non-traded fund to “negative” from “stable” on Tuesday, citing redemption requests that were significantly higher than at peers in the first quarter. Moody’s also said the change in the outlook on Blue Owl Credit Income Corp (OCIC) is due to the majority of the redemption requests coming from a very limited number of investors, revealing some concentration in the equity-holder base.

The downgrade highlights the mounting strains in the $2 trillion private credit industry after a strong run, as jittery retail investors bail out amid rising concerns around transparency, lending standards and valuations.

As we noted recently, having started the firesale in the private credit in February, the decision has since backfired on Blue Owl, leading to an unprecedented surge in redemptions, which hit a record 40.7% for the Blue Owl Technology Income Corp, and 22% for the Blue Owl Credit Income Corp.

In response, OCIC, Blue Owl’s biggest business development company (BDC), had said about 90% of the investors did not request to redeem in the first quarter, which, however, is precisely one of the main concerns for Moody’s which cautioned about concentration risk. OCIC investors sought to redeem 21.9% of shares in the first quarter, significantly higher than the 5.2% redemption requests received in the fourth quarter.

Moody’s said it expects elevated redemptions to persist in the coming quarters and inflows could slow further, resulting in the dissipation of OCIC’s currently strong capital and liquidity positions.

Blue Owl has previously said there was a “meaningful disconnect” between public sentiment on private credit funds and the underlying performance of its portfolio, although as we explained previously, the company may be simply delaying the inevitable asset remarking as a mere 20% drop in underlying asset values would breach key regulatory ratios.

Earlier on Tuesday, Moody’s had revised its outlook on US all BDCs to “negative” from “stable”, citing rising redemption pressures, higher leverage and weakening access to funding markets.

Non-traded perpetual BDCs, like OCIC, have grown rapidly in the past few years as alternative asset managers aggressively expanded in the wealth channel and focused on retail and high-net-worth investors, who are increasingly buying private assets.

But retail investors tend to be less patient and predictable compared to institutional investors during periods of volatility.

Such investment vehicles offer lower volatility compared to publicly traded BDCs, but investors have to contend with lower liquidity.

As we have repeatedly discussed, Blue Owl has become the poster child for private credit funds that are struggling with an elevated level of redemptions. Its stock has more than halved over the past 12 months and is trading near record low, and on Wednesday it reversed all early gains and was trading down 1%, if still above its record lows hit last week.

Its handling of some of its private credit funds in recent months also attracted intense scrutiny and raised concerns about liquidity for such vehicles.

Blue Owl had last year planned to merge its publicly traded fund Blue Owl Capital Corp with a non-public fund called Blue Owl Capital Corp II, but called off the deal after a plan to freeze withdrawals ahead of the transaction rattled investors.

The firm earlier this year replaced quarterly redemptions at OBDC II with promised payouts. It also sold $1.4 billion in assets from three of its credit funds to a consortium of investors which included an affiliated insurer, to return capital to investors and pay down debt. Concerns promptly emerged that the less than “arms length” transaction had cherry picked the best assets, leaving investors stuck with underperforming software exposure.

OBDC II is a finite-life non-traded BDC and the fund was due to give a full liquidity event to investors within three-to-four years of the completion of its public offering, which runs through 2026.

Last month, S&P Global revised the outlook on Cliffwater’s $33 billion flagship private credit fund to “negative” over higher investor redemption requests.

Tyler Durden

Wed, 04/08/2026 – 13:25

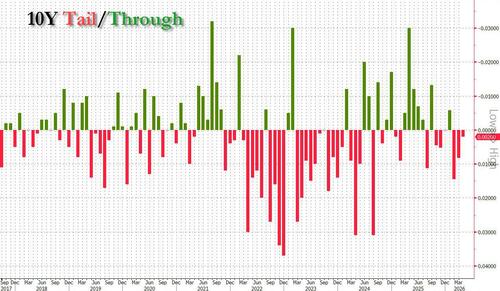

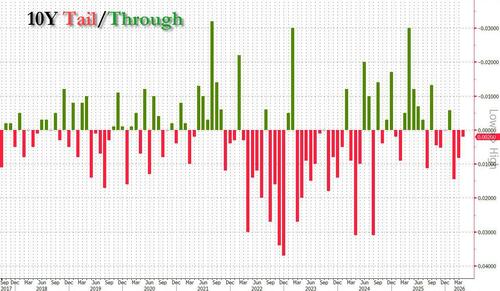

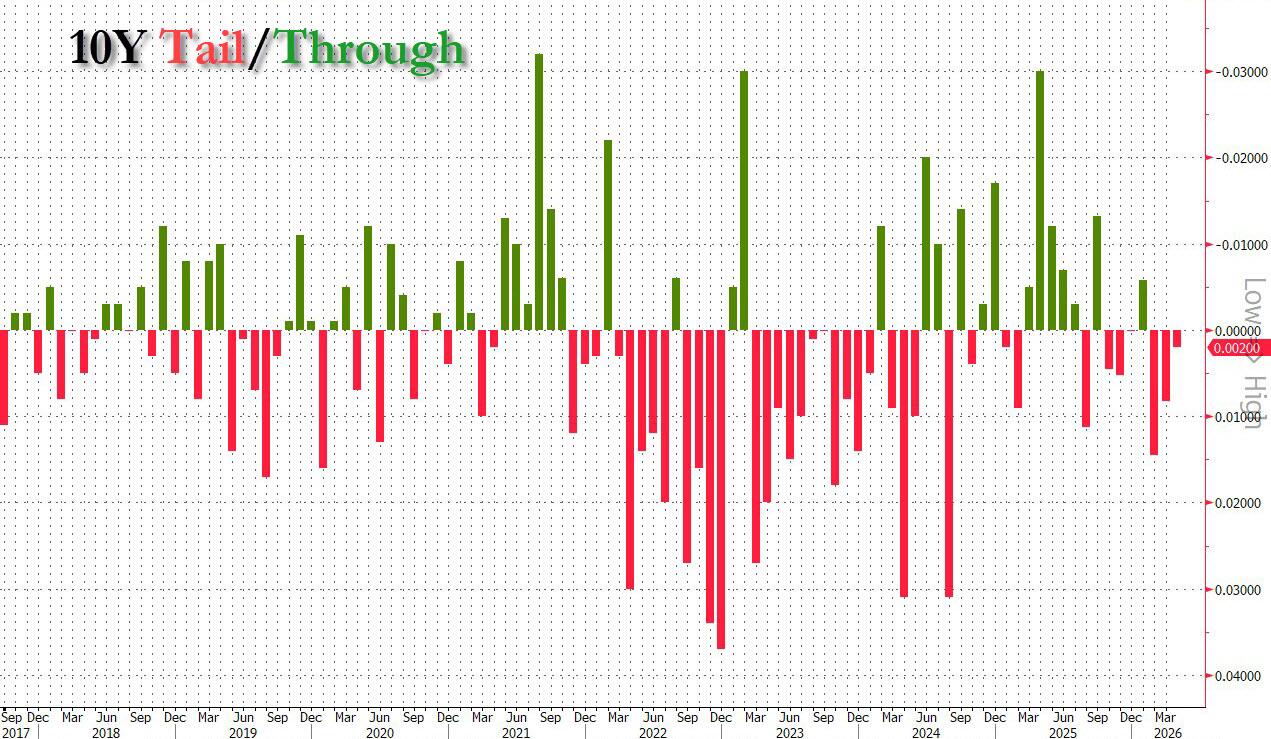

10Y Auction Tails As Foreign Demand Dips

10Y Auction Tails As Foreign Demand Dips

After yesterday’s impressive 3Y auction, moments ago the Treasury sold $39 billion in benchmark, 10Y paper, in what was a mediocre auction.

The auction, a 9-Year 10-Month reopening of cusip CPX8, stopped at a high yield of 4.282%, up from 4.217% last month and the highest since last August. It also tailed the When Issued 4.280% by 0.2bps, the third consecutive tail in a row.

The bid to cover dipped to 2.429 from 2.449, and was also below the six-auction average of 2.48.

The internals also disappointed, as foreign demand slumped from March with Indirects awarded 65.32%, down from 74.45%, and below the recent average of 68.78%. Directs offset much of this drop, rising to 23.88%, almost double the 12.83% in March and the highest since January. Dealers were left holding 10.8%, down from 12.7% the previous month, but in line with the average of 10.05%.

Overall this was a slightly subpar auction, especially after yesterday’s stellar 3Y auction, but in light of the bid drop in yields across the curve and the lack of concession, it priced roughly where it should have and the market has barely reacted as one would expect.

Tyler Durden

Wed, 04/08/2026 – 13:16

https://www.zerohedge.com/markets/10y-auction-tails-foreign-demand-dips

10Y Auction Tails As Foreign Demand Dips

10Y Auction Tails As Foreign Demand Dips

After yesterday’s impressive 3Y auction, moments ago the Treasury sold $39 billion in benchmark, 10Y paper, in what was a mediocre auction.

The auction, a 9-Year 10-Month reopening of cusip CPX8, stopped at a high yield of 4.282%, up from 4.217% last month and the highest since last August. It also tailed the When Issued 4.280% by 0.2bps, the third consecutive tail in a row.

The bid to cover dipped to 2.429 from 2.449, and was also below the six-auction average of 2.48.

The internals also disappointed, as foreign demand slumped from March with Indirects awarded 65.32%, down from 74.45%, and below the recent average of 68.78%. Directs offset much of this drop, rising to 23.88%, almost double the 12.83% in March and the highest since January. Dealers were left holding 10.8%, down from 12.7% the previous month, but in line with the average of 10.05%.

Overall this was a slightly subpar auction, especially after yesterday’s stellar 3Y auction, but in light of the bid drop in yields across the curve and the lack of concession, it priced roughly where it should have and the market has barely reacted as one would expect.

Tyler Durden

Wed, 04/08/2026 – 13:16

https://www.zerohedge.com/markets/10y-auction-tails-foreign-demand-dips

Watch Live: White House Addresses Fragile Iran Truce

Watch Live: White House Addresses Fragile Iran Truce

All eyes are on the very shaky Iran ceasefire, at a moment Tehran is already threatening to pull out due to heavy Israeli attacks on Lebanon. Iran says it has again halted Hormuz oil transit, and there’s much that’s still up in the air and uncertain. The briefing with press secretary Karoline Leavitt is expected to begin at 1300ET:

Washington and Tehran have just entered a two-week ceasefire, brokered by Pakistani mediation, aimed at negotiating a broader settlement following over a month of brutal conflict which has chiefly focused on an air war. Will it stick?

Both sides are readying for direct, face-to-face talks in Islamabad. Trump has previewed that Kushner, Witkoff, and maybe even Vice President J.D. Vance will be there. Trump has said these will happen “very soon”. He told the NY Post on Wednesday:

“We’ll have Steve Witkoff, Jared Kushner, JD — maybe JD, I don’t know,” Mr. Trump told the New York Post over the phone. “There’s a question of safety, security.”

One question is whether the two sides see eye to eye on the initial ‘agreed upon’ ten points. Even the basis for the current ceasefire has come under scrutiny and possible disagreement.

Earlier Wednesday morning, the NY Times stated:

A White House official says that the 10-point peace plan that Iran publicly released on Wednesday differs from the plan that Trump said was a “workable basis on which to negotiate.” The official declined to elaborate on the differences but said Karoline Leavitt, the White House press secretary, was expected to clarify at a 1 p.m. briefing.

Leavitt is expected to address this pressing issue during the briefing, which promises to be a lively exchange with reporters.

Tyler Durden

Wed, 04/08/2026 – 13:00

https://www.zerohedge.com/political/watch-live-white-house-addresses-fragile-iran-truce

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}