Category: News

Futures Rise For First Time In 4 Days As Oil Rebounds From 4 Year Low

Futures Rise For First Time In 4 Days As Oil Rebounds From 4 Year Low

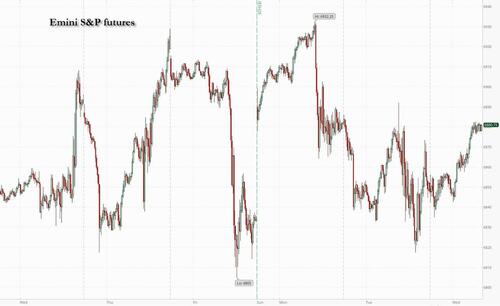

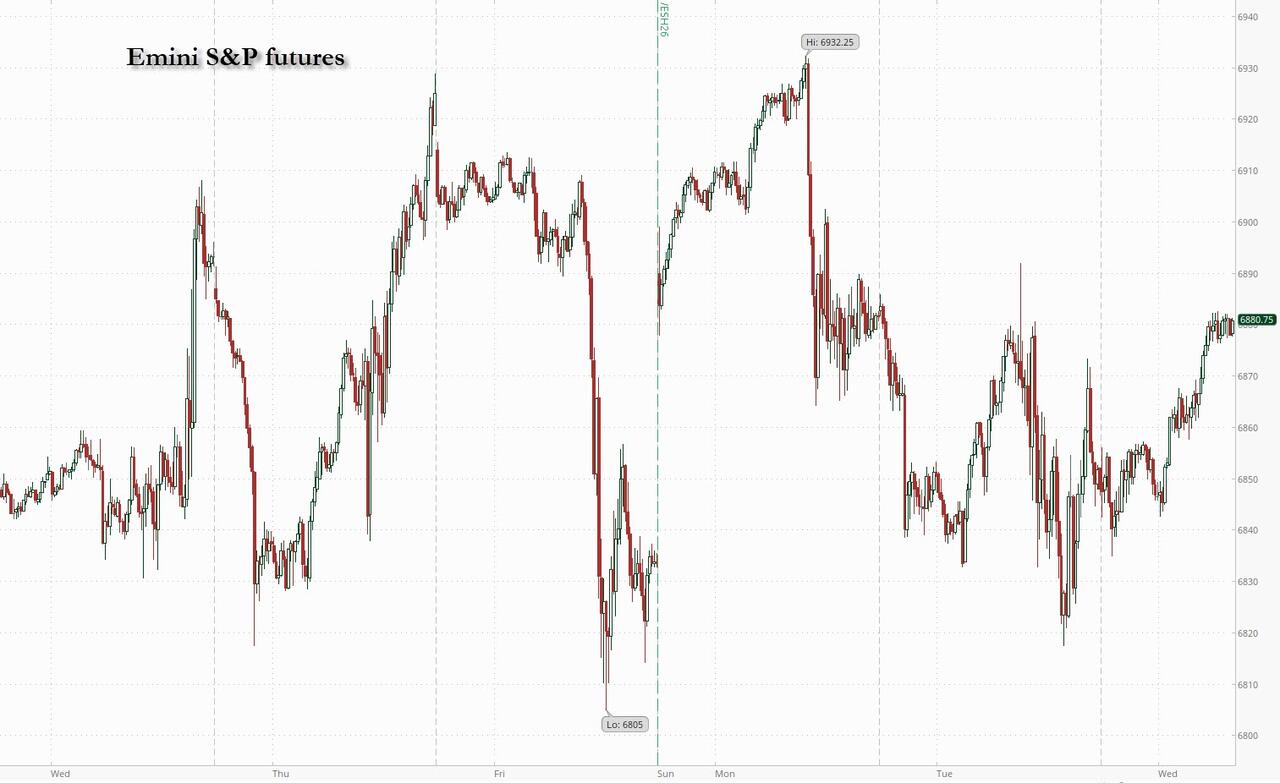

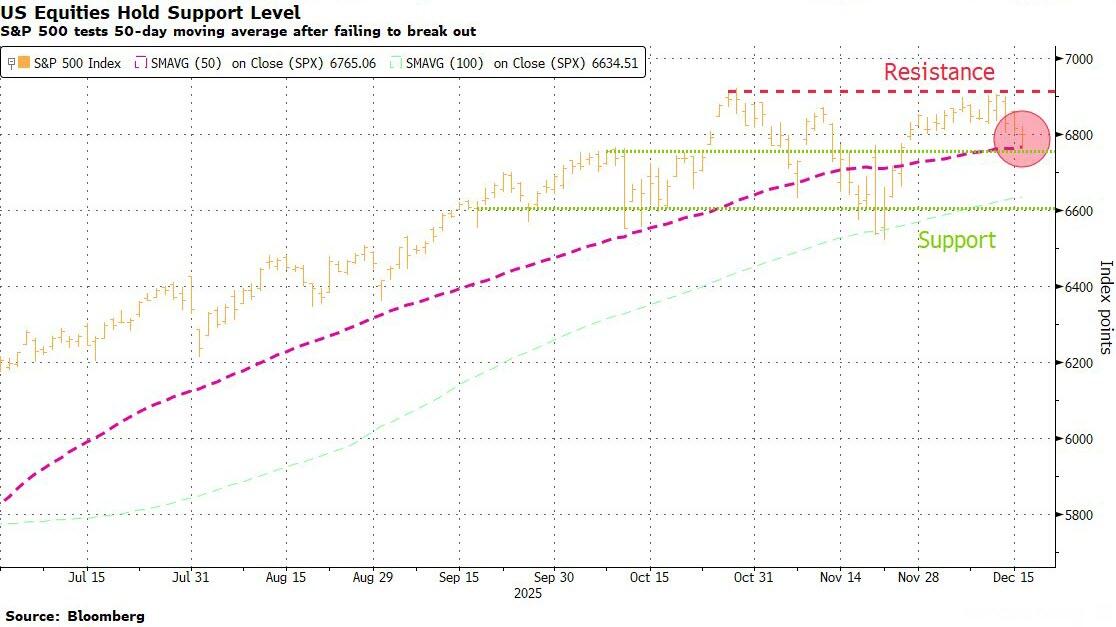

Stock futures are higher but with less than 10 full trading days left in the year, the Santa rally seems increasingly elusive, with traders struggling to find catalysts. The S&P 500 tested a key technical level on Tuesday, coming close to breaking below its 50-DMA. As of 7:15am ET, S&P 500 futures rose 0.3%, pointing to the first increase in four days for the S&P 500 as investor appetite returned after last week’s tech retreat; Nasdaq contracts +0.4%: Netflix rose 1.7% in premarket trading on bets it will prevail in its bid for Warner Bros. Discovery.Amazon rose 2% on report OpenAI is in initial discussions to raise at least $10 billion from Amazon and use its chips. Trading volumes are still relatively high, though will inevitably start to tail off as Christmas approaches. The main action today is in oil, with Brent prices bouncing 2.2% from a four year low back over $60, after Trump ordered a blockade of sanctioned tankers going into and leaving Venezuela, while the US is once again considering sanctions on Russia if Putin rejects the proposed Ukraine peace deal. Gold also jumped. 10Y treasury yields rose 3bps to 4.18% and the dollar index was at session highs. US economic calendar blank for the session. Fed speaker slate includes Waller (8:15am), Williams (9:05am) and Bostic (12:30pm)

In premarket trading, Mag 7 stocks are mostly higher: Amazon +1.9% as OpenAI is in initial discussions to raise at least $10 billion from Amazon and use its chips (Tesla +0.3%, Meta +0.3%, Alphabet +0.3%, Microsoft +0.2%, Apple +0.2%, Nvidia +0.1%)

Avantor (AVTR) slips 3% after Jefferies cut the life-sciences firm to underperform — a sell equivalent — from hold, citing structural headwinds with “no easy fix.”

Children’s Place (PLCE) slides 32% after the kids apparel retailer posted third quarter sales that fell 13% from the year-earlier period.

Frontier Group Holdings (ULCC) climbs 7% as the company is in merger discussions with Bankrupt Spirit Aviation Holdings Inc., according to people familiar with the matter.

Hut 8 (HUT) surges 21% after the Bitcoin miner and data center operator signed a 15-year, $7 billion lease with Fluidstack for 245 megawatts of IT capacity at its River Bend data center campus in Louisiana with Google backstopping.

Lennar (LEN) falls 4% after the homebuilder forecast first quarter orders, deliveries and margins all below expectations, signaling strains on the housing market despite a lower interest rate.

Netflix (NFLX) rises 1.3% as Warner Bros. Discovery plans to reject Paramount Skydance’s takeover bid due to concerns about financing and other terms. Warner Bros. (WBD) shares are down 1.4%, while Paramount (PSKY) drops 1.8%.

Worthington Enterprises (WOR) falls 8% after the maker of aluminum propane cylinders posted fiscal second-quarter profit that disappointed.

Tuesday’s payrolls signaled a cooling jobs market, but not weak enough to prompt major changes to rate-cut bets in the near term. Hiring was concentrated in education and health care, as well as AI-related construction, but not much else, wrote Bloomberg Economics’ Anna Wong. The CPI data due Thursday will be the last major steer of the year. Still, investors are awaiting that report mostly with a sense of apathy, with options traders betting the S&P 500 will swing just 0.7% in either direction, according to data compiled by Barclays. That’s sharply lower than the 1% average realized move spurred by 12 reports through September. There are also signs that the recent rotation trade is fading, with the Russell 2000 index of small caps down 2.8% over three sessions.

“Yesterday’s November US jobs data is more of a confirmation of the prior expected rate path rather than a new catalyst,” said Andrea Gabellone, head of global equities at KBC Global Services.

Investors are increasingly looking for opportunities beyond the US tech giants that have underpinned the S&P 500’s 16% rally so far this year. A growing chorus of Wall Street analysts are making bullish predictions for 2026 after three straight interest-rate cuts from the Federal Reserve and as nations from the US to Germany boost spending.

“I would expect more volatility because investors are differentiating more and they are not just playing one sector,” said Guy Miller, chief strategist at Zurich Insurance. “But the combination of trend-like growth, slightly lower interest rates, fiscal impulse coming through and importantly, a significant capital spending cycle kicking in, will work its way through the economy.”

Trump’s ban on sanctioned oil tankers going into and leaving Venezuela marked a major escalation and follows the seizure of an oil tanker last week by US forces off the country’s coast. Brent crude jumped 2% to $60.11 a barrel, advancing from the lowest level since 2021.

The US is also preparing for a fresh round of sanctions on Russia’s energy sector should President Vladimir Putin reject a peace agreement with Ukraine, according to people familiar with the matter, potentially adding to the uptick in geopolitical tensions.

Europe’s Stoxx 600 Index gained 0.4%, led by the energy sector with BP and Shell rallying more than 2%, tracking gains in oil prices after Bloomberg reported the US is preparing a fresh round of sanctions on Russia’s energy sector. The UK’s FTSE 100 outperforms after inflation fell more than expected, cementing expectations for an interest-rate cut at the Bank of England on Thursday. Here are some of the biggest movers on Wednesday:

DBV shares soar as much as 47% in Paris, to the highest level since September 2022, after the company’s experimental skin patch met its primary endpoint in a late-stage trial for peanut-allergic children.

HSBC shares advance as much as 3.6% to a fresh high after KBW upgraded the lender’s shares to outperform from market perform on the strength of its Hong Kong business.

Serco shares jump as much as 5.6%, touching their highest level in more than 11 years, after the outsourcing services provider boosted its earnings guidance and introduced targets for 2026 that also exceeded expectations.

IPF shares rise as much as 8.7%, trading at their highest level since 2019, after the company extended the deadline for BasePoint to make a firm takeover offer.

Ariston shares gain as much as 6% after the Italian white goods and heating firm agreed to buy energy business Riello.

EnQuest shares rise as much as 6.1% after the oil and gas company said annual production should hit or exceed the top-end of its guidance range.

Hansa Biopharma shares plummet as much as 28% in Stockholm, the most since 2023, after disappointing results from a trial aimed at improving kidney function in patients with anti-glomerular basement membrane disease.

Suedzucker shares fall as much as 4.4% to the lowest level since 2008 after the German sugar producer said it expects a slight decrease in FY26/27 revenues as “highly challenging” conditions in the market persist.

Bunzl shares drop as much as 7.7%, the most since April, after the value-added distributor gave guidance for 2026 including moderate revenue growth and operating margin slightly down year-on-year.

Asian stocks edged higher, buoyed by a rebound in technology shares. Benchmarks rose in South Korea and Hong Kong. The MSCI Asia Pacific Index gained 0.3%, snapping a two-day decline. Samsung Electronics, SK Hynix and Tencent Holdings were among the biggest boosts to the gauge’s climb. Shares also rebounded in mainland China. Sentiment around AI valuations appears to have steadied following a two-day slide that dragged the regional tech gauge down by more than 4% through Tuesday. Investors are once again focused on earnings that may provide further catalyst for shares. Asia is seeing a busy day for stock market listings on Wednesday. Among the debuts, Chinese chipmaker MetaX Integrated Circuits Shanghai Co. soared 693%, while Japan’s SBI Shinsei Bank Ltd. and Indonesia’s digital banking firm PT Super Bank Indonesia also surged. Meanwhile, Hong Kong’s largest licensed cryptocurrency exchange HashKey Holdings Ltd. fell on its first day of trading

In FX, the Bloomberg Dollar Spot index climbs 0.3%. Cable drops 0.7% to $1.3330 with sterling at the bottom of the G-10 FX leaderboard after inflation data came in below expectations. The yen also underperforms, falling 0.5% against the greenback. The Indian rupee jumped 1% after the central bank stepped in to support it after it hit a record low amid the country’s aggressive easing policies.

In rates, UK government bonds gapped higher at the open after headline, core and service CPI readings were lower-than-expected in November. Gains have pared but UK 10-year yields are still down 4 bps at 4.48%.

In commodities, WTI crude futures rise 2.4% to $56.60 a barrel while Brent crude jumped 2.2% to $60.24 a barrel, advancing from the lowest level since 2021. Trump’s Venezuela move helped send gold above $4,330 an ounce, pushing it close to the record $4,381 set in October. Other precious metals were also gaining, with silver climbing to a record above $66 an ounce and platinum hitting the highest since 2008.

Bitcoin slid 1% to trade around $86,868 as the token headed for the fourth annual decline in its history.

US economic calendar blank for the session. Fed speaker slate includes Waller (8:15am), Williams (9:05am) and Bostic (12:30pm)

Market Snapshot

S&P 500 mini +0.3%

Nasdaq 100 mini +0.4%

Russell 2000 mini +0.3%

Stoxx Europe 600 +0.4%

DAX +0.1%

CAC 40 little changed

10-year Treasury yield +2 basis points at 4.17%

VIX -0.3 points at 16.18

Bloomberg Dollar Index +0.3% at 1208.16

euro -0.2% at $1.1718

WTI crude +2.5% at $56.66/barrel

Top Overnight News

Trump on Tues ordered a “complete blockage” of sanctioned oil tankers from accessing Venezuela and labeled the Maduro gov’t a “terrorist regime.” Brent jumped and rose further on the news of potentially more Russia sanctions. RTRS

The US is preparing a fresh round of sanctions on Russia’s energy sector should Vladimir Putin reject a peace agreement with Ukraine, according to people familiar. The new measures may be unveiled as soon as this week. BBG

Trump is expected to sign an executive order as soon as this week that would fast-track reclassification of cannabis, according to NBC News.

US told China it’s ready to defend interests in Indo-Pacific: BBG

Trump officials privately raise doubts about Hassett for Fed chair, with his critics saying he has not been effective as head of the National Economic Council, playing little part in driving policies: Politico

Amazon (AMZN +166bps premkt) is in talks to invest more then $10bn in OpenAI and sell it more chips and computing power, in the latest investment deal tying the AI start up to its infrastructure providers. FT

Jared Kushner’s Affinity Partners is withdrawing from the takeover battle for Warner Bros. Discovery. The studio plans to reject Paramount’s hostile bid, people familiar said, as its board sees the Netflix deal providing greater value. BBG

Japan’s exports gained 6.1% last month, topping estimates, with shipments to the US rising for the first time since Trump announced baseline tariffs in April. BBG

India’s central bank stepped in to support the rupee, propelling it to its biggest gain in seven months. BBG

India’s central bank governor expects the country’s interest rates to remain low for a “long period” as it enjoys robust economic growth that could soon be boosted by trade pacts being thrashed out with the US and Europe. FT

UK inflation slipped to the lowest level in eight months, with CPI rising 3.2% in November, less than expected. The pound weakened, and traders saw the data as all but sealing a BOE rate cut Thursday. BBG

European leaders rallying support for Kyiv say they are working to defend a democratic country, safeguard international law and counter Russian aggression. But there is another motivation rooted in self-interest: Europe believes a deal that favors Moscow risks a wider war that could engulf the whole continent. Cash-drained European capitals fear they would have no other choice but to massively increase military spending and defensive preparations, in the hope of preserving their deterrence. WSJ

Fed’s Goolsbee (2025 voter, hawkish dissenter) said job market is cooling at a modest pace. Said: As we go into 2026, optimistic economy will sustain at stabilised rate.

Trade/Tariffs

The UK Government announces that they are to re-join the EU’s Erasmus+ programme in 2027, with the deal including a 30% discount compared to the default terms. The UK and EU set a deadline to agree a food and drink trade deal and carbon markets linkage in 2026. Negotiations on electricity market integration has also been agreed. UK contribution will be about GBP 570mln for 2027.

UK’s EU Relations Minister Thomas-Symonds is expected to announce the UK will rejoin the Erasmus student exchange program at 12:30 GMT, according to POLITICO. The Times said UK was not able to negotiate as large a discount as it wanted from the GBP 120mln/yr that was announced.

EU diplomats told POLITICO, regarding the Mercosur trade deal, “If a compromise emerges on safeguards, EU ambassadors are expected to vote on the overall deal (Mercosur) on Friday”.

South Korea is to push for service sector FTA with China and CPTPP affiliation for export momentum, according to Yonhap.

China commerce ministry said the UN convention on cargo documents fully demonstrates China’s determination and actions to uphold true multilateralism, and strive to provide public goods globally.

US and Japan are to consider projects that may tap the USD 550bln fund, according to Bloomberg.

US President Trump posted “Numbers recently released show that TARIFFS have reduced the Trade Deficit of the United States by more than half. This is larger than anyone, except ME, projected, and will only get stronger in the near future”. Full post: “Numbers recently released show that TARIFFS have reduced the Trade Deficit of the United States by more than half. This is larger than anyone, except ME, projected, and will only get stronger in the near future. Everybody should pray that the United States Supreme Court has the Wisdom and Genius to allow Tariffs to GUARD our National Security, and our Financial Freedom! There are Evil, America hating Forces against us. We can not let them prevail. Thank you for your attention to this matter. MAKE AMERICA GREAT AGAIN!”.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were indecisive with the region lacking conviction following the uninspiring lead from Wall Street where price action was choppy as participants digested a deluge of mixed data releases. ASX 200 was subdued in the absence of bullish drivers and as gains in the mining, materials and resources sectors were offset by weakness in energy, defensives and financials. Nikkei 225 swung between gains and losses amid a choppy currency and as participants digested the better-than-expected Japanese machinery orders and exports data, but with upside limited as an anticipated BoJ rate hike looms. Hang Seng and Shanghai Comp initially traded indecisively in a narrow range with little fresh macro catalysts from China, and after the PBoC drained liquidity in its open market operations. The bourses later climbed to session highs.

Top Asian News

India’s Finance Minister said bringing down India’s debt to GDP ratio will be a core priority for the government for the next fiscal year, adds high debt to GDP ratio in some Indian states is a cause of worry.

Japanese PM Takaichi said Japan needs to strengthen its capacity through proactive fiscal policy rather than excessive fiscal tightening. said:. Sustainable fiscal policy and the social welfare system will be achieved by reflating the economy, improving corporate profits and raising household income through wage gains that boost tax revenues. Fiscal spending will be strategic rather than a reckless expansion.

Australia Treasurer Chalmers said FY27/28 budget deficit seen rising to AUD 32.6bln.

Former BoJ Deputy Governor Wakatabe said BoJ must raise the neutral interest rate through fiscal policy and growth strategies, adds the neutral interest rate would rise if demand for funds increases. said:. If the neutral rate rises due to fiscal policy and growth strategies, it would be natural for the Bank of Japan to raise interest rates. The Bank of Japan should avoid premature rate hikes and excessive adjustment of monetary support given the level of the neutral rate. Sanaenomics carries over elements of Abenomics, but focuses more on strengthening the supply side of the economy.

BoK Governor Rhee said will make sure outbound investment to US from a trade deal doesn’t hurt Forex stability. said:Need to make MPS hedging strategies more flexible and less transparent to curb herd-like behaviour.

Bank of Korea said 2026 inflation could exceed forecasts if KRW remains weak against USD.

Confederation of Japan Automobile Workers’ Union president Kaneko said he’s concerned that a BoJ rate hike on Friday could weigh on companies’ ability to raise wages next fiscal year. said:“If the yen sharply strengthened after Friday’s decision, it could affect corporate sentiment”.

South Korea forex authority said it resumes currency swap with the Bank of Korea.

European equities are trading mostly firmer. The FTSE 100 (+1.4%) is the outperformer following cooler-than-expected CPI, which increased the odds of a December cut to near 100%. European sectors are mixed. Leading sectors are Basic Resources (+1.1%), Banks (+1.1%) and Energy (+1.1%). Sentiment for Basic Resources has been underpinned by an uptick in metal prices. Energy has been lifted by crude prices nursing the prior day’s losses, fuelled by geopolitical tension between the US and Venezuela after US President Trump’s announcement of a blockade of sanctioned oil tankers entering and leaving Venezuela. Furthermore, a Bloomberg report on potential Russian energy sanctions lifted crude to highs.

Top European News

EU Climate Commissioner said they are not exempting any countries from the Carbon levy, though the UK could be exempt but only after UK carbon market linked to EU’s.

EU Commission proposes extending carbon border levy to downstream steel and aluminium-heavy products. Would also apply it to imported washing machines and machinery. Carbon borders levy revenues from 2026-27 for fund to support EU industries. Proposes system to prevent circumvention of carbon border levy, including by applying default country emissions values if companies provide unreliable data.

French Socialists (PS) have reportedly outlined conditions that would enable them to abstain instead of voting against the Finance Bill, via Politico citing various press; specific demands incl. EUR 10bln in additional spending via new financing streams.

UK PM Starmer pushes back on delayed defence spending plan and has asked military chiefs to rework aspects of the defence investment plan, according to FT.

Germany is set to approve EUR 50bln in military purchases, according to FT.

New South Wales Premier Chris Minns said to recall state parliament to discuss legislation on firearms which will cap number of firearms that can be owned and will reclassify other types of guns, as well as reduce magazine capacity for shotgun.

FX

The USD is stronger against all G10FX peers following Tuesday’s US data deluge, along with broad weakness across other majors, especially GBP and JPY. The session ahead sees comments from Fed second-in-command Williams, Fed Chair candidate Waller, and 2027 voter Bostic. There are no notable data releases until Thursday, November US CPI. DXY trades within a 98.17-98.64 range, with further gains in the greenback capped by its 100DMA at 98.62.

EUR is a little lower vs the broadly stronger USD. The single currency was little moved following the German Ifo metrics (slightly shy of exp.) and EZ HICP Finals which remained unrevised. Currently within a 1.1704 to 1.1752 range.

GBP underperforms vs G10 peers. Policymakers on Threadneedle Street this morning will welcome the cooler-than-expected UK inflation print for November, aligning with the BoE’s view that inflation had peaked and coming in at 3.2% against the expected 3.5%, lower than October’s 3.6% print. GBP, against the EUR and USD has been weakening since the 07:00 data, with further moves likely to encounter resistance at the 0.8795 and 1.33 levels respectively. Following the data, markets have moved to price an additional 10bps of easing in 2026, moving from 58bps (Tuesday) to 66bps. For the BoE confab on Thursday, expectations rose from c. 91% to a fully priced 25bps cut.

USD/JPY is lower today. Despite better-than-expected Japanese exports and machinery orders, the stronger USD, firmer energy benchmarks (on the day), and technicals have weighed on the haven in light newsflow. Remarks from Japanese Government panel member Nagahama did little to move the JPY, he said the BoJ’s monetary policy appears to be heavily influenced by FX moves. Since the beginning of the European session, and partially coinciding with the aforementioned comments, the pair breached the psychological 155 level, last crossed on Monday. As such, USD/JPY trades within 154.52-155.59 parameters. Levels to be aware of include 21 and 50DMAs, at 155.95 and 154.25, respectively.

Fixed Income

Gilts are the clear outperformer this morning. Gapped higher by 73 ticks, boosted by a cooler-than-expected November CPI series. A release that cements a December cut with markets now assigning a 99% chance of such a move (vs 91% pre-release). Ahead of the data, sell-side analysts generally viewed a 5-4 vote split as the consensus; the release today could now see the split shift a bit more dovishly. The current hawks are Mann, Pill, Greene and Lombardelli; the latter has been viewed as the most likely candidate to join Bailey in cutting rates in December, with Chief Economist Pill perhaps the other member to watch. Back to price action, Gilts are currently higher by 50 ticks and at the lower end of a 91.38 to 91.78 range.

USTs are a touch lower this morning, pulling back after ultimately settling in the green on Tuesday. Currently trading towards the lower end of a narrow 112-11 to 112-17+ range. Ahead, US data is lacking (CPI tomorrow); before that, the POTUS will deliver remarks where he could potentially outline new policies for the new year.

Bunds were essentially unchanged throughout overnight trade, but then caught a bid following the release of the UK’s inflation report (see below). The German benchmark swung from troughs to peaks following the release, but have since scaled back towards the midpoint of a 127.53 to 127.79 range. No real move on the German Ifo data, which was broadly slightly shy of expectations, another disappointing release from the region. From an inflationary standpoint, a recent Bloomberg article suggested that the US is planning new energy sanctions on Russia, if they reject a peace deal with Ukraine. This sparked upside in the crude complex, putting the German benchmark under very slight pressure – albeit within ranges.

Commodities

Crude benchmarks have completely reversed the losses seen throughout Tuesday’s as the US blocks sanctioned oil tankers going in and out of Venezuela and recent reports, from Bloomberg sources, that the US are preparing new Russian energy sanctions if Russia rejects a Ukraine peace deal. Kremlin recently said that it had not yet seen the report, but highlighted that any sanctions will harm attempts to mend relations. As soon as the Bloomberg reports came out regarding new Russian energy sanctions, WTI lifted from USD 55.95 to a 56.74/bbl session high while Brent rose from USD 59.60 to a 60.40/bbl session high.

Spot XAU continued to grind higher throughout the APAC session but remains well-contained within Friday’s range of USD 4257-5354/oz. After opening just above USD 4300/oz, XAU gradually traded higher and briefly extended beyond Tuesday’s high of USD 4335/oz, peaking at USD 4342/oz, before falling back into Tuesday’s range. XAG has, in recent sessions, dragged the yellow metal higher as investors look for cheaper alternatives to gold. XAG extended to a new ATH of USD 66.52/oz in the APAC session.

3M LME Copper bid higher throughout the Asia-Pac session, trending from USD 11.62k/t to a peak of USD 11.79k/t, in-line with the rest of the metals space. The red metal has slightly pulled back as the European session gets underway, dipping to a trough of USD 11.7k/t, but gains remain mostly in-tact as trade continues.

Kazakhstan Deputy Energy Minister said Kazakhstan oil production in the first 11 months of 2025 totalled 91.9mln tons and exports were 73.4mln tons.

Chevron Corp (CVX) spokesperson said operations in Venezuela continue without disruption following Trump’s blockade order.

US Private Inventory Data (bbls): Crude -9.3mln (exp. -1.1mln), Distillate +2.5mln (exp. +1.2mln), Gasoline -4.8mln (exp. +2.1mln), Cushing -0.5mln.

Geopolitics

Russia’s Kremlin said it is not expecting US envoy Witkoff to come to Moscow this week. As soon as the US are ready, they will inform Moscow about their talks with Ukraine.

US readies new Russian energy sanctions in the scenario that Russia rejects a Ukraine peace deal, according to Bloomberg sources; could potentially be announced as early as this week. Considering options such as targeting vessels in Russia’s “shadow fleet” of tankers used to transport Moscow’s oil. Crude benchmarks saw immediate upside. WTI lifted from USD 55.95 to a 56.68/bbl session high. Brent rose from USD 59.60 to a 60.33/bbl session high.

Ukraine’s military strikes Russian oil refinery in Krasnodar region.

EU ambassadors convene at 08:00 GMT, to talk on frozen Russian assets; a diplomat told POLITICO it was “still quite early”. Belgian Prime Minister De Wever is expected to float a legal workaround at Thursday’s summit that would allow joint EU borrowing for Ukraine, according to four diplomats. POLITICO writes that EU joint borrowing was first aired by ECB’s Lagarde, and since received support from Italy, though the idea has since been disregarded with officials dismissing it as legally unviable.

Ukrainian drone attack on Russia’s Krasnodar region injures two people and cuts power to parts of the region, according to regional authorities.

Israeli forces conduct raids in Al Tuffah and Al Zaytoun neighbourhoods east of Gaza City, according to Al Jazeera.

US Event Calendar

4:00 am: Sep New Home Sales MoM, est. -10.82%, prior 20.5%

4:00 am: Sep New Home Sales, est. 713.5k, prior 800k

4:00 am: Sep Housing Starts MoM, est. 1.61%

4:00 am: Sep P Building Permits, est. 1350k, prior 1330k

4:00 am: Sep Housing Starts, est. 1328k, prior 1307k

4:00 am: Sep Construction Spending MoM, est. 0%, prior 0.2%

7:00 am: Dec 12 MBA Mortgage Applications, prior 4.8%

Central Banks (All Times ET):

8:15 am: Fed’s Waller Speaks on Economic Outlook

9:05 am: Fed’s Williams Delivers Opening Remarks

12:30 pm: Fed’s Bostic Participates in Moderated Discussion

DB’ Jim Reid concludes the overnight wrap

The mood in markets hasn’t been very “Christmassy” this week with yesterday seeing the S&P 500 (-0.24%) post a third consecutive decline thanks to a US jobs report that could be interpreted in whichever way your biases were. The report was always expected to be choppy given the DOGE cuts and the government shutdown, but the rise in unemployment was even bigger than expected, reaching a four-year high of 4.6%. So on balance, investors interpreted the report in a dovish light, and Treasuries rallied in a choppy post payroll session, as investors priced in more cuts for 2026. Moreover, that risk-off mood was clear across the board, with US HY spreads (+5bps) reaching their highest in three weeks. And we saw Brent crude oil prices (-2.71%) close beneath $60/bbl for the first time since February 2021, at just $58.92/bbl, though they are +1.21% higher overnight after Trump ordered a blockade of sanctioned oil tankers in Venezuela. The move has taken Treasuries yields back higher too.

In terms of more detail on that jobs report, the main headline was that payrolls were down by -105k in October, before rebounding by +64k in November (vs. +50k expected). That October decline was driven by a collapse in government payrolls of -157k, marking their biggest monthly slump since the pandemic-driven losses in May 2020. But it was hard for markets to take too much optimism from the November recovery, as the unemployment rate ticked up to 4.6% (vs. 4.5% expected), and the broader U6 measure (which adds in the underemployed and those marginally attached to the labour force) hit 8.7%, the highest since August 2021. Diluting some of the concern over higher unemployment was that this was driven by re-entrants to the labour market rather than permanent job losses. Another consolation was the resilience of private payrolls, up by +52k in October and +69k in November, suggesting that things were a bit stronger away from the DOGE cuts and the shutdown. The 3-month moving average for private payrolls is in fact now at a 6-month high.

Ultimately however, the higher unemployment rate confirmed existing fears about a softer labour market, and investors priced in more Fed rate cuts for 2026. Indeed, the number of cuts priced by the December 2026 meeting was up +2.4bps on the day to 59bps. And in turn, Treasuries rallied across the curve, with the 2yr yield (-1.5bps) down to 3.49%, whilst the 10yr yield (-2.8bps) fell to 4.15%. Those moves came amid ongoing headlines surrounding the Fed Chair nomination, with the Wall Street Journal reporting that Trump was going to interview Fed Governor Chris Waller today. The latest standings on Polymarket put NEC Chair Kevin Hasset at around 53%, and comfortably back in the lead, ahead of former Fed Governor Kevin Warsh at 26% and with Waller up to 16% from 7% the previous day.

Nevertheless, equities struggled against this backdrop, with the S&P 500 (-0.24%) having now posted 3 declines since its record high last Thursday. Those moves were broad-based, with around three-quarters of the index losing ground yesterday. Indeed, the losses would’ve been larger were it not for outperformance by the Mag-7 (+0.82%), which were led by Tesla (+3.07%) reaching a new record high for first time since last December. By contrast, the equal-weighted S&P 500 was down -0.71%, with energy stocks (-2.98%) leading the decline given the latest slump in oil prices.

Brent crude fell -2.71% to $58.92/bbl, its lowest since February 2021, though it is +1.21% higher overnight after President Trump posted last night that he was ordering a “BLOCKADE OF ALL SANCTIONED OIL TANKERS going into, and out of, Venezuela”. This marks the latest move by the US to raise pressure on the Maduro regime. The overnight oil rise is also helping 10yr Treasury yields (+2.5bps) reverse some of yesterday’s decline.

In Europe, markets had followed a very similar pattern yesterday, with a risk-off move that pushed equities and bond yields lower. In part, that was driven by an underwhelming set of flash PMIs for December, with the Euro Area composite reading falling back from its two-year high in November to 51.9 (vs. 52.6 expected). So that added to fears that the economy had lost some momentum into year-end, and the STOXX 600 (-0.47%) fell back, along with yields on 10yr bunds (-0.8bps), OATs (-1.7bps) and BTPs (-2.7bps).

Admittedly, European assets were supported by signs of progress on the Ukraine negotiations, and the impact was clear in assets sensitive to the conflict. In addition to the decline in oil, the 10yr yield on Ukraine’s dollar bond (-28.4bps) fell back to 13.77%, its lowest level since March, whilst the STOXX Aerospace & Defense index (-1.79%) underperformed. Yet despite hopes for a ceasefire in the coming months, that still wasn’t enough to outweigh the broader negativity for European equities from the US jobs report and the weaker PMIs.

One exception to that pattern came in the UK, where gilts struggled after yesterday’s data leant in a hawkish direction. For instance, wage growth was up by +4.7% in the three months to October (vs. +4.4% expected), and the flash composite PMI also moved up to 52.1 in December (vs. 51.5 expected). So collectively, that suggested inflationary pressures might be stronger than thought, and 10yr gilt yields (+2.3bps) moved back up to 4.52%. Remember as well that we’ll get the UK CPI print for November shortly after this goes to press, so the focus will be on whether that continues its downward trajectory. Then the BoE meeting tomorrow.

This morning, Asian equity markets are stabilising, led by the KOSPI, which is up +0.95%. The Hang Seng (+0.22%) and the Nikkei (+0.15%) are also higher. In mainland China, both the CSI (+0.58%) and the Shanghai Composite (+0.18%) are also trading in positive territory, fueled by expectations of additional fiscal stimulus from Beijing, especially in the wake of several weaker-than-expected economic indicators for November. In contrast, the S&P/ASX 200 in Australia is bucking this regional trend, currently down -0.16%. US equity futures are down a tenth.

In Japan, exports in November recorded their fastest growth in nine months this year, increasing by an impressive 6.1% y/y. This significantly surpassed market expectations of a +5.0% rise and was also a marked improvement from the 3.6% increase observed in the preceding month. This strong export performance was underpinned by a +3.6% increase in goods shipped to Western Europe and an +8.8% surge in exports to the United States, Japan’s second-largest trading partner. Notably, this marks the first time that exports from Japan to the US have increased since March. Concurrently, imports into Japan rose by +1.3% in November, which was below the anticipated +2.5% increase. As a result, Japan’s trade balance for November amounted to a surplus of 322.3 billion yen, far exceeding the projected 72.6 billion yen surplus and representing a significant turnaround from the 226.1 billion yen deficit recorded in the prior month.

Elsewhere yesterday, we had a few other data releases, including the delayed US retail sales for October. They were unchanged (vs. +0.1% expected), but the measure excluding autos and gas stations was up +0.5% (vs. +0.4% expected), and retail control, which feeds into GDP, was up +0.8%, much higher than the +0.4% expected. Meanwhile in Germany, the expectations component of the ZEW survey moved up to a 5-month high of 45.8 (vs. 38.4 expected), although the current situation fell back to a 7-month low of -81.0 (vs. -80.0 expected).

Tyler Durden

Wed, 12/17/2025 – 08:11

https://www.zerohedge.com/markets/futures-rise-oil-rebounds-year-low

Glenview to pay $50,000 to learn whether $24 million site contains toxins

The village of Glenview will pay for additional environmental studies at a former industrial site it is slated to purchase next year after “preliminary concerns” were reportedly identified in earlier studies that were recently reviewed.

Glenview trustees on Dec. 2 voted to approve a “subsurface investigative assessment” of several areas within the 56-acre former Signode property located northeast of Pfingsten Road and West Lake Avenue.

The $49,900 study will include 18 soil borings around the site, with soil samples analyzed for contaminants, including toxic industrial chemicals and compounds. Concrete samples from building floor slabs will also be analyzed.

The Glenview Village Board voted on Nov. 4 voted to purchase the shuttered Signode property for $23.4 million, with Board members saying they envisioned it as a site for recreational uses and open space.

A manufacturer of protective packaging systems, Signode’s operations involved the use, production and storage of various materials, including petroleum, solvents, acids, paints, hydraulic fluids and lubricants, according to the village. The property contains three buildings used for manufacturing, distribution and office purposes, and has been used for heavy industrial purposes since the 1950s.

Signode relocated from Glenview to Tampa, Florida in 2021.

Earlier environmental and asbestos studies that were conducted on the property by a previous prospective buyer of the site were purchased by the village and covered under a $105,105 expenditure that also included a survey of the site.

Carlson Environmental, the company hired to review these earlier studies, will perform the new, additional assessments approved by the board.

“While they found no substantial issues to the site, they have recommended a supplemental investigation of some of the subsurface areas to fill in the gaps that are lacking information,” said Director of Community Development Jeff Brady.

This investigation, he said, will “determine the impacts for the entire site.”

Reviews of the prior studies found that underground storage tanks containing petroleum were stored on the site, many of which were found to be leaking, a memo to the Village Board states. Prior investigation of the subsurface identified chemicals that may have impacted soil, groundwater and concrete slabs in one building, according to the memo.

“The historical site operations, chemical and waste generation/storage, and documented on-site contamination have been identified as preliminary concerns,” a memo from Carlson Environmental states.

The new analysis will better determine the known area of soil contamination and groundwater conditions, according to the village. A former open drainage ditch that received waste and a former Navy burn pit adjacent to the property will also be studied.

The analysis “is intended to bring a level of comfort” that issues discovered during the earlier environmental studies “are manageable and do not pose an imminent threat to human health and the environment,” Carlson Environmental’s memo said.

Documents shared by the village do not address potential remediation of the site.

If the sale proceeds, the village is slated to take ownership of the Signode site in February. Officials envision recreational uses and open space for the site, with public input and partnerships with the Glenview Park District and area school districts ultimately determining how the land will be redeveloped.

Playgrounds, athletic fields, sports facilities, trails, natural areas and open space are all ideas for the site, Brady told the Village Board.

https://www.chicagotribune.com/2025/12/17/glenview-50000-learn-24-million-site-contains-toxins/

Carlos Alcaraz pone fin a siete años de colaboración con el entrenador Juan Carlos Ferrero

MADRID (AP) — El número uno del mundo Carlos Alcaraz anunció el miércoles que se separa de Juan Carlos Ferrero, su entrenador de toda la vida.

Alcaraz anunció su decisión de poner fin al vínculo de siete años en un mensaje en sus redes sociales.

Con Ferrero, el astro español de 22 años ha ganado seis títulos de Grand Slam: dos títulos del Abierto de Francia, dos coronas de Wimbledon y dos Abiertos de Estados Unidos.

“Tras más de siete años juntos, Juanki y yo hemos decidido poner fin a nuestra etapa juntos como entrenador y jugador”, escribió Alcaraz. “Gracias por haber hecho de sueños de niño, realidades. Empezamos este camino cuando apenas era un chaval, y durante todo este tiempo me has acompañado en un viaje increíble, dentro y fuera de la pista. Y he disfrutado muchísimo de cada paso contigo”.

Por lo pronto, Samuel López, quien se incorporó al equipo para alternarse con Ferrero en la conducción, entrenará a Alcaraz.

La nueva temporada arrancará en enero y Alcaraz tendrá en la mira el Abierto de Australia, el único cetro de un grande que le falta.

___

Deportes AP: https://apnews.com/hub/deportes

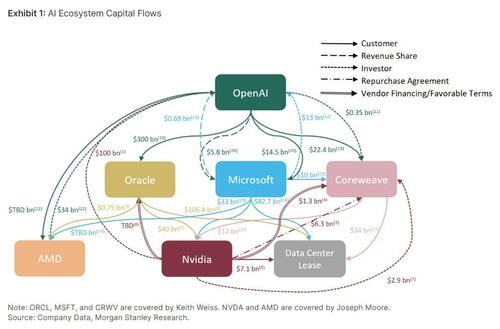

Capital-Hungry OpenAI Discussing $10 Billion Investment From Amazon

Capital-Hungry OpenAI Discussing $10 Billion Investment From Amazon

Amazon is in talks with ChatGPT-maker OpenAI to invest more than $10 billion, The Information reported, citing multiple people familiar with the discussions. The proposed round would value OpenAI at half a trillion dollars, underlining just how capital-hungry Sam Altman’s chatbot company has become, as it expects to burn through more than $100 billion over the next four years.

The Amazon investment would help OpenAI fund large-scale cloud-computing commitments and potentially broaden Amazon’s role in the AI sphere.

Here’s more from the report:

OpenAI last month announced it would spend $38 billion renting servers from AWS over the next seven years, making AWS one of at least five cloud providers OpenAI uses to develop its artificial intelligence.

The deal could also help Amazon find a new customer for its Trainium AI server chips, which compete with the Nvidia AI chips that OpenAI primarily uses today. As part of the deal under discussion, OpenAI plans to use Trainium chips, two people said.

Amazon has discussed potential commercial partnerships, including OpenAI’s plan to turn ChatGPT into a shopping and referral platform and to sell an enterprise version of ChatGPT to Amazon. However, that remains unclear because Amazon will not be able to sell OpenAI models to its cloud customers, as Microsoft, which owns about 27% of OpenAI equity, has secured an exclusive right to do so.

The people noted that Amazon financing could prompt additional fundraising rounds with more investors for the capital-hungry chatbot company, which is expected to burn more than $100 billion over the next four years.

OpenAI told investors months ago that its 2027 fundraising target is $90 billion, earmarked for investments in talent, servers, and data centers.

The Information noted, “That could theoretically include an initial public offering.”

Ahead of the new year, spending commitments for Altman’s company have been piling up. OpenAI plans to spend hundreds of billions of dollars on Microsoft and Oracle – something we have described as “circular.” It also struck deals to rent servers from Google, a major rival in developing AI, and AI cloud provider CoreWeave.

Let’s see how the circular part looks on paper:

OpenAI has also said it will invest billions in developing its own data centers and may rent servers from other companies.

The Information noted, “For Amazon, an OpenAI deal would mirror Microsoft’s approach, its fiercest cloud-services rival. After Microsoft made large equity investments in OpenAI, it recently announced an investment in rival AI developer Anthropic and agreed to use that company’s AI.”

Tyler Durden

Wed, 12/17/2025 – 07:45

https://www.zerohedge.com/ai/capital-hungry-openai-discussing-10-billion-investment-amazon

An inspiring figure, Levi Finch aims to mold a winner that future North Chicago teams can ‘aspire to be like’

On a recent frigid Sunday, there were no classes or practices to occupy North Chicago’s Levi Finch, but he didn’t sit idle.

Rather than roll over in bed or seek the comfort of a warm couch, the senior guard awoke, like he does every other day, thinking about how he could get better. So he braved the cold to get to a gym and a weight room.

“I’ve got to stay on my toes,” Finch said. “There’s always someone out there trying to get better than you. I haven’t always thought like that. But as I’ve gotten older, I understand how seriously you have to take this.”

If Finch sounds like someone who has been around the block, that’s because he has been a mainstay in North Chicago’s program longer than he has been a student at the school. Longtime boys basketball coach Gerald “King” Coleman, who has since retired, heard about Finch’s exploits at a local youth center and invited him to play with the varsity team in the summer before his freshman year.

That forced Finch to grow up quickly on the court. There were bumps in the road along the way, but the experience benefited him in the long term.

“I do wish sometimes that I got to play one freshman or JV game to see how much I could go for,” Finch said. “I still definitely enjoyed my experience being on varsity. I do think it made me a better player.”

North Chicago’s Levi Finch (12) shoots the ball over Wheeling’s Zach Neukirch (11) during a nonconference game in Wheeling on Tuesday, Dec. 16, 2025. (Talia Sprague / News-Sun)

No one could argue with that. Finch took a major step forward last season, when he averaged 18.0 points for a much-improved team that was more competitive in the Northern Lake County Conference. He’s averaging 14.6 points and 3.0 assists for the Warhawks (5-4, 1-2) so far this season, but he has also stepped forward in other ways on and off the court.

“I think of his leadership and character first and foremost,” North Chicago coach Rico McCoy said. “He sets the tone in practice every day, and that’s so important when you have four sophomores getting major minutes. He represents the school and the program with a lot of class and maturity.”

Reflecting that maturity, Finch realizes the Warhawks will be more successful if he doesn’t try to do too much.

“I can keep using all of my good traits, but it’s all of us, it’s not just me attacking the other team,” he said. “I cannot beat another team by myself. That’s why I need my teammates to have my back, and vice versa.”

Which means Finch’s younger teammates need to get comfortable on the varsity level.

“I told them that when they get up here, it’ll be a big change,” Finch said. “I tell them what they need to fix in practice, and I tell them that if there’s something they don’t understand, I’ll help them during a timeout or at halftime.”

Finch, whose father, Levi, is a former three-sport standout at North Chicago and played football at St. Norbert College, draws inspiration from former NBA stars.

“I’m a big fan of old-school basketball and love hearing stories of how vets helped newcomers and guided them,” he said. “I try to emulate guys like Steve Francis, Penny Hardaway and Isiah Thomas.”

North Chicago’s Levi Finch, left, guards Wheeling’s Peter Kulig during a nonconference game in Wheeling on Tuesday, Dec. 16, 2025. (Talia Sprague / News-Sun)

Finch also leads by example.

“When I was younger, I did look to Levi because of his scoring ability,” North Chicago sophomore guard Jonce Robinson said. “But I also look up to how he keeps his composure all the time. There were times earlier in my career that I had trouble keeping my emotions. But we’re on the same page, and it makes me better.”

At this stage of Finch’s career, winning is at the forefront of his mind. His first two varsity seasons yielded a total of six wins. The Warhawks then won 12 games last season, but Finch hopes that was only the beginning.

“The difference between last year and this year is that I told myself I knew I could be better,” he said. “Twelve wins left me wanting more.

“I’m constantly driving and working to help make the team one that after I leave the school that younger kids coming up will want to aspire to be like.”

Steve Reaven is a freelance reporter.

https://www.chicagotribune.com/2025/12/17/basketball-north-chicago-levi-finch/

Carlos Alcaraz anuncia ruptura con su entrenador Juan Carlos Ferrero

MADRID (AP) — Carlos Alcaraz anuncia ruptura con su entrenador Juan Carlos Ferrero.

Daywatch: Travel ban extended by Trump administration

Good morning, Chicago.

The Trump administration is expanding its travel ban to include five more countries and impose new limits on others.

This move is part of ongoing efforts to tighten U.S. entry standards for travel and immigration. The decision follows the arrest of an Afghan national suspect in the shooting of two National Guard troops over Thanksgiving weekend.

Here are the top stories you need to know to start your day, including a new report that Illinois could be only five years away from electricity shortages, five things we learned from the Bears and this year’s pick for Chicagoans of the Year for Museums.

Today’s eNewspaper edition | Subscribe to more newsletters | Asking Eric | Horoscopes | Puzzles & Games | Today in History

U.S. Border Patrol Cmdr. Gregory Bovino walks with agents after detaining a person while conducting an immigration enforcement operation in Little Village on Dec. 16, 2025. (Armando L. Sanchez/Chicago Tribune)

Border Patrol Cmdr. Gregory Bovino and agents return to Chicago in show of force across city and suburbs

Border Patrol Cmdr. Gregory Bovino and dozens of federal immigration agents returned in force across Chicago and the suburbs yesterday for a seemingly made-for-television jaunt about a month after he and scores of Border Patrol agents left town.

At least 100 U.S. Homeland Security agents or officers were in the Chicago area for the latest wave of federal immigration enforcement activity, according to a federal source familiar with the effort.

What to know about immigration enforcement raids in Chicago

The power lines that run northeast of 75th Street in Hodgkins are part of the ComEd power distribution system that connects the nuclear plants in Will County to the city. (Dominic Di Palermo/Chicago Tribune)

Illinois could be only 5 years away from electricity shortages, higher bills, report says

With artificial intelligence sparking a surge in electricity demand, Illinois could be only five years away from chronic shortages and higher monthly bills, according to a report released late Monday by three state agencies.

Dr. Sameer Vohra, director of the state health department, speaks before Gov. JB Pritzker signed Illinois House Bill 767 on Dec. 2, 2025, at the Illinois Department of Human Rights office in Chicago’s West Loop. (Dominic Di Palermo/Chicago Tribune)

Illinois should recommend hepatitis B vaccines for all newborns, committee says, despite federal guidance

Illinois should continue to recommend that nearly all newborns be vaccinated against hepatitis B, a state advisory committee decided yesterday, in a move that could represent another break with federal vaccine guidance.

The family of slain Chicago police Officer Andrés Mauricio Vásquez Lasso, including his widow Milena Estepa de Vásquez, left, and mother, Rocio Lasso, second from right, at the Leighton Criminal Court Building, Dec. 16, 2025, after Steven Montano was sentenced to life in prison for Vásquez Lasso’s murder in 2023. (Eileen T. Meslar/Chicago Tribune)

Man given life sentence in slaying of Chicago police officer, though recent law offers a chance at parole

After several hours of arguments and testimony, Cook County Judge John Lyke ordered a sentence of life in prison for Steven Montano, 21, after a jury in July convicted him of first-degree murder following a weeklong trial that showcased body camera footage of the slaying and emotional testimony from his wife and other responding police officers.

Medline Industries, Inc. on Nov. 1, 2018, in Waukegan. (Erin Hooley/Chicago Tribune)

Medline raises more than $6.2 billion in initial public offering, one of the largest of the year

Medline sold about 216 million shares at $29 a piece — a larger offering than the company had initially outlined. The company said earlier this month that it planned to sell 179 million shares for between $26 and $30 a share. Shares of the massive medical supply company will begin trading publicly today on the Nasdaq Global Select Market under the symbol MDLN.

A group prays the Rosary during a vigil held by the Diocese of Gary outside the Indiana State Prison in Michigan City on Oct. 9, 2025, hours before the scheduled execution of Roy Lee Ward. (Michael Gard/for the Post-Tribune)

Indiana Senate bill would allow firing squad for death penalty

A bill allowing for firing squad executions for death penalty inmates was filed in the Indiana legislature for the 2026 session.

Gov. JB Pritzker smiles after signing the Northern Illinois Transit Authority Act, a state transit funding and reform bill, at Union Station, Dec. 16, 2025. (Eileen T. Meslar/Chicago Tribune)

JB Pritzker signs transit bill that should avert major service cuts, but cautions that ‘transformation’ takes time

Gov. JB Pritzker celebrated his enactment of a new law that advocates say will avert catastrophic service cuts on Chicago’s public transit systems and make the region’s trains and buses safer and more reliable — even as he acknowledged “transformation takes a little bit of time.”

Bears quarterback Caleb Williams waits in the tunnel before a game against the Browns on Dec. 14, 2025, at Soldier Field. (Dominic Di Palermo/Chicago Tribune)

5 things we learned from the Chicago Bears, including why Caleb Williams is OK with being a little ‘arrogant’

The Bears had a rare Tuesday workday, holding a walk-through as they prepare for Saturday night’s NFC North showdown against the Green Bay Packers at Soldier Field.

Here are five things we learned at Halas Hall.

Bears Q&A: Has the schedule prepared them for playoffs? Is it a surprise Packers are favored?

Bears QB Caleb Williams has dubbed each of his O-linemen an Avengers character — see who he picked

Chicago Cubs pitcher Caleb Thielbar pitches against the Chicago White Sox during spring training at Sloan Park on Feb. 22, 2025, in Mesa, Arizona. (Armando L. Sanchez/Chicago Tribune)

Chicago Cubs to bring back veteran lefty reliever Caleb Thielbar after his bounce-back season

The Cubs are bringing back one of their most reliable relievers.

The Cubs have a deal in place with veteran left-hander Caleb Thielbar, pending a physical, a source confirmed to the Tribune. Thielbar, who turns 39 in January, is coming off one of his best big-league seasons following an underwhelming performance with Minnesota in 2024.

Line cook Jesus Rosario has a laugh with chef Darryl “D.C” Carter, left, and executive chef Corey Rice as Rosario prepares a wine reduction for a short ribs dish at Burnham Yacht Club in Chicago on Dec. 12, 2025. Rice hired Rosario for a full-time role in September after Rosario interned at the club following his completion of the free culinary bootcamp style 12-week program at Inspiration Kitchens. (Chris Sweda/Chicago Tribune)

Inspiration Kitchens’ free culinary boot camp helps students break barriers to find jobs in food service

“Dine well, do good.”

It’s a simple quote plastered in big, bold letters above Inspiration Kitchens’ service window in East Garfield Park. But it’s a value that extends beyond the front-of-house and out into the world, where students hope to land a job in the culinary industry after they’ve sharpened their knife skills and learned to chiffonade basil.

Executive director Lisa Lee, center, is surrounded by staff, artists and former public housing residents at the National Public Housing Museum on Dec. 3, 2025, in Chicago. (Brian Cassella/Chicago Tribune)

Chicagoans of the Year for Museums: National Public Housing Museum staff keeps residents at heart

The National Public Housing Museum opened on the Near West Side in the spring on the former site of the Jane Addams Homes, near the University of Illinois Chicago.

A gleaming LED display in the lobby recaps decades of public housing history. Nearby, the museum’s gift shop promotes small businesses and merch by public housing residents. Upstairs are an oral history studio and an interactive listening room, allowing visitors to spin LPs by musicians who once lived in public housing.

See the list of 2025 Chicagoans of the Year announced so far

https://www.chicagotribune.com/2025/12/17/daywatch-travel-ban-extended-by-trump-administration/

Warner Bros pide a sus inversionistas que rechacen la oferta de adquisición de Paramount Skydance

Associated Press

NUEVA YORK (AP) — Warner Bros. ha recomendado a los accionistas que rechacen una oferta de adquisición de Paramount Skydance, afirmando que una oferta rival de Netflix será mejor para los clientes.

“Creemos firmemente que la unión de Netflix y Warner Bros. ofrecerá a los consumidores más opciones y valor, permitirá a la comunidad creativa llegar a más público con nuestra distribución combinada y alimentará nuestro crecimiento a largo plazo”, indicó Warner Bros el miércoles. “Hicimos este acuerdo porque su amplio portafolio de franquicias icónicas, su extensa biblioteca y sus fuertes capacidades de estudio complementarán, no duplicarán, nuestro negocio existente”.

Paramount lanzó una oferta hostil la semana pasada, pidiendo a los inversionistas que rechacen el acuerdo con Netflix favorecido por la junta de Warner Bros.

Paramount está ofreciendo 30 dólares por acción de Warner frente a los 27,75 de Netflix.

La oferta de Paramount no está completamente descartada. Aunque la carta del miércoles a los accionistas significa que la oferta de Paramount no es la preferida por la junta de Warner Bros., los accionistas aún pueden decidir ofrecer sus acciones a favor de la oferta de Paramount por toda la compañía, incluyendo las gigantes de la televisión por cable CNN y Discovery.

A diferencia de la oferta de Paramount, la propuesta de Netflix no incluye la compra de las operaciones de cable de Warner Bros. Una adquisición por parte de Netflix, si es aprobada por los reguladores y accionistas, se cerrará sólo después de que Warner complete la separación previamente anunciada de sus operaciones de cable.

Paramount ha afirmado que hizo seis ofertas diferentes que la dirección de Warner rechazó antes de anunciar su acuerdo con Netflix el 5 de diciembre. Solo después de eso llevó su oferta directamente a los accionistas de Warner.

Más allá de la luz verde de los accionistas, ambas ofertas de adquisición enfrentan un tremendo escrutinio regulatorio. Un cambio de propiedad en Warner remodelaría drásticamente la industria del entretenimiento y los medios, impactando la producción cinematográfica, las plataformas de streaming para consumidores y, en el caso de Paramount, el panorama de noticias.

Los críticos del acuerdo con Netflix dicen que combinar la enorme compañía de streaming con HBO Max de Warner le daría un dominio abrumador del mercado, mientras que el servicio de streaming Paramount+ es mucho más pequeño.

“Esto es algo que hemos escuchado durante mucho tiempo, incluso cuando comenzamos el negocio de streaming”, dijo Warner Bros. en una presentación de valores el miércoles. “Nuestra postura entonces y ahora es la misma: vemos esto como una victoria para la industria del entretenimiento, no como su fin”.

Las ofertas de Netflix y Paramount han generado alarma por lo que podrían significar para la producción de cine y televisión. Mientras que Netflix ha acordado mantener las obligaciones contractuales de Paramount para los estrenos teatrales, los críticos han señalado su modelo de negocio pasado y su dependencia de los lanzamientos en línea. Sin embargo, Paramount y Warner Bros. son dos de los “cinco grandes” estudios fundacionales que quedan en Hollywood hoy.

El intento de Paramount de comprar las redes de cable y el negocio de noticias de Warner también pondría a CBS y CNN bajo el mismo techo. Además de acelerar aún más la consolidación de medios, eso podría plantear preguntas sobre cambios en el control editorial, como se vio en CBS News tanto antes como después de la compra de 8.000 millones de dólares de Skydance de Paramount, que completó en agosto.

El presidente Donald Trump ya ha sido vocal sobre su futura participación en el acuerdo, indicando que la política jugará un papel en la aprobación regulatoria.

Trump dijo anteriormente que el acuerdo de Netflix “podría ser un problema” debido al potencial de un control desproporcionado del mercado. El presidente republicano también tiene una relación cercana con el fundador multimillonario de Oracle, Larry Ellison, el padre del CEO de Paramount, cuyo fideicomiso familiar también respalda fuertemente la oferta de la compañía para comprar Warner.

Affinity Partners, una firma de inversión dirigida por el yerno de Trump, Jared Kushner, declaró anteriormente que invertiría en el acuerdo de Paramount, también. Pero el martes, la firma anunció que se retiraría de la oferta.

Aún así, Trump también tiene una tendencia a tomar decisiones basadas en su instinto y su estado de ánimo personal. Ha continuado atacando públicamente a Paramount por decisiones editoriales en “60 Minutes” de CBS.

“Para aquellas personas que piensan que estoy cerca de los nuevos dueños de CBS, por favor entiendan que 60 Minutes me ha tratado mucho peor desde la llamada ‘adquisición’ de lo que me han tratado antes”, escribió Trump en su plataforma Truth Social el martes. “¡Si son amigos, no me imagino cómo serán mis enemigos!”

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

Euroclear: The Line Europe Can’t Cross Without Breaking Global Trust

Euroclear: The Line Europe Can’t Cross Without Breaking Global Trust

Submitted by Thomas Kolbe

Euroclear and the Looming Breach of Trust

The alliance financing the war in Ukraine is facing a new problem. Seven members of the European Union want to block the expropriation of the Russian central bank assets held at Euroclear. This puts the continuation of war financing at risk. At the same time, the specter of a financial crisis looms—one that would once again leave taxpayers footing the bill.

The negotiation marathon between representatives of Ukraine, the EU and the United Kingdom, with a US delegation acting as mediator, continues in Berlin. As usual, it is accompanied by familiar phrases about “progress” on the road to peace and assurances that roughly 90 percent of the target has already been reached.

How much weight this interim result actually deserves will become clear in the coming days. Expect a frantic ramp-up of the propaganda machine, drones over airports (and over Wolfram Weimer’s residence), and growing pressure on US President Donald Trump. The militarily precarious situation of Ukraine’s armed forces is now colliding with an almost equally dramatic financial situation among Kyiv’s creditors.

Everything points to mounting pressure to cut the Gordian knot—sooner rather than later—as war costs on both sides threaten to spiral out of control.

This brings the latest developments in the debate over the expropriation of the Russian central bank and its assets parked at Euroclear back into sharp focus.

A Critical Demarcation Line

Euroclear could turn into a personal Waterloo for EU Commission President Ursula von der Leyen. She is working at full throttle to convert the current crisis into a massive expansion of power for Brussels—and thus for her Commission.

Hungary, Slovakia and Belgium—already outspoken critics of expropriating Russian assets—are now joined by Italy, Bulgaria, Malta and Cyprus. Resistance to Brussels’ escalation push is growing by the day.

Notably, this resistance coincides with a clear shift in timing. Since the United States effectively withdrew from financing Ukraine, Europe’s financial reality has come into view without cosmetic filters. Without access to roughly €210 billion in Russian assets—about €25 billion of which are spread across various EU states—continued financing of this war of attrition appears barely feasible.

All major creditors—Germany, France and the United Kingdom—have long overstretched their budgets and are running new debt levels between four and six percent. The Ukraine project is on the brink of fiscal collapse.

The Illusion of Expropriation as a Lifeline

What is being attempted is as simple as it is dangerous. These assets—partly government bonds, partly matured bond holdings in foreign currencies—are to be used as collateral for further loans. Europe is already trapped in a debt spiral and is tapping every remaining source of funding. Even the enemy is no longer off-limits for the London-Brussels tandem.

Observers with a sensitivity for political phraseology and grandiosity understood as early as April 2022 what was unfolding: in a state of euphoric overconfidence, decision-makers catastrophically miscalculated and constructed a scenario in which a defeated Russia would be forced to pay for the entire war. This would have allowed Europe to neatly extract its own banks—deeply entangled in Ukraine’s financing—from the equation.

History offers a familiar pattern: bankers and politicians working hand in hand, this time in Kyiv. Many were already anticipating the day of Putin’s submission, followed by regime change in Moscow and the launch of large-scale extraction of Russia’s immense raw-material wealth. Europe’s banking system would have been recapitalized to the rooftops, and the energy problem solved once and for all.

That calculation has clearly failed. Instead, the taxpayer will bear the losses.

Ukraine as a Systemic Risk

Without credit guarantees, Ukraine would already be insolvent. A disorderly collapse of the state would hit the European banking system like a nuclear detonation. There is no realistic way around the public sector eventually absorbing these massive loan liabilities.

This inevitably brings the debate over expanding Eurobonds—formally prohibited under EU law—back to center stage, potentially reintroduced outright as European war bonds.

With the “NextGenerationEU” program, this supposedly forbidden practice has already become de facto reality. Brussels has raised €800 billion on capital markets through this mechanism. These funds fuel the EU’s bloated subsidy machine and are now structurally embedded in its power architecture, always backstopped by the ECB.

Brussels is already acting as a sovereign bond issuer in its own right, further increasing member states’ liability exposure and debt levels. Europe has maneuvered itself into both a geopolitical and financial dead end—an outcome that has been foreseeable for years.

Euroclear and the Looming Breach of Trust

The chronic reality denial and embedded incompetence of EU and UK political leadership defy rational explanation. All the more notable is the emerging resistance around Euroclear—even as Brussels searches for ways to force the decision through by simple majority if necessary.

There is reason for cautious optimism that countries like Italy understand what expropriating Russian central bank assets at Euroclear would mean for the eurozone’s financial stability. Italian Prime Minister Giorgia Meloni’s initiative to discreetly safeguard Italy’s central-bank gold against potential ECB access underscores that Rome knows exactly what is at stake. Italy would be well positioned for a potential reboot of a sovereign currency.

The damage caused by expropriating Russian assets would be maximal: a financial super-GAU, a total loss of credibility and of the merchant-law principles indispensable to banking and international transactions. The entire global financial system—transaction settlement and custodial asset holding—rests on trust: on the absolute stability of its core pillars.

Institutions like Euroclear are among those pillars. They do not merely safeguard international transaction flows—they make them possible in the first place. Once this foundation is damaged, far more than a political signal is at risk. The stability of the entire system is on the line.

Tyler Durden

Wed, 12/17/2025 – 07:20

https://www.zerohedge.com/markets/euroclear-line-europe-cant-cross-without-breaking-global-trust

Warner Bros pide a accionistas rechazar oferta de Paramount, dice que una fusión con Netflix es mejor para los clientes

NUEVA YORK (AP) — Warner Bros pide a accionistas rechazar oferta de Paramount, dice que una fusión con Netflix es mejor para los clientes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}