Category: News

Iran “Laying Traps” And “Building Up Defenses” On Kharg Island, Preparing For U.S. Ground Attack

Iran “Laying Traps” And “Building Up Defenses” On Kharg Island, Preparing For U.S. Ground Attack

Iran has recently bolstered its defenses around Kharg Island, anticipating a possible US move to seize the key oil export hub, CNN reported this week. The island is vital to Iran’s economy, handling roughly 90% of its crude shipments, and has become a focal point in escalating tensions.

The Trump administration has explored the option of sending US forces to take control of the island as leverage to pressure Iran into reopening the Strait of Hormuz. But military officials caution that such an operation would carry serious risks. Iran has reinforced the island with additional air defense systems, including portable missiles, and has planted mines along likely landing zones.

There is also growing skepticism among US allies and policymakers about whether capturing the island would achieve its broader objective. Even if successful, it may not resolve the wider dispute over energy flows and could instead intensify the conflict. An Israeli source warned that US troops could face attacks from drones and shoulder-fired missiles if they attempt a landing.

“I would be very worried about this,” said retired Adm. James Stavridis. “Iranians are clever and ruthless. They will do everything they can to inflict maximum casualties on US forces both on the ships at sea, and especially once ground troops are anywhere in their sovereign territory.”

CNN writes that Iran has responded with its own warnings. Parliament speaker Mohammad Bagher Ghalibaf said any attempt to occupy Iranian territory would prompt retaliation against critical infrastructure in the region, adding that US troop movements are under close watch.

Despite its relatively small size—about one-third of Manhattan—Kharg Island would require a substantial military operation to capture. US forces in the region include Marine units trained for amphibious assaults, along with airborne troops preparing to deploy. Surveillance has shown newly fortified positions and defensive preparations on the island.

Although earlier US strikes weakened parts of Iran’s defenses, American forces would still face significant threats from missiles and drones launched from the nearby mainland. This has led to internal debate in Washington over whether the potential benefits justify the risks.

Regional allies are urging restraint, warning that a ground assault could result in heavy casualties and trigger wider retaliation across the Gulf. Some analysts suggest that targeting Iran’s oil exports through a naval blockade could be a less risky alternative to putting troops on the ground.

Tyler Durden

Thu, 03/26/2026 – 09:05

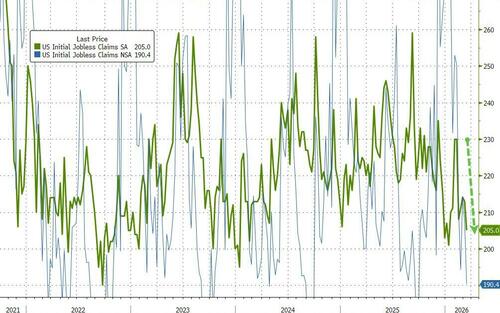

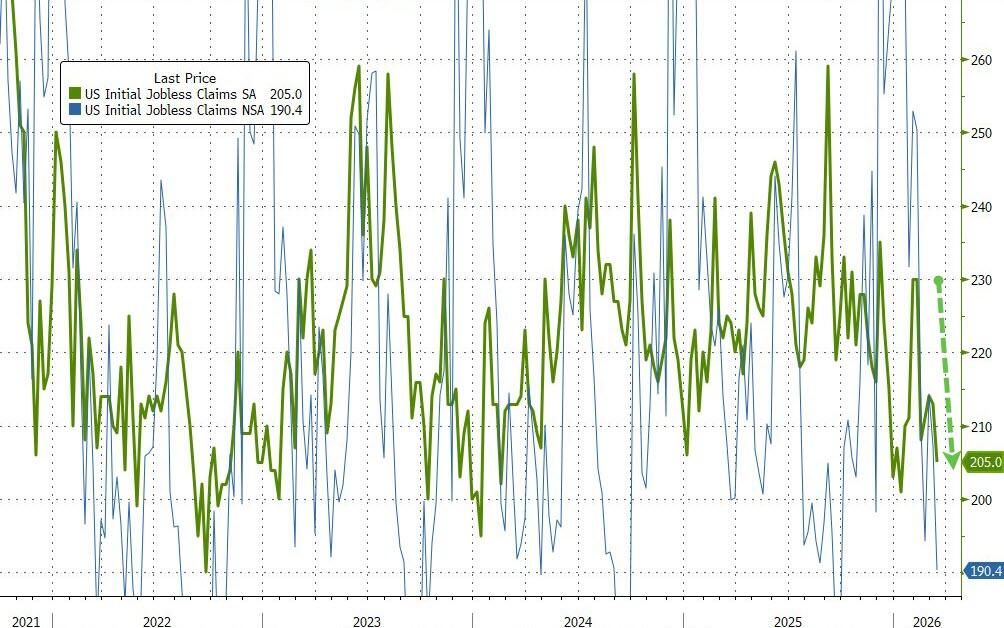

Jobless Claims Hover Near Record Lows Sustaining ‘No Hire, No Fire’ Narrative

Jobless Claims Hover Near Record Lows Sustaining ‘No Hire, No Fire’ Narrative

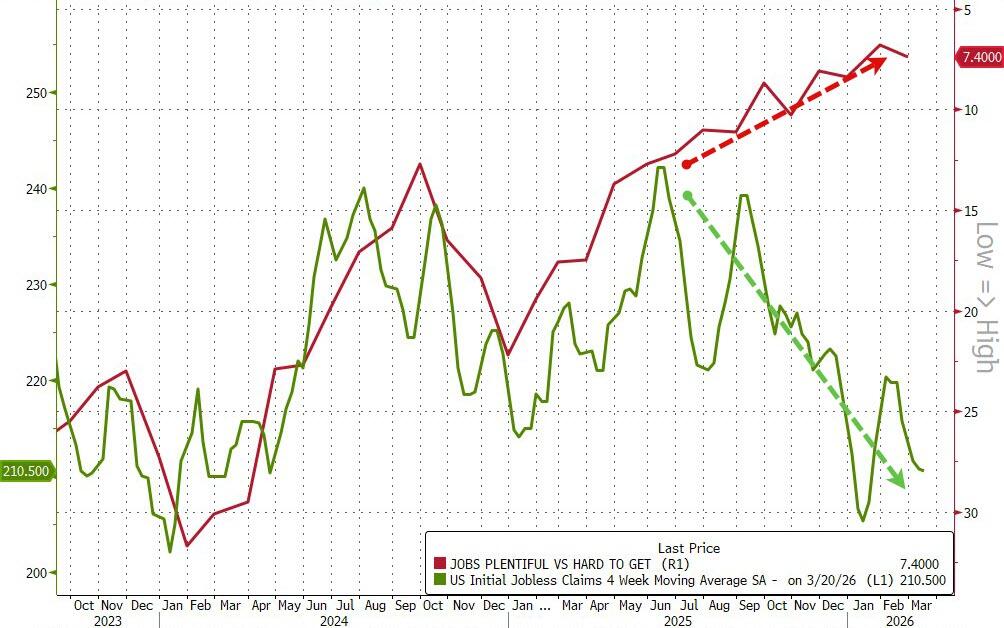

The number of Americans filing for unemployment benefits for the first time was flat from the prior week at 210.5k (215k exp). Simply put, these numbers are hovering near their lowest levels since 1969…

Source: Bloomberg

Continuing claims also printed below expectations at 1.819 million Americans. This is the lowest level since May 2024…

Source: Bloomberg

Finally, as a reminder, sentiment surveys suggest the labor market is bifurcated with ‘jobs hard to get’ but joblessness not surging…

Source: Bloomberg

That chart reinforces the ‘no hire, no fire’ economy remains the status quo – no worse, no better.

Tyler Durden

Thu, 03/26/2026 – 08:35

Stocks, Bonds Slide As Ceasefire Hopes Fade

Stocks, Bonds Slide As Ceasefire Hopes Fade

It’s Day 27 of the war: stocks and bonds fell globally as ceasefire optimism fades given mixed messages on progress toward ending the war in Iran and growing uncertainty over Iran’s willingness to engage in talks about a ceasefire in the Middle East sent oil prices higher. Futures gapped lower just after 5am ET, when Axios reported that the Pentagon is developing military options for a “final blow” in Iran that could include ground troops. Trump urged Iran “to get serious” before it was too late but Tehran is steadfast saying no negotiations are occurring and both side rejecting each other’s deal demands as the fighting continues & more military assets arriving. As of 8:00am ET, S&P 500 futures dropped 0.9%, at session lows, with about 48 hours before a US delay in strikes on Iranian energy infrastructure expires. Nasdaq futures slumped more than 1%.In premarket trading, Mag7 names were down with all sectors lower ex-Energy. Brent resumed its advance, rising 3.8% to above $106 a barrel; Oil is on track for its biggest monthly jump in more than three decades, as the Trump administration examines potential consequences if prices spike to $200 a barrel. The move rekindled inflation fears and pushed yields higher as money markets priced in tighter monetary policy. Two-year Treasury yields rose four basis points to 3.93% as the yield curve bear flattened with yields +4 – 6bp; the 10Y yield was back up to 4.39%, pushing the USD also higher. Gold slipped below $4,450 an ounce. Today’s macro data focus is on initial / continuing claims

In premarket trading, Mag 7 stocks are all lower (Alphabet -1%, Amazon -1%, Apple -0.2%, Nvidia -1.2%, Meta -1.3%, Microsoft -0.4%, Tesla -1%)

US mining stocks fell and energy stocks rose as attacks in the Middle East continued and US President Donald Trump warned Iran to get serious about discussions “before it is too late.”

Memory-chip stocks fall in reaction to a new compression technique proposed by Google researchers that could reduce the amount of memory needed for AI workloads. Micron (MU) falls 2% while Sandisk (SNDK) declines 3%.

Equitable Holdings Inc. (EQH) gains 3% and Corebridge Financial Inc. (CRBG) rises 1.7% as the US insurers are set to merge in an all-stock deal valuing that combined business at $22 billion.

Kodiak Sciences (KOD) climbs 43% after the drug developer gave efficacy data from a late-stage trial of its experimental drug for diabetic retinopathy — a complication of diabetes that affects the eyes.

MillerKnoll (MLKN) drops 18% after the office furniture designer’s earnings forecast for the fourth quarter missed the average analyst estimate.

Navan (NAVN) rises 18% after the business travel platform reported fourth-quarter results that beat expectations and gave an outlook analysts see as both positive and conservative.

Olaplex (OLPX) rose more than 50% after Henkel agreed to buy the hair-care brand in a $1.4 billion deal.

Precigen (PGEN) jumps 15% after the biopharmaceutical company said first-quarter revenue is expected to exceed $18 million, driven by sales of its recurrent respiratory papillomatosis treatment, Papzimeos.

In other corporate news, Blackstone is said to be close to a deal to buy Rowan Digital Infrastructure, which may value the major U.S. data center developer at more than $10 billion. Novo Nordisk’s Chairman is set for an earful at the AGM after a boardroom coup, with investors pointing to recent missteps.

With markets already on edge over Iran’s unwillingness to negotiate ceasefire terms, the mood deteriorated overnight after an Axios report that the Pentagon is developing military options for a “final blow” in Iran that could include the use of ground forces and a massive bombing campaign. Trump claimed Iran was desperate for a deal to end hostilities and the White House insisted peace talks are ongoing, even as Tehran publicly rejected US overtures and issued fresh conditions of its own to end the conflict. Those included sovereign control over the Strait of Hormuz, and drafting laws to introduce tolls for safe passage.

“If Iran were to signal willingness to negotiate and an end to the closure of the Strait of Hormuz became more likely, equity markets may quickly move back to previous highs,” said Wolf von Rotberg, strategist at Bank J Safra Sarasin. “Yet Iran has so far declined all offers to talk as time is on their side.”

In AI news, memory stocks are under pressure on concerns over demand after Google researchers touted its new TurboQuant technology, a new compression technique. Bulls suggest the improved efficiency may actually increase demand, but related stocks at risk of profit taking after exponential moves in related stocks. Accenture launched Cyber.AI powered by Claude, Anthropic’s AI model.

Private credit is again in focus after Jefferies’ results missed Wall Street estimates, dragged down by losses on wayward credit bets, an Ares private credit fund posted its steepest monthly loss on record and ex-Goldman CEO Lloyd Blankfein warned of “fire” risk in private markets. In contrast, executives from Apollo, Blackstone and Blue Owl said they don’t see evidence of rising systemic risks or defaults, which is to be expected since they all run… private credit funds.

BlackRock Inc. President Rob Kapito said investors may be underestimating the risks stemming from the war, which are likely to weigh on economic growth and drive inflation higher even if the conflict ends soon.

“What if this disruption is a week, six months, a year — what is it going to mean for the companies that I own?” Kapito said. “My biggest concern is that people aren’t looking at this – they’re just making the assumption” for an optimistic outcome.

JPMorgan expects around $65 billion of equity buying and bond selling due to March-end rebalancing; Goldman sees a more modest $13 billion. Elsewhere, global investors are on track to withdraw a record amount from Asian EM equities excluding China, as surging oil prices due to the Middle East conflict cloud the region’s outlook.

The Fed’s Stephen Miran said he moved up his projection for where interest rates should end the year by half a percentage point in response to disappointing inflation data, not due to oil and Iran. A plethora of Fed speakers are on deck later today.

In politics, FHFA’s Pulte sent letters to the DOJ encouraging prosecutors to open new fraud investigations into New York Attorney General Letitia James related to real estate. G-7 energy, finance ministers and monetary policy makers will meet on Monday to discuss the situation in the Middle East. Officials in Berlin have started mapping vulnerabilities in US supply chains to identify points where Germany and its European Union partners could apply pressure.

European stocks slumped more than 1.2% as higher energy prices dampen sentiment. Stoxx 600 falls 1.2% to 580.54 with mining and technology stocks leading declines. The biggest outperformers were chemicals and personal care shares. Here are the biggest movers Thursday:

Next shares rally as much as 6.9%, the most in five months, after the clothing retailer posted annual profits that were slightly ahead of the upgraded guidance outlined in January, having boosted its outlook five times throughout the year

Comet rises as much as 4.8% after BNP Paribas double-upgrades the semiconductor equipment components supplier to outperform from underperform, citing expectations the company will benefit from a multi-year memory capex super-cycle

THG shares rise as much as 8.8%, among the top gainers in the FTSE 250 Index on Thursday morning, after the online retailer reported 2025 results and said it’s had a strong start to the new year, which support revenue and adjusted Ebitda expectations

Pollen Street rises as much as 8.4%, the most since Jan. 2025, after the alternative asset manager delivered results which Panmure Liberum says came in ahead of consensus expectations

The Stoxx 600 basic resources index is the worst-performing sector in Europe, falling as much as 3.6% on Thursday

Boliden drops as much as 19%, the most since January 2008, after providing an update on the abnormally high seismic activity that has impacted production at its key Garpenberg mine

Edenred shares drop as much as 16%, slumping to a 2016-low, after the Italian Competition Authority launched an investigation into its Italian subsidiary over possible abuse of its dominant market position in the meal voucher market

H&M slips as much as 6.6%, the most since September 2024, after the Swedish fast-fashion retail group reported weaker-than-expected current trading which analysts said overshadowed margin strength in the first quarter

Currys shares drop as much as 11%, the most in over two years, after announcing the departure of Chief Executive Alex Baldock

3i Group shares fall as much as 3.3% after sales and margin at Action, its largest portfolio company, missed analyst estimates

CSG shares fall as much as 6.7% after the recently-listed defense firm posted weaker-than-expected earnings in its Ammo+ small caliber ammunition division, though it saw a better performance in military vehicles and weapons

Asian stocks fell after two consecutive days of gains as conflicting signals from the US and Iran about their ceasefire talks turned investors cautious. The MSCI Asia Pacific Index fell as much as 1.4% before paring some declines. Shares of South Korean chipmaking giants Samsung and SK Hynix were the biggest drags on the benchmark, slumping on concerns over demand after Google researchers touted a new compression technique that can reduce memory size for large language models and vector search engines. Equity benchmarks in Hong Kong and Indonesia were among the top losers in Asia alongside the Kospi, while markets in India were shut for a holiday. Strategists at Goldman Sachs downgraded the South Asian nation’s stocks to marketweight from overweight, citing higher‑for‑longer energy prices from the war.

In FX, markets are contained compared to stocks and bonds with the Bloomberg Dollar Spot Index barely up 0.1% as the greenback posts a mixed performance versus peers.

In commodities, Brent crude is up over 3% and around the $106 per barrel mark with the US and Iran providing conflicting comments on efforts to end the war. More recently, an Axios report noted that the Pentagon is developing military options for a “final blow” in Iran.

In rates, higher energy prices are again dragging bonds lower with US yields up 4-5bps across the curve. Norwegian bonds saw further losses after the Norges Bank held rates steady but pointed towards a potential rate hike.

Spot gold and silver are on the back foot, showing respective losses of 1.5% and 4%. Bitcoin is down 1.9%.

US economic data scheduled includes weekly initial jobless claims (8:30am) and March Kansas City Fed manufacturing activity (11am). Fed speaker slate includes Cook (4pm), Miran (6:30pm), Jefferson (7pm) and Barr (7:10pm)

Market Snapshot

S&P 500 mini -0.8%

Nasdaq 100 mini -1%

Russell 2000 mini -1.2%

Stoxx Europe 600 -1.3%

DAX -1.6%

CAC 40 -1.1%

10-year Treasury yield +4 basis points at 4.38%

VIX +2.2 points at 27.51

Bloomberg Dollar Index little changed at 1212.32

euro little changed at $1.1557

WTI crude +3.4% at $93.38/barrel

Top Overnight News

The Pentagon is developing military options for a “final blow” in Iran that could include the use of ground forces and a massive bombing campaign: Axios

President Trump has told associates in recent days that he wants to avoid a protracted war in Iran and that he hopes to bring the conflict to an end in the coming weeks. The president has privately informed advisers he thinks the conflict is in its final stages, urging them to stick to the four-to-six-week timeline he has outlined publicly, according to people familiar with the matter. WSJ

Israeli officials say a US-Iran deal remains unlikely, but fear President Donald Trump could still declare a temporary ceasefire as talks continue. Jerusalem Post

Trump administration officials are examining what a potential spike in oil prices as high as $200 a barrel would mean for the economy, according to people familiar with the matter, a sign senior officials are studying the possible fallout from extreme scenarios for the Iran war. BBG

On the stage and sidelines of a global energy conference in Houston, CEOs painted a much bleaker picture: Financial markets aren’t accurately reflecting the gravity of the crisis, the war is crippling the world’s fuel supplies, and the industry’s Middle East operations are at risk, they said. WSJ

Hong Kong is weighing “big bang” tax cuts that may allow many asset managers to earn their performance fees free of all levies. FT

Norway’s central bank said it’ll probably raise its benchmark rate at one of its forthcoming meetings. Officials left it at 4% today, as expected. BBG

Germany has plans for the EU to squeeze US tech, drug supplies and manufacturers in its next dispute with Trump. The goal is to create a consensus among bloc members on how to best use their leverage. BBG

Gulf and European allies are closely watching and growing concerned about the lack of momentum towards negotiations to end the conflict or even put a ceasefire into place. CNN

An Ares-managed $23 billion private credit fund posted its steepest monthly loss on record in February. BBG

Global investors are on track to withdraw a record amount from Asian EM equities excluding China, as surging oil prices due to the Middle East conflict cloud the region’s outlook. BBG

White House confirms that US President Trump is to hold a cabinet meeting is to be held from 10:00EDT/14:00GMT on Thursday.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded cautiously as the geopolitical situation in the Middle East remained fluid, with mixed messages from the US and Iran about talks, while strikes persisted overnight against Iran and its regional neighbours. ASX 200 closed slightly lower with miners, tech and materials front-running declines, but with downside cushioned by gains in energy, defensives and financials, while price action was contained by a lack of data or fresh major catalysts. Nikkei 225 retreated as the rebound in oil stoked inflationary and growth concerns, given Japan’s large dependency on Middle East oil, despite the government releasing emergency oil reserves, as planned. Hang Seng and Shanghai Comp were pressured amid a deluge of earnings releases and with developer debt concerns stoked as China Vanke seeks another bond repayment delay, whilst it works on a restructuring plan.

Top Asian News

Japan’s provisional budget is seen totalling around JPY 8.6tln, according to NHK.

European bourses (STOXX 600 -1.1%) have gotten off to a softer start to Thursday’s session. The DAX 40 underperforms, hindered by poor Porsche SE (-2.6%) earnings, while the SMI outperforms with only mild losses, as Kuehne+Nagel, along with the broader shipping sector, is supported by Hapag-Lloyd earnings. European sectors are entirely in the red, with Basic Resources, yet again, sitting at the bottom of the pile as metals prices continue to fall. Technology also prints decent losses, following news stateside by Google that its new TurboQuant tech can reduce the amount of memory needed for AI workloads, which is weighing on computer memory and storage makers (ASML -3.8%).

Top European News

Spanish GDP Growth Rate QoQ Final (Q4) Q/Q 0.8% vs. Exp. 0.8% (Prev. 0.6%).

Spanish GDP Growth Rate YoY Final (Q4) Y/Y 2.7% vs. Exp. 2.6% (Prev. 2.7%).

German GfK Consumer Confidence (Apr) -28.0 vs. Exp. -26.5 (Prev. -24.7, Low. -32.2, High. -25.6).

Italian Business Confidence (Mar) 88.8 (Prev. 88.5).

Italian Consumer Confidence (Mar) 92.6 (Prev. 97.4).

Trade/Tariffs

Germany reportedly drafts a plan to hit US tech, drug supplies and companies, Bloomberg reported citing sources; officials are mapping vulnerabilities in US supply chains to apply pressure on the US.

China’s Foreign Ministry, on Trump’s China visit announcement for May 14-15th, said the two sides have maintained communication.

China Commerce Ministry will impose an additional 55% tariff on beef imports from Australia after quota threshold reached.

EU’s Dombrovskis said we have received assurances from the US that they intend to honour the trade deal.

US President Trump said Supreme Court ruling on tariffs will cost the US hundreds of millions.

FX

DXY is essentially flat and trades within a narrow 99.56-99.75 range, with price action taking a breather after a string of ceasefire related volatility. Recent reports surrounding the Middle East situation suggests that US President Trump told aides he wants a speedy end to the Iran war and wants to wrap up the conflict in the coming weeks, via WSJ. Elsewhere, Israeli Media reported that US President Trump may announce a ceasefire with Iran by next Saturday. Jobless claims and a slew of Fed speak is due throughout the day.

G10s are incrementally lower against the USD (ex-Antipodeans). Ultimately, subdued price action as markets await updates related to concrete progress on the ceasefire plan, or the risk of another bout of escalation measures. Most recently, Axios reported that Trump is preparing for a massive “final blow” against Iran. Antipodeans are at the bottom of the G10 pile this morning, with the Kiwi underperforming – pressure which follows the broader downbeat risk-tone. EUR/USD trades within a very thin 1.1547-1.1572 range, and ultimately little moved to ECB’s Nagel and de Guindos. Elsewhere, Cable is incrementally lower, as traders await commentary from BoE’s Breeden, Taylor and Greene. Focus will be on the former, given Taylor spoke last week (remained dovish), whilst Greene spoke on Wednesday.

NOK is net-unchanged in the aftermath of the Norges Bank policy announcement, where the Bank kept rates steady at 4% (as expected). There was some volatility at the time, with EUR/NOK moving higher as traders unwound outside bets of a hike. That move since entirely pared. Decision aside, focus was on the MPR and accompanying commentary was hawkish, with the Bank noting that “it will likely be appropriate to raise the policy rate at one of the forthcoming monetary policy meetings”. This was also reflected by the updated MPR, whereby the end-2026 rate is now seen at 4.35% (prev. 3.71%); 2027 was revised higher to 3.98% (prev. 3.31%), and the “terminal rate” was raised to 3.54% (prev. 3.20%).

Fixed Income

Once again, another session dictated by energy movements and the associated implications for prices and yields.

USTs are lower by 12 ticks at most, to a 110-16+ trough. If the move continues, we look to the 110-05+ mark from the 24th, and then the 109-31+ WTD base. Ahead, a handful of data points, numerous Fed speakers and supply features in a relatively busy schedule; however, geopolitics will likely continue to dictate.

Bunds in-fitting. At a 125.30 low, with losses of nearly 70 ticks at most. If the move continues, we look to support at 125.02 and then the 124.77 WTD base. For Europe, newsflow is somewhat limited, with no move to a handful of data points or ECB officials. The region’s docket ahead is a little light, and as such, action will be determined by the above US points and/or Middle East developments.

Gilts took the lead from peers and opened with losses of over 60 ticks before falling another 35 or so to a 87.73 trough. If the move continues, we look to recent bases at 87.06, 86.81 and then the contract low of 85.91. A busy BoE docket today, with Taylor and Greene scheduled; though, we have yet to see anything of pertinence from Breeden.

Commodities

Crude futures gradually edged higher overnight and held onto that strength throughout the European morning, with Brent Jun’26 printing a USD 100.96/bbl peak (vs USD 97.69/bbl low) while WTI May’26 prints a current USD 94.13-90.71/bbl range.

On the geopolitical front, US President Trump reportedly told aides that he wants a speedy end to the war and believes the conflict is in its final stages. Meanwhile, Israeli media reported that Trump may announce a ceasefire with Iran by next Saturday, even without a final agreement, while N12 News separately said the working assumption in Israel is that he could announce a ceasefire as soon as this coming Saturday. More recently, it was reported US Pentagon is reportedly preparing for a massive “final blow” of the Iran war, via Axios.

Spot gold is lower after a two-day recovery, with bullion back under USD 4,450/oz at the time of writing, giving back most of the prior session gains, amid the conflicting US and Iranian statements. Spot gold currently resides in a USD 4,412-4,544/oz range after finding support on Monday at its 200-DMA (4,091.57/oz)

Base metals are also softer, with copper under pressure as investors weigh the inflationary implications of the conflict alongside the risk of weaker global activity and softer demand. 3M LME copper resides in a USD 12,114.00- 12,276.08/t range at the time of writing.

Russian Deputy PM Novak says “we will impose a gasoline export bank if necessary”; has possibility to increase oil production if required, but investment will be needed; is already trading oil without discount, and with a premium in a number of lines.

French Commerce Minister said release of strategic oil reserves to be discussed at G7 minister meeting on Monday.

Japan begins releasing national oil reserves, as expected, according to Kyodo.

Turkish oil tanker was hit by a drone in the Black Sea near Istanbul.

Saudi Arabia’s oil sales to China and India are set to be lower-than-usual levels next month, according to Bloomberg.

Japan is reportedly to lift restrictions on coal-fired power plant operation as an emergency response to the Middle East situation for a one-year limit period, according to the Nikkei.

Philippines suspends electricity market due to Middle East conflict and proposes modified administered pricing by April 1st, cites fuel supply risks and price volatility for the suspension.

Pilbara ports in Australia said they closed the ports of Ashburton, Cape Preston West, Dampier and Varanus Island due to cyclone Narelle.

Central Banks

Norges Bank maintains its rate unchanged at 4.0% as expected; “it will likely be appropriate to raise the policy rate at one of the forthcoming monetary policy meetings”. STANCE. The Committee judges that a tighter monetary policy stance is needed to return inflation to target within a reasonable time horizon. The inflation outlook indicates that an increase in the policy rate will likely be required. The Committee therefore wants to await further information on the prospects for inflation. FUTURE POLICY. The future path of the policy rate will depend on economic developments. If the outlook indicates higher inflation than currently projected, a higher policy rate than currently envisaged may be required.

US Treasury Secretary Bessent said to have discussed ways to recast ties between the Fed and the Treasury in the Bank of England’s image, and praises BoE’s market intervention capabilities, according to FT.

ECB’s de Guindos said the outbreak for the Iran war has made the growth and inflation outlook significantly more uncertain, sharp increase in energy prices poses upside risks for inflation and downside risks for economic growth. ECB is well positioned to navigate this uncertain period.

ECB’s Nagel said the ECB will have enough data by April to determine if they need to act or whether to wait and see.

ECB hopes to look through energy price shock from Iran war and Lagarde said it’s too early to know the impact of the Iran war, while it sees rates steady if shock is temporary but may hike rates twice if energy shock is persistent, according to FT.

BoE’s Breeden (neutral) says firms and workers are likely to have less price and wage bargaining power, so second round effects less likely.

BoJ Governor Ueda said large JGB holding doesn’t make policy adjustments difficult, adds conducting policy to achieve price stability target.

RBA Assistant Governor Kent said the board will set monetary policy to achieve low and stable inflation and full employment. Will continue to assess the countervailing forces operating on the economy. Middle East conflict has tightened financial conditions. The longer the conflict persists, the larger the economic impacts will be.

CNB Minutes (Mar): Ready to tighten policy if core inflation rises, agreed a rate hike is premature now.

UBS expects the Fed to deliver two 25bps cuts in September and December (prev. saw cuts in June and September).

Geopolitics

US Pentagon reportedly prepares for massive “final blow” of Iran war, Axios reported. The Pentagon developing military options for a “final blow” in Iran that could include the use of ground forces and a massive bombing campaign. Options include: Invading or blockading Kharg Island; Invading Larak, an island that helps Iran solidify its control of the Strait of Hormuz; seizing the strategic island of Abu Musa and two smaller islands, which lie near the western entrance to the strait and are controlled by Iran but also claimed by the UAE; Blocking or seizing ships that are exporting Iranian oil on the eastern side of the Hormuz Strait.

Pakistan Foreign Minister says US-Iran indirect talks are taking place through messages being relayed by Pakistan.

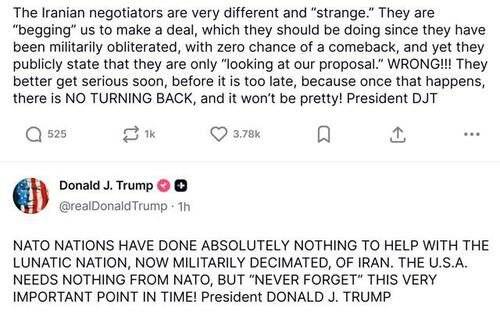

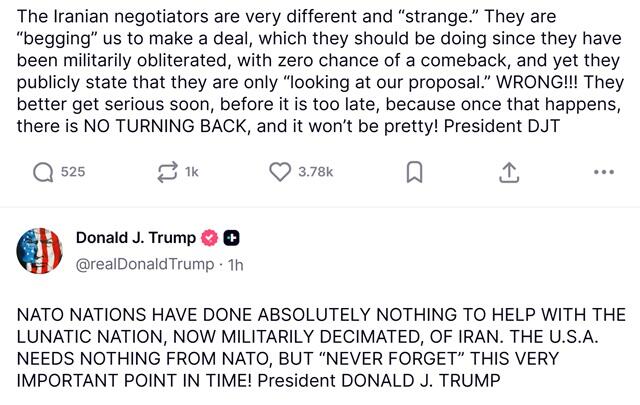

US President Trump says NATO nations have done absolutely nothing to help with Iran.

US Pentagon is considering diverting Ukraine military aid to the Middle East, WaPo reported. Comes as the war in Iran depletes some of the US military’s most critical munitions, according to sources cited.

US President Trump said Iran is negotiating and wants a deal, but is afraid to say so, adds no one in Iran wants to be Supreme Leader right now.

Iran’s Foreign Minister said Iran’s current policy is to continue resistance in the face of ongoing unprovoked American-Israeli aggression while ruling out negotiations and ceasefire in the absence of required guarantees, according to Press TV. Vessels belonging to “friendly countries” including China, Russia, India, Iraq and Pakistan had been allowed to pass through the Strait of Hormuz.

IRGC has reportedly imposed a de facto ‘toll booth’ regime in the Strait of Hormuz, requiring vessels to submit full documentation, obtain clearance codes and accept IRGC-escorted passage through a single controlled corridor, according to Lloyd’s List.

US Central Command said USS Abraham Lincoln aircraft carrier continues to carry out strikes on military targets in Iran, while CENTCOM also said most of the Iranian facilities used to build missiles, drones and warships, are badly damaged or destroyed.

Iranian-linked Handala Hack Group say they have “initiated a new phase of Operation Lockheed Martin (LMT)”, said Co. employees have 48 hours to respond, Mehr News reported.

Pakistani official said Israel took Iran’s Foreign Minister Araghchi and Parliamentary Speaker Ghalibaf off the hit list after Pakistan requested the US not to target them.

Iran targeting an American fuel supplier, according to a report cited by Tasnim.

The IRGC naval commander was eliminated in Bandar Abbas, according to the Jerusalem Post citing an Israeli source.

Hezbollah said it targeted headquarters of Israel’s Ministry of Defense with missiles on Thursday and barracks affiliated with the military intelligence department of Israel’s army in the north of Tel Aviv, was also one of the targets of the operation.

Egypt’s Foreign Minister said Cairo is ready to host talks to support de-escalation between US and Iran, and backs President Trump’s push for negotiations, adding he hopes there will be direct talks between the two sides.

UAE Foreign Minister discussed developments in the region and the repercussions of Iran’s missile attacks on the UAE and brotherly countries in a call with foreign ministers of Pakistan, Britain, Spain, France and Kazakhstan.

Local sources say huge explosions occurred in the Amir Sultan Air Base in Saudi Arabia following drone attacks.

Explosions heard in Iranian cities of Isfahan and Bandar Abbas.

Arab sources report a loud explosion was heard in the capital of the UAE, according to SNN.

Israel’s Ben Gurion airport halts all operations amid Iranian missile barrage, according to Press TV.

Russia’s Kremlin says “we have not lost interest in peace talks”; territory is one issue that has not been settled.

Ukrainian President Zelensky said Ukraine does not see any genuine desire from Russia to end the war.

Russia attacked damaged ports and energy infrastructure in Ukraine’s Odesa region, according to the regional governor.

UK authorises armed forces to board Russian shadow fleet tankers in British waters, according to The Guardian.

US Event Calendar

8:30 am: United States Mar 21 Initial Jobless Claims, est. 210k, prior 205k

8:30 am: United States Mar 14 Continuing Claims, est. 1849k, prior 1857k

4:00 pm: United States Fed’s Cook Speaks on Financial Stability

6:30 pm: United States Fed’s Miran Speaks on Balance Sheet

7:00 pm: United States Fed’s Jefferson Speaks on the US Economy

7:10 pm: United States Fed’s Barr in Moderated Conversation

DB’s Jim Reid concludes the overnight wrap

As we go to press this morning, oil prices are moving higher again, with Brent crude up +1.86% overnight to $104.12/bbl. Several factors are responsible, but a big one is that Iran have continued to reject the messages from the US about some kind of deal, raising questions about whether there is really an off-ramp to the conflict in the days ahead. Indeed, market attention is quickly turning to the end of Trump’s 5-day deadline from Monday, when he said he’d postpone strikes against Iranian power plans and energy infrastructure. So that’s just over 48 hours away now, and multiple outlets have reported that thousands of US troops have been sent to the region. So the prospect of a fresh escalation is still top of mind for investors.

That shift in sentiment has hit global markets this morning, with futures on the S&P 500 (-0.20%) and the DAX (-0.49%) both lower, whilst 10yr Treasury yields (+2.6bps) are back up to 4.36%. Indeed, the 2yr Treasury yield (+3.1bps) is currently at 3.91%, the highest since July. Meanwhile in Asia, the major equity indices have lost ground as well, with the Nikkei (-0.52%), the Hang Seng (-1.43%), CSI 300 (-0.62%), Shanghai Comp (-0.67%) and the KOSPI (-2.70%) all falling back. Moreover, Japanese bond yields have continued to rise, with the 2yr JGB yield (+3.2bps) up to 1.32% this morning, which is the highest it’s been since 1996. So it’s a tough morning across the board.

For markets, the issue is there’s still plenty of doubt about whether a US-Iran deal can be reached, given how Iran have publicly rejected the US on several occasions. So that’s seen markets become increasingly sceptical about positive headlines from the US side, because we haven’t seen similar noises from Iran. For a sense of the difference, it’s been widely reported that the US have a 15-point plan, which includes the dismantling of Iran’s nuclear facilities and reopening the Strait of Hormuz. That hasn’t been confirmed by the White House, but Press Secretary Leavitt said there were elements of truth to the reports. Meanwhile, CNN reported yesterday that Vice President JD Vance might travel to Pakistan this weekend for a meeting to discuss an off-ramp. And White House Press Secretary Leavitt said that the US was engaged in “productive conversations”. So all that suggested some kind of progress towards a ceasefire.

By contrast, we’ve had much more negative rhetoric on the Iranian side. Indeed, oil prices moved higher after Iran’s Fars News cited sources who said the moves by Trump to start indirect talks were illogical and not viable at this stage. Then, Iran’s Press TV cited an official who said Iran would end the war when it chose, and when its conditions were met, including security guarantees and recognition of Iran’s authority over the Strait of Hormuz. Later on, Reuters also reported that Iran has demanded for Lebanon to be involved in any ceasefire, implying an end to Israel’s offensive against Hezbollah. So by the close, that meant Brent crude had risen from $97.30/bbl during the European morning to end the US session at $102.22/bbl, before its latest climb this morning to $104.12/bbl.

Before that, markets had seen a more positive session yesterday when oil prices were lower, as that helped to ease concerns on the extent of any inflation shock. So that led investors to dial back their expectations for rate hikes this year, which in turn helped bonds and equities on both sides of the Atlantic. For the Fed, that meant just 4bps of hikes were priced for this year by the close, down -1.8bps on the day. And for the ECB, the probability of a hike at the next meeting in April came down from 86% to 62% by the close.

For the ECB, that shift in market pricing followed comments from ECB President Lagarde, who said they would “not act before we have sufficient information on the size and persistence of the shock and its propagation”. So that offered some reassurance against an imminent hike, although she also said they were “prepared, if appropriate, to make changes to our policy at any meeting”. Separately, we also had the latest Ifo business climate indicator from Germany, which fell to a 13-month low of 86.4 in March (vs. 86.3 expected). So again, that cemented investor conviction that the European economy was slowing down given the conflict, in line with what the flash PMIs had shown the previous day.

Given all that, sovereign bonds rallied across Europe, with yields on 10yr bunds (-7.0bps), OATs (-10.6bps) and BTPs (-11.6bps) all posting large falls. Moreover, 10yr UK gilts (-11.7bps) saw a decent decline as well, despite some upside surprises in the latest CPI print yesterday. That showed headline CPI remained at +3.0% in February, as expected, but core CPI unexpectedly moved up to +3.2% (vs. +3.1% expected). And in the US it was a similar story, with yields falling back as investors priced in less inflation and fewer rate hikes. So the 2yr yield (-0.4bps) fell to 3.9%, and the 10yr yield (-3.0bps) fell to 4.33%. Interestingly, that also pushed the 2s10s Treasury curve down to 44bps, which is the flattest it’s been since July.

For equities, it was a decent session across the board yesterday too. In the US, the S&P 500 (+0.54%) advanced, and remains on track for its first weekly gain since the strikes began, having risen +1.31% over the three days so far this week. That gain was supported by a decent performance for the Magnificent 7 (+0.78%), whilst small-caps in the Russell 2000 (+1.23%) hit a two-week high. Those moves came as the VIX index (-1.62pts to 25.33) eased to its lowest level since last Thursday. Meanwhile, gold (+0.68%) posted back-to-back gains for the first time in three weeks.

Over in Europe, the STOXX 600 (+1.42%) also did well, posting a third consecutive advance for the first time since the strikes began, taking it up to a one-week high. And that was echoed elsewhere, with the DAX (+1.41%), the CAC 40 (+1.33%) and the FTSE MIB (+1.48%) all posting solid gains.

Looking at the day ahead, data releases include the US weekly initial jobless claims, the Kansas City Fed’s manufacturing index for March, and the Euro Area money supply for February. Central bank speakers include the Fed’s Cook, Miran, Jefferson and Barr, along with the ECB’s de Guindos and Muller, and the BoE’s Breeden, Taylor and Greene.

Tyler Durden

Thu, 03/26/2026 – 08:29

https://www.zerohedge.com/markets/stocks-bonds-slide-ceasfire-hopes-fade

Trump Tells Iran ‘Get Serious’ About Negotiations Or ‘No Turning Back’ As WH Mulls Plans For ‘Final Blow’

Trump Tells Iran ‘Get Serious’ About Negotiations Or ‘No Turning Back’ As WH Mulls Plans For ‘Final Blow’

Summary

White House, Pentagon reviewing options for ‘final blow’ as Trump tells Iranians ‘get serious’ about talks, which they’ve rejected.

Trump said to want ‘speedy end to war’ (WSJ) while at the same time warning Tehran of ‘no turning back’ if it doesn’t negotiate.

Israel says it has killed Alireza Tangsiri, commander of Iran’s Islamic Revolutionary Guard Corps navy.

VP Vance may travel to Pakistan this weekend for potential talks with Iran.

* * *

‘Final Blow’

President Trump on Thursday is on the one hand calling on Iran “to get serious soon” in negotiations with the US “before it is too late” – while on the other he’s said to be mulling plans for a “final blow” in the military campaign. Axios writes that several possibilities are being considered, all which point toward serious escalation and in some cases even ground troops. All but one of the below “final blow” options carry the potential for US to get stuck in Iran for years:

— Seize or blockade Kharg Island (Iran’s main oil export hub).

— Invade/control Larak Island (key to Strait of Hormuz control).

— Take Abu Musa + nearby islands (strategic entrance to the strait).

— Block or seize Iranian oil tankers in the region.

— Launch massive airstrikes on nuclear/energy sites.

— (More extreme) Ground operations inside Iran to secure nuclear material.

Axios elsewhere reminds: “Trump’s five-day pause on strikes against Iranian energy infrastructure expires Saturday, and a dramatic military escalation will grow more likely if no progress is made in diplomatic talks, particularly if the Strait of Hormuz remains closed.”

Negotiations or ‘No Turning Back’

Meanwhile, below are a couple of the latest Iran-related Truth Social posts by President Trump, at a moment Iran has made clear it will reject direct talks until its ‘five conditions’ are met. Iran has said it won’t be “fooled again” and even though Trump has declared ‘success’ and that Iran has been “militarily obliterated, it’s clear that Tehran has serious strategic leverage given its de facto control of the Hormuz Strait.

Trump threatens in all caps that if Iran doesn’t relent then there is “no turning back” – however, the WSJ is at the same time reporting Trump has told aides he wants a speedy end to the war.

“President Trump has told associates in recent days that he wants to avoid a protracted war in Iran and that he hopes to bring the conflict to an end in the coming weeks,” WSJ writes.

The publication continues, “Nearly one month into the war, the president has privately informed advisers he thinks the conflict is in its final stages, urging them to stick to the four-to-six-week timeline he has outlined publicly, according to people familiar with the matter. White House officials planned a mid-May summit with Chinese leader Xi Jinping in Beijing with the expectation that the war would be concluded before the meeting begins, some of the people said.”

And then it states the obvious which should have been known before Operation Epic Fury was launched: “The problem is Trump has no easy options for ending the war, and peace negotiations are at a nascent stage.” Certainly all of the above-mentioned ‘final blow’ options all carry extreme risk of quagmire (which might make the Iraq and Afghan wars easy by comparison). Path to offramp or more massive escalation coming?

Iran War: We are not watching a path to peace

Three warning signs now visible:

1. “Talks” without a ceasefire

2. Expansion to economic choke points

3. Quiet preparation for ground forces

This is how limited wars become global disasters pic.twitter.com/GTTOc4o4YB

— Robert A. Pape (@ProfessorPape) March 26, 2026

IRGC Navy Commander Killed, Says Israel

Israel says one of its air strike has killed Alireza Tangsiri, commander of Iran’s Islamic Revolutionary Guard Corps navy, in another reported top-level death. Defense Minister Israel Katz described the strike was carried out on Wednesday night “in a precise … operation” and targeted other “senior officers of the naval command.” He played a central role in controlling the strategically vital Strait of Hormuz and recently issued direct warnings to Israel and the United States, including threats to close the waterway; however, just like all Iran’s military commanders, he’ll likely soon be replaced.

Overnight and in the last 24 hours, Iran has targeted more key refineries in Saudi Arabia and Kuwait, which Gulf states have described as a “brutal aggression” against the global economy. Gulf Cooperation Council officials said the situation is an “international responsibility,” warning that “what is a threat today will grow” and stressing that oil supply chains must be protected.

Reminder: Israel keeps an ‘assassination list’ and has reportedly removed these two men from it, to leave room for negotiations, apparently. Below: Mohammad-Bagher Ghalibaf and Iranian Foreign Minister Abbas Aragchi

The GCC called for de-escalation, stating their goal is a “diplomatic solution” to end the attacks, at a moment Pakistan, Turkey, and Egypt are said to be seeking mediation to get peace talks off the ground. “Our main message to our partners in the world is to send an international message, a unified message to Iran to stop immediately and unconditionally their attacks against the GCC countries.” They added their objective is not to “destroy” Iran but to build a “good relationship,” warning that “the deterioration of the situation in the Arab Gulf will be a warning that will exceed the Gulf area.”

Casualties in Iran: Iran’s Deputy Health Minister Ali Jafarian said at least 1,937 people have been killed during the war, including 240 women and 212 children. He added that at least 24,800 people have been injured, including around 4,000 women and 1,621 children.

Meanwhile Iran continues to send steady missiles and drones on Israel, with mounting Israeli casualties and much infrastructure, cities, and neighborhoods suffering severe damage.

⚡️ Iranian cluster munition hit in Israel’s Kafr Qasim earlier today pic.twitter.com/jEs6fdK8ON

— War Monitor (@WarMonitors) March 26, 2026

* * *

More headlines and latest developments:

Iranian state TV quoted an anonymous official saying Tehran rejected the plan delivered via Pakistan and will “end the war when it decides to do so and when its own conditions are met”.

Iranian FM: “At present, our policy is the continuation of resistance. We do not intend to negotiate – so far, no negotiations have taken place, and I believe our position is completely principled.”

The White House said the US is “very close to meeting the core objectives in Iran” and warned Donald Trump is prepared to “unleash hell” if Iran does not accept defeat.

Trump said negotiations are under way and claimed Iran wants “to make a deal so badly” but that “they’re afraid to say it, because they figure they’ll be killed by their own people”.

VP Vance may travel to Pakistan this weekend for potential talks with Iran.

Iran has threatened to disrupt the Bab el-Mandeb Strait—the vital Red Sea route connecting the Mediterranean with MENA and Asia—if attacks target its territory or islands.

Iran attacked a power plant in Israel; the state monopoly said there was no infrastructure damage.

Iran said the US and Israel attacked the vicinity of the Bushehr nuclear plant.

Media coverage of potential Kharg Island takeover scenarios has intensified in the past 24 hours.

Iran’s parliament is working on a bill to impose fees on ships in the Strait of Hormuz.

The Israeli military said it carried out a “wide-scale wave of strikes on Iran” this morning.

The Telegraph: Russia has begun arming Iran with drones in the first known transfer of lethal munitions from Moscow to Tehran since the war began.

The United Kingdom is discussing with global partners “a viable plan” to secure maritime traffic in the Strait of Hormuz.

Tyler Durden

Thu, 03/26/2026 – 08:15

Will AI Trigger The Next Great Depression?

Will AI Trigger The Next Great Depression?

Authored by Michael Lebowitz via RealInvestmentAdvice.com,

Our article title is certainly scary. The question we pose has become a hot topic following the release of “The 2028 Global Intelligence Crisis,” by Citrini Research.

While evaluating the impact of AI on the labor market is complex, we can distill both optimistic and pessimistic views into two straightforward questions.

Will AI bring about an era of unmatched prosperity and productivity, freeing workers from monotonous tasks, revitalizing old industries, and creating new and unimaginable ones?

Or will AI displace many white-collar workers faster than the economy can absorb them, triggering a deflationary spiral with consequences that rival the Great Financial Crisis or worse, the Great Depression?

To better understand how AI might affect the labor market and, ultimately, the economy, we review the bleak Citrini article alongside more optimistic rebuttals from Citadel Securities and Bianco Research. The articles and our summaries provide a useful primer on how the labor markets may adjust to the upcoming major technological changes.

The articles we review are linked below.

The 2028 Global Intelligence Crisis – Citrini Research

The 2026 Global Intelligence Crisis – Citadel Securities

An Alternate View of the Post-AI Labor Market – Bianco Research

Citrini: A Warning from the Future

The pessimistic outlook comes from Citrini Research’s recent article, “The 2028 Global Intelligence Crisis.” The author cleverly frames the article as a memo written two years from now, looking back on an economic catastrophe that is already underway. The article is not a prediction. To wit, they start with the following caveat:

What follows is a scenario, not a prediction. This isn’t bear porn or AI doomer fan-fiction. The sole intent of this piece is modeling a scenario that’s been relatively underexplored.

Citrini’s scenario starts with the “opening act,” something that is already in motion: agentic AI is making software cheaper and easier to develop. Citrini writes:

A competent developer working with Claude Code or Codex could now replicate the core functionality of a mid-market SaaS product in weeks,

The Software as a Service (SaaS) industry is based on initial purchase revenue and recurring subscription income. In Citrini’s view, this business model falters in the face of AI, causing wide-ranging effects across the industry.

What makes Citrini’s view concerning is not the impact on software companies and their employees. It is the negative feedback loop rippling through the economy.

AI capability improves, payroll shrinks, spending softens, margins tighten, companies buy more capability, capability improves,…. A negative feedback loop with no natural brake.

Citrini: Act Two- The Intelligence Displacement Spiral

Citrini’s pessimistic outlook extends well beyond the SaaS industry. That is merely the opening act. Act two is what Citrini calls “the intelligence displacement spiral.” This is a self-reinforcing loop in which displaced white-collar workers across many industries are pushed into the gig economy, depressing wages and weighing on economic activity. Bear in mind that wages and employment have a significant impact on consumer spending, which accounts for 70% of GDP. Moreover, the author reminds us that, in their scenario, the new employees- machines- spend “zero” dollars on discretionary goods.

It’s not just joblessness and a faltering economy. The once dependable backstop for the economy — the US government — will be dealing with falling tax revenue amidst already large fiscal deficits, and a significant preexisting debt load. To wit:

The government needs to transfer more money to households at precisely the moment it is collecting less money from them in taxes.

As is typical, the economic struggles will spread to the financial markets. For example, they foresee a large number of software-related private credit defaults, which weigh heavily on insurance companies that invest heavily in these assets. Also consider the mortgage market, with approximately $13 trillion in US mortgage debt, the repayment of which depends on borrowers maintaining their current income. They write:

In 2008, the loans were bad on day one,” Citrini notes. “In 2028, the loans were good on day one. The world just…changed after the loans were written.

They conclude:

As investors, we still have time to assess how much of our portfolios are built upon assumptions that won’t survive the decade. As a society, we still have time to be proactive.

The canary is still alive.

The Rebuttal: Citadel Securities

The first rebuttal we summarize is courtesy of Citadel Securities.

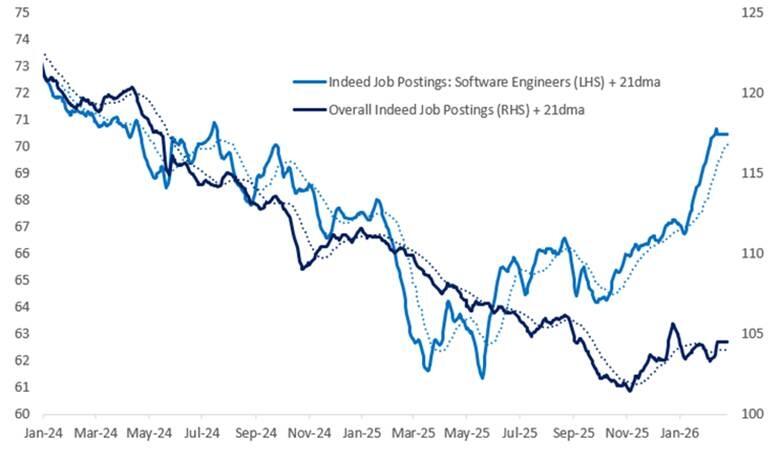

As the title alludes (The 2026 Global Intelligence Crisis), Citadel’s article was clearly motivated by their disagreement with Citrini. They start by directly challenging Citrini’s pessimistic assessment of today’s software job market. The graph below shows that job postings for software engineers are rising, up 11% year-over-year. Furthermore, they state that St. Louis Fed data on AI adoption at work “presents little evidence of any imminent displacement risk.”

Citadel’s core argument is that Citrini is wrong about AI’s recursive potential, specifically the speed and breadth of its spread throughout the economy. To wit:

“Technological diffusion,” or the rate at which a new technology spreads through the economy, has historically followed an “S-curve.”

Essentially, Citadel argues that even if Citrini is right about where AI is eventually headed, the pace of getting there is likely far slower than Citrini assumes — and that slower pace gives the labor market, businesses, and governments time to adapt.

They write:

Markets often extrapolate the acceleration phase linearly, but history implies the pace of adoption plateaus as organizational integration is costly, regulation emerges, and diminishing marginal returns exist in economic deployment.

Citadel also directly challenges Citrini’s macroeconomic logic. They claim:

AI-driven automation is a productivity shock. Productivity shocks are positive supply shocks: they lower marginal costs, expand potential output, and increase real income. They are in isolation disinflationary and growth-enhancing in the medium term.

They support the opinion by noting how steam power, electrification, the internal combustion engine, and, more recently, computing, have followed the “S-curve” pattern. Furthermore, they argue that lower prices due to productivity growth increase consumption.

Defining GDP

They support the argument with the national income accounting identity.

The national income identity states that all spending in the economy (Y) comes from four categories: consumption (C), investment (I), government spending (G), and net exports (X-M –exports minus imports)

Or:

Y = C + I + G + (X − M)

Because this is an identity, it always holds true. Citadel states:

If output rises and real GDP increases then by national income accounting identity something must be rising on the demand side: Consumption, investment, government spending, or net exports must be increasing (more here). A scenario in which productivity surges but aggregate demand collapses while measured output rises violates accounting identities.

More simply, everything produced is ultimately purchased by someone. Consumers (C) buy it, businesses (I) invest in it, the government (G) spends on it, or foreign buyers (X-M) import it. Those are the only four options. If total economic output (Y) is rising — which Citrini’s scenario assumes, since AI is driving a productivity boom — then by definition someone must be doing more buying. You cannot have an economy producing more and selling less at the same time. The basic math and capitalist motives do not allow for it.

Historically, technological revolutions have altered task composition rather than eliminated labor as an input. To produce a negative demand shock large enough to overwhelm output expansion, one must assume near-total automation of economically relevant labor combined with extremely weak redistributive responses. To frame this debate correctly one can simply ask, was the advent of Microsoft office a complement or substitute for office workers? Ex-ante, the concern skewed towards substitution; ex post, it appears a clear complement.

Citadel brings up an important historical note. In 1930, John Maynard Keynes, in his piece “Economic Possibilities For Our Grandchildren,” predicted that rising productivity would reduce the workweek to fifteen hours by the early twenty-first century. He was right about productivity growth but dead wrong about the labor market implications. To wit-“Rather than working dramatically less, societies consumed dramatically more.”

They end by reminding us:

It is also worth recalling that over the past century, successive waves of technological change have not produced runaway exponential growth, nor have they rendered labor obsolete. Instead, they have been just sufficient to keep long-term trend growth in advanced economies near 2%. Today’s secular forces of ageing populations, climate change and deglobalization exert downward pressure on potential growth and productivity, perhaps AI is just enough to offset these headwinds.

Jim Bianco

Jim Bianco’s piece (An Alternate View Of The Post-AI Labor Market), like Citadel’s, is a more optimistic take than Citrini’s article. Bianco approaches the rebuttal from a different angle than Citadel — the nature of business itself.

Bianco writes, “At its core, every business exists to solve a human problem,” calling Citrini’s fatal flaw “the assumption that humanity has a finite number of problems.”

Bianco’s argument leans on Jevons Paradox: when technology makes something more efficient, demand for that thing tends to explode, rather than contract. If AI reduces the cost of drafting a lawsuit to near zero, lawyers do not go home; instead, they file more lawsuits, creating new demand for legal defense and judges.

Bianco also makes a useful distinction between automating parts of a job. He uses GPS as an example. To wit:

When a job is disrupted, the outcome depends entirely on which part is automated. For 150 years, the hard part of driving a London taxi was passing the knowledge test. This involved memorizing 25,000 streets and nearly 20,000 landmarks. This took three or four years, often riding around London on a moped. This knowledge created a scarcity of qualified drivers, allowing them to command a premium wage. GPS automated this scarcity into a free app, flooding the market with new competitors (Uber/Bolt), which flattened wages. Technology took away the hard part of being a taxi driver, making the role less valuable.

Bianco’s “flipside” of less valuable London cab drivers is the story of accountants. Computers eliminated the easy part of accounting, which in turn allowed accountants to provide “more valuable” financial advisory services along with accounting services.

The outcome on the labor market depends on whether AI automates the scarce, high-judgment part of a role or the repetitive overhead.

Bianco believes AI removes the easy, repetitive parts of knowledge work, making workers more valuable. This counters Citrini, who claims it does not matter which part gets automated — if it happens fast enough and at a large enough scale, the labor market cannot absorb the displacement, regardless of whether the remaining work is more interesting.

Bianco closes with what he considers the most critical variable — the speed of transition. He introduces us to a historical parallel, the Engel Pause of the Industrial Revolution.

The Engels Pause: Where Everyone Agrees

The Engels Pause, named after Friedrich Engels, co-author of The Communist Manifesto, describes a harsh fifty-year period from 1790 to 1840. During the Industrial Revolution, this interval was marked by significant job losses that were not immediately offset by new employment. According to Bianco:

That gap between job destruction and job creation sparked a massive collective pushback against capitalism that the world came to know as Communism. Karl Marx directly observed this dangerous dynamic, writing that when an instrument of labor takes the form of a machine, it immediately becomes a competitor of the worker himself.

Citrini’s scenario is, at its core, a modern Engels Pause playing out again, but much more quickly; thus, its immediate impact could be greater. Bianco and Citadel do not deny the transition risk; however, they seem to argue that the gap can be managed if the pace of adoption is measured and institutional responses are timely.

The three authors implicitly agree that if job destruction outpaces job creation for long enough, the political and social consequences could be severe, despite improvements in productivity and corporate profits.

Summary

Technological revolutions have consistently created more jobs than they destroyed. While that statement is 100% true, we must caveat it by describing the transition with the word “EVENTUALLY.” If the AI transition is unbalanced, the negative economic, social, and political ramifications become more worrisome.

From our perspective, the Citrini 2028 scenario is a tail risk and not a base case. That said, we certainly don’t turn a blind eye to their opinion.

To assess the ongoing labor market transition, we will closely monitor economic indicators, including white-collar job openings, real wage growth in knowledge industries, and consumer spending patterns among higher-income households. If those metrics deteriorate simultaneously, the feedback loops Citrini describes could be a force to reckon with.

The canary, Citrini notes, is still alive, but we need to watch it closely.

Tyler Durden

Thu, 03/26/2026 – 08:05

https://www.zerohedge.com/ai/will-ai-trigger-next-great-depression

Western Intel Says Russia Preparing Kamikaze Drone Shipment To Iran

Western Intel Says Russia Preparing Kamikaze Drone Shipment To Iran

A senior Western official told Financial Times reporters that new intelligence indicates Moscow is preparing to ship a batch of kamikaze drones to Iran as part of a broader support package, with the US-Iran conflict nearing the one-month mark.

When asked about the drone shipment, Kremlin spokesperson Dmitry Peskov told FT reporters, “There are a lot of fakes going around right now. One thing is true: we are continuing our dialogue with the Iranian leadership.”

One thing is certain: Iranian forces have launched what reports estimate to be as many as 3,000 drones at US air bases, energy infrastructure, tankers, and neighboring Gulf states that coordinate with US and allied forces.

FT’s report suggests that Iran may need additional drone supplies after an overnight update from Operation Epic Fury, US Central Command Chief Admiral Brad Cooper said Wednesday that US forces had struck their 10,000th target.

“Together, we have struck thousands more, clearly demonstrating that we’re stronger together,” Cooper said.

Cooper said US forces have severely degraded Iran’s missile capabilities and heavily bombarded its missile, drone, and naval production sites. He added that Iran’s drone and missile launch rates have collapsed by 90%, and that two-thirds of its military-industrial base has been destroyed or heavily damaged.

Another Western security official told FT that the type of Russian drones in this month’s upcoming shipment has yet to be determined. The official said Moscow would likely deliver Geran-2 drones, which are basically copycats of the Iranian-designed Shahed-136.

Geran-2 drones

Antonio Giustozzi, a senior research fellow at the Royal United Services Institute, said of the Iranians, “They don’t need more drones. They need better drones. They are after the more advanced capabilities.”

Nicole Grajewski, a professor at Sciences Po University in Paris who focuses on Russia and Iran, noted, “The Russians dramatically improved the Shaheds, including modifications to the engines, navigation, and anti-jamming capabilities. So these systems are already more advanced than the ones Iran was producing domestically.”

Grajewski warned that any new batch of Russian-made drones shipped to Iran could significantly improve the effectiveness of Iranian drone strikes.

Recall that our supply chain report on a crashed Iranian drone found a Russian guidance chip with Western parts in the early days of the conflict. Also, China appears to be making low-cost kamikaze drones for the war (read the report).

Tyler Durden

Thu, 03/26/2026 – 07:45

https://www.zerohedge.com/military/western-intel-says-russia-preparing-drone-shipment-iran

The ‘Blame Game’ In Private Credit Begins

The ‘Blame Game’ In Private Credit Begins

Submitted by QTR’s Fringe Finance

This morning I warned (again) this wasn’t a normal market in private credit. It was a liquidity event. And today it’s becoming something else too.

According to the Financial Times, the SEC is now questioning whether Egan-Jones, a small but deeply embedded credit rating agency in private credit, can “consistently produce credit ratings with integrity.” That’s not a routine inquiry. That’s the regulator openly wondering whether one of the key cogs in the machine was ever doing its job properly in the first place. Think S&P during The Big Short…

And the timing is almost too perfect.

Because just as gates go up, withdrawals get capped, and investors start asking for their money back, the conversation is shifting from “everything is fine” to “who signed off on this?”

That shift matters just as much as the redemptions.

For years, private credit sold stability. It worked because nobody had to test it. As long as money kept coming in and nobody needed to get out all at once, the system held together. You know, kinda like Madoff.

Now people are trying to get out, and suddenly the inputs behind those reassuring return streams — the marks, the models, the ratings — don’t look quite as solid. So naturally, we arrive at the part of the cycle where everyone starts looking around the room for someone else to blame.

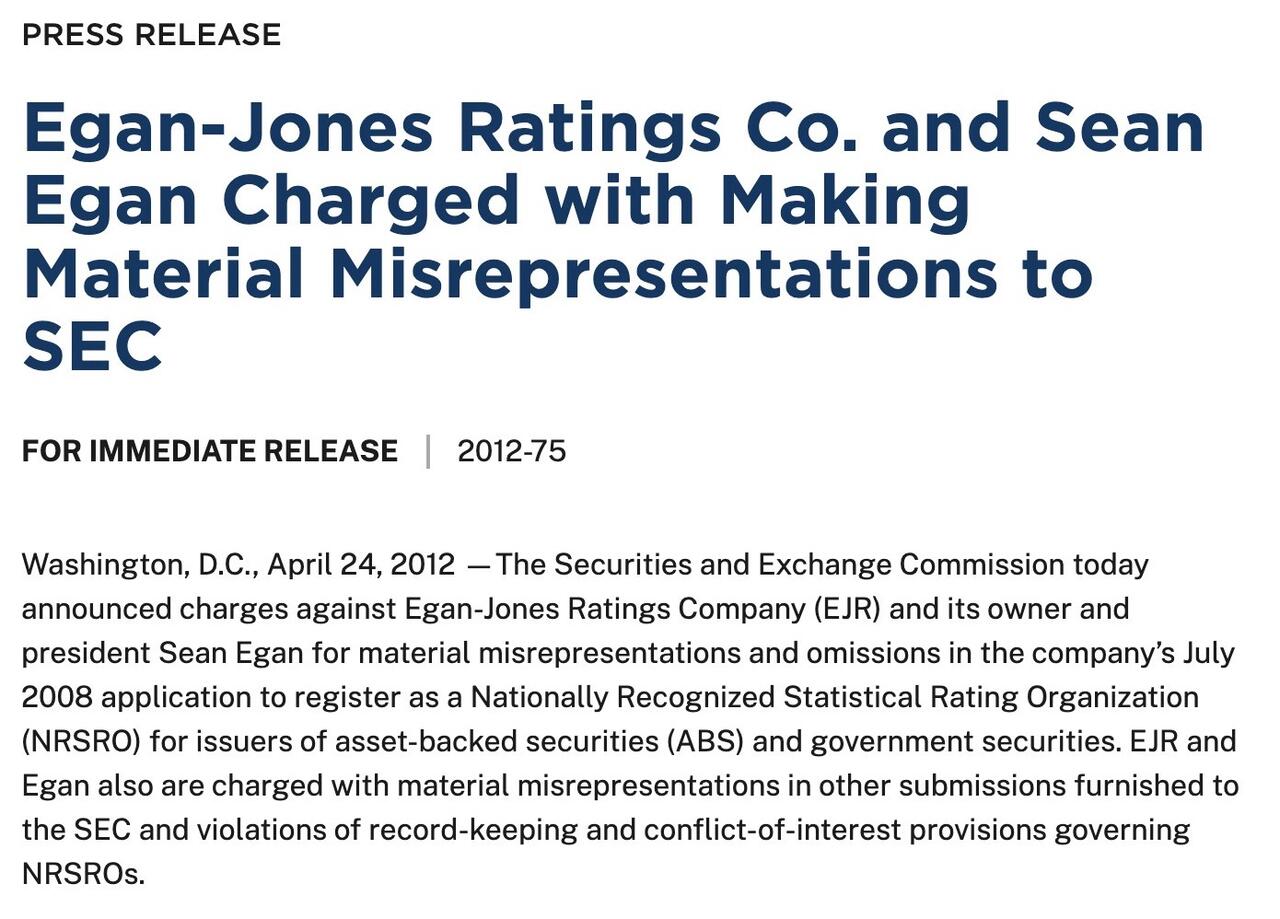

Egan-Jones is an easy place to start. For years, it has faced recurring regulatory scrutiny, primarily from the U.S. SEC, over conflicts of interest, disclosure practices, and internal controls tied to its business model. The most significant action came in 2012, when the SEC charged the firm with misrepresenting its expertise in rating asset-backed securities, resulting in fines and a temporary suspension from rating certain structured products. Ongoing concerns have centered on compliance systems, documentation, and transparency, highlighting tensions between its independent approach and NRSRO regulatory standards.

A small shop with a big footprint, issuing thousands of ratings on private loans that insurers rely on for capital treatment. If those ratings are even slightly generous, or just structurally flawed, then the implications stretch far beyond one firm. It raises the uncomfortable possibility that risk across the system wasn’t just misunderstood, but conveniently packaged to look safer than it was. Again, the analogues to the housing crisis are easy to identify.

And this idea takes hold, it doesn’t stay contained. Managers distance themselves. Investors get louder. Regulators, even reluctant ones, start asking questions they would have preferred not to ask.

Which makes this even more interesting, because this SEC has hardly been spoiling for a fight. In fact, just yesterday news broke that the acting head of enforcement, effectively the agency’s top cop, is stepping down after reportedly pushing for more aggressive action than leadership wanted.

So if this group is starting to publicly question the integrity of ratings in private credit, it’s probably not because they woke up feeling ambitious. It’s because the pressure is getting hard to ignore.

That’s how these things usually go. Not with a bang, but with a slow, reluctant acknowledgment that something underneath the surface isn’t right. Kicking the can down the road continues literally as long as it’s humanly possible.

And now private credit is still a liquidity event, but it’s evolving into a credibility event at the same time. As the blame starts getting handed out, don’t be surprised if a few more “previously respected” pillars of the private credit boom suddenly look a lot less sturdy. The blame game is just getting started and there could be plenty more of it to go around in coming weeks.

Tracking the private credit meltdown:

March 24, 2026 – SEC questions Egan-Jones’ ratings in private credit

March 24, 2026 – Ares restricts withdrawals on its Strategic Income Fund after redemption requests hit 11.6%

March 23, 2026 – Apollo caps withdrawals on its $25 billion Apollo Debt Solutions vehicle after redemptions hit 11%

March 19, 2026 – Stone Ridge’s Alternative Lending Risk Premium Fund gates redemptions after overwhelming redemption requests

March 16, 2026 – Apollo co-president says that “all” marks in parts of the private markets industry are “wrong”

March 11, 2026 – Morgan Stanley and Cliffwater cap redemptions in $8 billion, and $33 billion funds, respectively

March 6, 2026 – BlackRock begins limiting withdrawals from its $26 billion HPS Corporate Lending Fund

March 3, 2026 – Blackstone faces “record” redemptions from its flagship private credit vehicle, investors sought to redeem 7.9% of fund’s $82B in assets

February 19, 2026 – Blue Owl restricts redemptions from its retail private credit fund

January 26, 2026 – Blackrock takes 19% markdowns on TCP Capital Corp.

December 17, 2025 – Blue Owl walks away from $10 billion data center deal for Oracle

October 15, 2025 – QTR warns private credit is one of 10 areas of the market that I would avoid heading into 2026

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Tyler Durden

Thu, 03/26/2026 – 07:20

https://www.zerohedge.com/markets/blame-game-private-credit-begins

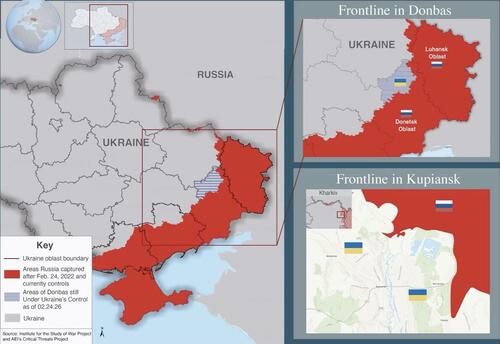

Zelensky: Trump Pressuring Him To Give Up On Donbas And End War Soon

Zelensky: Trump Pressuring Him To Give Up On Donbas And End War Soon

With the Ukraine war now marching into its fifth year, and with the next weather-driven “fighting season” underway, a frustrated Ukrainian President Volydymyr Zelensky says the Trump administration is pressuring him to give up the Donbas region in exchange for US security guarantees. He also claims that Russia is offering to stop providing intelligence to Iran if the United States stops giving intel to Ukraine.

Last week, we reported that trilateral talks about the Ukraine war had been suspended, thanks to the United States now having to focus on executing Trump’s war on Iran with Israel. However, in an interview with Reuters, Zelensky said that Trump is now pressuring Ukraine to cave on its biggest demand just to wipe the war off his to-do list. In his 2024 campaign, Trump told voters that he’d have the war settled “before I even arrive at the Oval Office.”

“The Middle East definitely has an impact on President Trump, and I think on his next steps. President Trump, unfortunately, in my opinion, still chooses a strategy to put more pressure on the Ukrainian side,” he told Reuters. The principal thrust of that pressure: Ukraine giving up on its demand that the eastern Donbas region be returned to Ukraine, in exchange for US security guarantees for what’s left of the Ukraine after the shooting stops. Comprising the Donetsk and Luhansk oblasts, the great majority of the Donbas is already under Russian military control.

“The Americans are prepared to finalize these guarantees at a high level once Ukraine is ready to withdraw from Donbas,” Zelensky said, adding that such a move would leave Ukraine and Europe vulnerable to Russian aggression, because ceding Donbas would also cede key defensive terrain.

Zelensky also bemoaned what he says is an insufficient supply of interceptor missiles for Patriot air defense systems. “We were not stopped from deliveries. I’m very grateful to President Trump, and to his team, but this supply of Patriot missiles is not as large as we need.” That gripe comes as both US and Israeli interceptor missile supplies are being rapidly diminished in responding to wave after wave of Iranian attacks — weeks after White House boasts that Tehran’s ballistic missile capability had been “functionally destroyed.” Meanwhile, Ukraine has apparently come up with an alternative air defense tactic straight out of a video game:

🇺🇦 #Ukraine: Wild footage shows a Ukrainian soldier flying aboard a Yak-52 aircraft, shooting down an incoming Russian Shahed drone with his rifle.

The footage was taken last month, and the location is described as “somewhere in the south,” possibly in Kherson or Zaporizhzhia. pic.twitter.com/uliweMjomj

— POPULAR FRONT (@PopularFront_) March 25, 2026

Zelensky also claimed that his military intelligence had acquired “irrefutable” evidence that Russia is sharing intelligence with Iran, as the country continues to defend itself in the war launched by Israel and the United States on Feb. 28. What’s more, he claimed Putin is using that as a bargaining chip to persuade Trump to acknowledge Russian sovereignty over Donbas:

“I have reports from our intelligence services showing that Russia is doing this and saying: ‘I will not pass on intelligence to Iran if America stops passing intelligence to Ukraine.’ Isn’t that blackmail? Absolutely.”

This latest stirring of the pot by Zelensky comes on the heels of Russia launching the largest 24-hour aerial attack since the Feb 2022 Russian invasion. Counting both drones and cruise missiles, 979 warheads poured into Ukrainian airspace, with about half of them coming in a very rare broad-daylight blitz on Tuesday.

While we can’t verify its authenticity, this video seemingly shows that Trump isn’t the only one who’s unenthusiastic about Zelensky’s pipe dream of retaking the Donbas:

Civilians resist to the military dictatorship in Ukraine.

A man gave a draft officer a ride on the hood of his car, showing him that forcing people to war is wrong.

Zelenskyy made a promotional video for GTA 6 about Ukraine. pic.twitter.com/TseVnR4XPo

— Diana Panchenko 🇺🇦 (@Panchenko_X) March 25, 2026

Tyler Durden

Thu, 03/26/2026 – 06:55

https://www.zerohedge.com/geopolitical/zelensky-trump-pressuring-him-give-donbas-and-end-war-soon

Net Zero Activists Stumped By Shock New Evidence Showing No Link Between CO2 & Temperature Over Last Three Million Years

Net Zero Activists Stumped By Shock New Evidence Showing No Link Between CO2 & Temperature Over Last Three Million Years

Authored by Chris Morrison via DailySceptic.org,

The climate science world (‘settled’ division) is in shock following the discovery in ancient ice cores that levels of carbon dioxide remained stable as the world plunged into an ice age around 2.7 million years ago. Levels of CO2 at around 250 parts per million (ppm) were said to be lower than often assumed with just a 20 ppm movement recorded for the following near three million-year period. In addition, no changes in methane levels were seen in the entire period. Massive decreases in temperature with occasional interglacial rises appear to have occurred without troubling ‘greenhouse’ gas levels, and this revelation has caused near panic in activist circles.