Category: News

Departamento de Justicia admite que jurado no revisó acusación final en caso Comey

Por ERIC TUCKER y MICHAEL KUNZELMAN

ALEXANDRIA, Virginia, EE.UU. (AP) — El Departamento de Justicia reconoció en la corte el miércoles que el jurado especial que acusó al exdirector del FBI James Comey no recibió una copia de la acusación final, una concesión que podría poner aún más en peligro un proceso ya sujeto a múltiples desafíos y demandas de desestimación.

La revelación es la última indicación de una presentación problemática del caso al gran jurado por parte de una fiscal inexperta y nombrada apresuradamente solo unos días antes por el presidente Donald Trump.

Las preocupaciones sobre el proceso surgieron a principios de la semana cuando un juez diferente en el caso dijo que no había registro en la transcripción que había revisado del jurado revisando la acusación que realmente se presentó contra Comey.

Lindsey Halligan, la fiscal estadounidense interina a cargo del caso, declaró bajo interrogatorio que solo el director del jurado y un segundo miembro del panel estuvieron presentes para la entrega de la acusación.

Comey se ha declarado inocente de cargos de hacer una declaración falsa y obstruir al Congreso y ha negado cualquier delito.

El Departamento de Justicia ha negado que la acusación fuera vengativa o selectiva e insiste en que las acusaciones respaldan la acusación.

Trump despidió a Comey como director del FBI en mayo de 2017 mientras Comey supervisaba una investigación del FBI sobre posibles vínculos entre Rusia y la campaña de Trump en 2016. Los dos han estado públicamente enfrentados desde entonces.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

Michael ‘Big Short’ Burry Goes Stealth Mode, Still “Active In Markets”

Michael ‘Big Short’ Burry Goes Stealth Mode, Still “Active In Markets”

Bloomberg’s Claire Ballentine caught up with “Big Short” investor Michael Burry following last week’s news that he had deregistered Scion Asset Management with the Securities and Exchange Commission.

Burry told Ballentine in an email that Scion’s latest iteration functioned essentially as a “friends and family” fund, not a traditional asset-gathering vehicle, and that he wanted to avoid the problems he faced during the original Scion Capital era.

“I didn’t market it or treat it like most do, and I wasn’t trying to grow assets by acquiring investors I didn’t already know. I didn’t want the problems I had the first go around with Scion Capital,” he said.

Burry emphasized that Scion isn’t shutting down, just simply not operating as a registered investment adviser or manager of outside money. He said instead, it will serve as a vehicle for his other investments, adding that he’s relieved to shed regulatory filings that he believes created misunderstandings.

“I am still running my money and active in markets,” Burry noted.

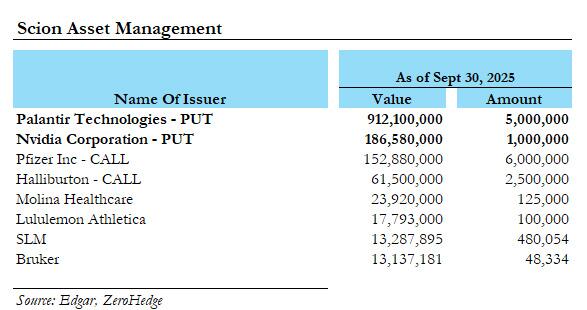

Scion Asset Management’s latest 13F revealed that roughly 80% of its put positions were concentrated in the high-flyers Palantir and Nvidia.

It’s no mystery why Burry wants to hide his trades in secrecy – it only takes one X post to go viral, like this one…

Michael Bury is arguably the worst investor of our generation. Here are 12 of his most smooth brained predictions.

Jan 2017 – Predicted a global financial collapse and WW3 were imminent.

Sep 2019 – Claimed index funds were the next CDOs, ready to implode like 2008.

Dec 2020 –… pic.twitter.com/KyWEyWBe6J

— RJC (@RJCcapital) November 12, 2025

Meanwhile, ‘bearish Burry‘ in 2023.

Burry concluded in the Bloomberg interview, “I am glad to be free of the compliance burden and broad misunderstandings generated by my filings.”

Tyler Durden

Wed, 11/19/2025 – 12:25

https://www.zerohedge.com/markets/michael-big-short-burry-goes-stealth-mode-still-active-markets

Cepal urge a América Latina y el Caribe diversificar mercados para hacer frente a aranceles de EEUU

Por NAYARA BATSCHKE

SANTIAGO (AP) — Los países de América Latina y el Caribe deben apostar por diversificar sus relaciones comerciales y profundizar la integración regional para hacer frente a la nueva política arancelaria de Estados Unidos, alertó el miércoles la Comisión Económica para América Latina y el Caribe (Cepal).

“Enfrentamos un nuevo escenario en plena reconfiguración y que trae aparejada una importante elevación de incertidumbre que nos seguirá acompañando en los próximos años”, dijo el secretario ejecutivo del organismo regional de las Naciones Unidas, José Manuel Salazar-Xirinachs, en una rueda de prensa en Santiago.

En su informe “Perspectivas del Comercio Internacional de América Latina y el Caribe 2025”, el organismo analiza el “profundo giro que ha tenido la política comercial de los Estados Unidos” y su impacto en el comercio global y regional, así como revela las proyecciones para el escenario en 2026, que apuntan a “una marcada desaceleración”.

Aunque en general los países de América Latina y el Caribe están sujetos a aranceles estadounidenses más bajos que las grandes potencias económicas, la situación podría cambiar rápidamente, alertó la Cepal. “En esta coyuntura, los gobiernos de la región deberían diversificar las relaciones comerciales y profundizar la integración económica regional”, agregó.

Según el reporte, las alzas tarifarias aplicadas por Estados Unidos desde el regreso de Donald Trump al poder en enero han incrementado los aranceles para la región en un promedio del 10%. Entre los países, Brasil es el país más afectado, con un arancel promedio del 33%, seguido de Uruguay (20%) y Nicaragua (18%), mientras que México enfrenta una tasa efectiva del 8%.

Si bien indica que el impacto de las subidas ha sido menores que el proyectado a comienzos de año debido a varios factores, como el adelantamiento de importaciones o el dinamismo de los mercados de Asia, la Cepal prevé un deterioro del comercio internacional para 2026, ya que “parece claro que el giro proteccionista que ha tenido la política comercial de los Estados Unidos durante el presente año se mantendrá por lo que resta de la actual Administración”.

En ese sentido, recomienda a los países latinoamericanos y caribeños evitar “medidas reactivas que puedan aumentar la incertidumbre” —que ya se hace sentir en las inversiones directas en la región— e invertir en la diversificación de nuevos mercados, buscando profundizar los intercambios con socios comerciales ya consolidados, como China y la Unión Europea.

Solo en el primer semestre de 2025, los anuncios de proyectos de inversión extranjera directa en la región llegaron a 31.374 millones de dólares, 53% menos que en igual período de 2024 y 37% por debajo del promedio de 2015 a 2024.

“El aumento de los aranceles en los Estados Unidos durante 2025 también ha tenido el efecto indirecto de abrir nuevas oportunidades exportadoras a la región en China”, mientras que “el reforzamiento de los vínculos con la Unión Europea ofrece grandes oportunidades”, señala el informe.

Asimismo, sugiere ahondar las relaciones comerciales y económicas con socios emergentes, como la India, la Asociación de Naciones del Sudeste Asiático (ASEAN), el Consejo de Cooperación del Golfo y la Zona de Libre Comercio Continental Africana, bloques que “ofrecen oportunidades significativas de crecimiento futuro”.

“La recomendación que estamos haciendo no es reducir ni sustituir las exportaciones de los Estados Unidos, sino agregar otros destinos y diversificar”, acotó el secretario general en la conferencia.

El informe indica que el valor de las exportaciones regionales de bienes de América Latina y el Caribe crecerá 5% en 2025, incremento similar al registrado en 2024 (4,5%).

Para este año, la Cepal estima un crecimiento de 2,4% para la región, después de elevar su proyección el pasado octubre. En tanto que para 2026 mantuvo la estimación de crecimiento en 2,3%.

Indígenas y ambientalistas protestan contra construcción de ferrocarril en Amazonía

Por MAURICIO SAVARESE

SAO PAULO (AP) — Mientras Brasil busca mejorar su reputación ambiental convirtiéndose en la sede de la cumbre climática de las Naciones Unidas, una propuesta para construir un ferrocarril a través de Amazonía amenaza con empañar esa imagen en medio de protestas de grupos indígenas y ambientalistas.

El proyecto ferroviario Ferrograo transportaría productos básicos, como maíz y soya, por casi 1.000 kilómetros (621 millas) desde una ciudad en el borde sur de la selva tropical hasta un puerto situado a lo largo de un importante afluente del río Amazonas. Desde allí, los productos serían transportados a un puerto más grande cerca de Belém, la ciudad anfitriona de la conferencia COP30, para su exportación a China y otros socios comerciales.

El gobierno brasileño espera avanzar con el ferrocarril una vez que el Supremo Tribunal del país dictamine sobre la legalidad de cambiar las fronteras de un parque nacional para permitir la construcción y que un organismo de control del Congreso apruebe los planes. Los manifestantes, entre los que se encuentran las poblaciones indígenas potencialmente afectadas, salieron a las calles y ríos de Amazonía este mes para oponerse.

Actualmente, los camiones que transportan soya y maíz a través de la selva tropical deben circular por carreteras que, en algunos lugares, no están pavimentadas, derramando grano que se empuja al costado de la carretera cada día. El ferrocarril propuesto seguiría una ruta similar desde la ciudad de Sinop hasta el puerto de Miritituba, en el río Tapajós, un importante afluente del Amazonas.

En julio de 2023, meses después de que el presidente Luiz Inácio Lula da Silva regresara al cargo, las autoridades locales estimaron que el proyecto ferroviario costaría alrededor de 20.000 millones de reales brasileños (3.800 millones de dólares). Analistas independientes calculan que el costo será un tercio más alto.

Cuando se le preguntó sobre Ferrograo y otros proyectos en el norte de Brasil, donde se encuentra la mayor parte de la zona de Amazonía del país, el ministro de Transporte, Renan Filho, dijo: “No es posible convertirse en uno de los mayores exportadores del mundo sin infraestructura”.

En declaraciones hechas en TV Band, Filho agregó: “Hoy, a diferencia del pasado, el centro de Brasil tiene mucha carga pesada y necesita ser transportada”.

Se esperan nuevas proyecciones el próximo año, cuando el Ministerio de Transporte de Brasil presente estudios ante el organismo de control del Congreso. El gobierno estima que un solo tren de 170 vagones podría reemplazar 422 camiones, reduciendo las emisiones de carbono en la región, según informes de medios locales. Por otro lado, cualquier tala de bosques, sin importar para qué, a menudo genera más desarrollo. Eso sucedió en toda Amazonía, cuando Brasil emprendió importantes proyectos de carreteras en la década de 1970.

Desde su regreso a la presidencia, Lula ha hecho de la reducción de la deforestación en Amazonía una parte central de su agenda y ha logrado importantes avances. Ese esfuerzo parece ir en contra del importante proyecto ferroviario.

Grupos indígenas alzan la voz

Los expertos dicen que existen alrededor de 15 grupos indígenas dispersos a lo largo del camino de Ferrograo y las vías fluviales que conducen a Barcarena, el puerto cerca de Belém donde el grano se carga en barcos para su exportación.

“Los impactos acumulativos (de Ferrograo), que son deforestación, monocultivo y tóxicos, muestran que no basta con comparar emisiones”, dijo en un comunicado Alessandra Munduruku, líder de una población indígena que podría verse afectada por el ferrocarril. Ella y otros activistas afirman que cualquier persona que viva en las cuencas de los ríos Xingu y Tapajós podría perder su hogar a manos de las granjas si el ferrocarril aumenta el transporte y hace que la agricultura sea más lucrativa.

Mariel Nakane, analista de Ferrograo en el Instituto Socioambiental, una organización no lucrativa, dijo a The Associated Press que la administración de Lula ha hecho poco para consultar con los grupos indígenas.

“Esta administración dijo que se acercaría a los indígenas, pero simplemente no lo hizo”, afirmó, agregando que también hubo “cero diálogo” con el predecesor de Lula, el expresidente Jair Bolsonaro.

Las estimaciones del gobierno muestran que el ferrocarril podría transportar hasta 40 millones de toneladas métricas de soya y maíz cada año, duplicando la capacidad actual de la carretera, con la posibilidad de alcanzar 70 millones de toneladas métricas. Pero el daño a los ríos y sus orillas podría alejar a los pueblos indígenas, aumentando aún más las posibilidades para la agricultura y la deforestación, según el Instituto Socioambiental.

El jefe Raoni Metuktire, de 93 años, cuyo pueblo Kayapó sería uno de los más afectados por la construcción del ferrocarril, se unió a más de 300 indígenas y activistas que participaron en una flotilla de barcos que viajaron a Belém para protestar contra el ferrocarril durante la cumbre COP30. Se prevé que la conferencia finalice el viernes.

“Hablé con Lula y (el presidente francés, Emmanuel) Macron para que no perforen petróleo por aquí y no permitan el Ferrograo”, dijo Metuktire a los periodistas en Belém la semana pasada.

Las poblaciones locales cerca de Miritituba dicen que los envíos de soya ya contaminan el agua y causan restricciones en la pesca, efectos que podrían empeorar si un nuevo ferrocarril aumenta el transporte.

Batallas judiciales en curso

Melillo Dinis, abogado del Instituto Kabu, que representa a grupos indígenas, dijo que los opositores a Ferrograo están comprometidos a luchar en los tribunales y mediante acciones administrativas durante el tiempo que sea necesario. Su organización respalda una demanda colectiva contra el gobierno brasileño que busca obtener 1.700 millones de reales brasileños (320 millones de dólares).

“Litigaremos esto, emprenderemos acciones civiles, llevaremos esto a los organismos de control del gobierno y también lucharemos si es necesario en la fase de licenciamiento ambiental”, dijo Dinis a la AP.

El abogado dice que los grupos de protección indígena decidieron sabiamente retirarse de las discusiones del gobierno sobre Ferrograo el año pasado, ya que entendieron que sus recomendaciones no fueron tomadas en serio por las autoridades.

“El diálogo con los indígenas se lleva a cabo en las aldeas, dentro del modelo cultural de cada uno de esos pueblos. Pensaron que una reunión en Brasilia, la capital, debería resolver esto”, dijo Dinis. “Estuvimos allí casi ocho meses. Les ofrecimos 100 páginas con sugerencias. Las ignoraron totalmente”.

___

La cobertura climática y ambiental de The Associated Press recibe apoyo financiero de múltiples fundaciones privadas. La AP es la única responsable de todo el contenido. Encuentra los estándares de la AP para trabajar con organizaciones filantrópicas, una lista de las fundaciones y las áreas de cobertura que financian en AP.org.

___

Esta historia fue traducida del inglés por un editor de AP con la ayuda de una herramienta de inteligencia artificial generativa.

NATO Scrambles Jets Amid One Of Deadliest Russian Attacks On Western Ukraine

NATO Scrambles Jets Amid One Of Deadliest Russian Attacks On Western Ukraine

Russia overnight carried out its typical aerial and drone strikes on Ukraine, but this time escalated attacks in Ukraine’s West, which apparently were close enough to the border to cause alarm in nearby Poland and Romania.

The two NATO member countries scrambled jet fighters in response amid the massive Russian and drone and missile strikes which killed at least 25 people, some of which were reported as children.

Aftermath of strike on Ternopil, Ukraine. via Reuters

Romania’s defense ministry said that during the attacks on Ukraine a Russian drone entered its sovereign airspace. Its military then scrambled two Eurofighters which are part of NATO’s fleet. An additional pair of Romanian F-16s were also sent.

Simultaneously, Polish jets were launched to protect Polish airspace on Wednesday morning. “In connection with the attack by the Russian Federation carrying out strikes on facilities located on the territory of Ukraine, Polish and allied aviation is operating in our airspace,” Poland’s military announced. All of this caused some regional commercial airport closures:

Poland temporarily shut down two airports in its southeast, Rzeszow and Lublin, the Polish Civil Aviation Authority said.

The air hubs were closed to provide freedom for warplanes, the regulator explained.

Russian strikes also focused on Kharkiv, resulting in dozens injured, in the overnight hours. These eastern strikes have become frequent, but large-scale attacks on Western Ukraine are much more rare.

Major direct hit on a residential area captured on video from the early morning hours…

Just look at this.

Ukraine’s Ternopil just this morning.

A Russian missile (Kh-101?) directly hits a residential block.

At least 25 killed, including 3 kids.

And of course, Russian propaganda and Telegram channels are wildly rejoicing in ecstasy. pic.twitter.com/zUB4xNZb4o

— Illia Ponomarenko 🇺🇦 (@IAPonomarenko) November 19, 2025

BBC describes of the carnage, “At least 25 people have been killed including three children in a Russian drone and missile attack on the western city of Ternopil that hit two blocks of flats, Ukrainian rescue officials say.”

“Another 73 people were wounded, 15 of them children, officials said, in one of the deadliest Russian strikes on western Ukraine since Moscow launched a full-scale war in 2022,” the report continues.

The attack comes at a moment of ‘secretive’ US-Russia talks based on a new 28-point peace plan by the Trump White House, but also as Europe is trying to rally bigger, urgent support to Kiev:

Russia is bombing – here, Ternopil.

Europe is watching. pic.twitter.com/DarVWI37UU

— Jürgen Nauditt 🇩🇪🇺🇦 (@jurgen_nauditt) November 19, 2025

The Western cities of Lviv and Ivano-Frankivsk were also hit, which wounded over 30 people, and resulted in buildings and cars destroyed and set ablaze.

Russia is rejecting Ukrainian and European assertions it attacked civilian residencies, instead issuing a statement claiming the targets were military-linked defense industry buildings and energy sites:

“In response to Ukraine’s terrorist attacks on civilian targets in Russia this morning, the Russian armed forces launched a massive strike with long-range, air- and sea-based precision weapons, including hypersonic ballistic Kinzhal missiles and strike drones against the defense industry and energy facilities that supported its operation, as well as against long-range drone depots, located in western Ukrainian regions. The strike targets were achieved, and all designated objects were hit,” the statement read.

These are two ordinary residential buildings in Ternopil. Not military targets, but simply someone’s homes.

This morning Russia struck them, killing at least 10 people and injuring four dozen more, including 12 children.

Russian attacks across the country, from Kharkiv to… pic.twitter.com/U49GZd2kQc

— Andrii Sybiha 🇺🇦 (@andrii_sybiha) November 19, 2025

Ukraine’s air force subsequently said close to 500 drones were sent by Russia in the attacks, and nearly 50 missiles. The statement said it intercepted the majority of them. But the several that got through clearly caused a lot of devastation.

The timing of this could derail the fresh Trump admin efforts to achieve peace in Ukraine. Certainly the hawks in Europe will have more reason to reject any plan seen as offering too much compromise to Moscow.

Tyler Durden

Wed, 11/19/2025 – 11:45

Ucrania pide al Vaticano formalizar mediación para el retorno de ciudadanos retenidos por Rusia

Por NICOLE WINFIELD e ILLIA NOVIKOV

ROMA (AP) — Ucrania ha pedido al Vaticano que formalice su papel facilitando las negociaciones sobre el retorno de niños y civiles ucranianos llevados por Rusia durante la guerra de casi cuatro años, manifestó el miércoles un funcionario del gobierno de Kiev.

El presidente Volodymyr Zelenskyy hizo la solicitud en una carta al papa León XIV antes de una audiencia el viernes entre el pontífice y una delegación de niños y civiles ucranianos que han regresado.

La carta solicitaba que el papa formalizara el acuerdo informal iniciado por el papa Francisco en el que un cardenal italiano, Matteo Zuppi, había servido como enviado papal personal para asuntos humanitarios.

“Para poder lograr más, necesitamos formalizar este proceso en el Vaticano, y por eso esta solicitud ahora se presenta oficialmente”, declaró Iryna Vereshchuk, la subdirectora de la oficina de Zelenskyy.

Dijo a los periodistas en Roma que Ucrania quiere que la Santa Sede actúe como intermediario, o “plataforma”, a través de la cual Ucrania y Rusia pudieran discutir el retorno de civiles.

No está claro si alguno ha sido devuelto a través del canal informal del Vaticano.

Vereshchuk acompañaba a una delegación de niños ucranianos, padres y abuelos que habían vivido en partes de Donetsk controladas u ocupadas por Rusia o que fueron retenidos por fuerzas rusas en otros lugares y que ahora vivían en territorio controlado por Ucrania.

Señaló que bajo la misión de Zuppi, Rusia ha logrado usar una “zona gris” para no responder a las listas de civiles que Ucrania quiere liberar, porque el proceso no estaba formalizado.

“Una vez que el proceso esté formalizado, podremos tener comunicaciones adecuadas con los rusos y cuando presentemos una carta a través de la plataforma, tendrán que responder”, afirmó.

Ni el Vaticano ni la embajada rusa ante la Santa Sede respondieron a las solicitudes de comentarios.

Ucrania dice que sigue documentando miles de casos de niños que fueron llevados ilegalmente al territorio ruso durante la guerra, una práctica que Kiev llama una de las crisis humanitarias más sensibles del conflicto.

La Corte Penal Internacional en 2023 emitió una orden de arresto contra el presidente ruso Vladímir Putin por crímenes de guerra, acusándolo de responsabilidad personal por los secuestros de niños de Ucrania.

Según los datos actuales publicados por la plataforma presidencial de Ucrania “Bring Kids Back”, 19.546 niños ucranianos fueron oficialmente registrados como deportados o transferidos por la fuerza por Rusia.

Informes de medios citando al Defensor del Pueblo de Derechos Humanos de Ucrania, Dmytro Lubinets, dijeron que al 27 de marzo, 1.247 niños habían sido devueltos exitosamente a Ucrania a través de canales diplomáticos y humanitarios.

___________________________________

La cobertura de temas religiosos de la Associated Press cuenta con apoyo de The Conversation US, con fondos de la Lilly Endowment Inc. La AP es la única responsable del contenido.

___________________________________

Novikov contribuyó desde Kiev, Ucrania.

___________________________________

Esta historia fue traducida del inglés por un editor de AP con ayuda de una herramienta de inteligencia artificial generativa.

Column: Smokeout urges smokers to quit the habit

The number of Illinois smokers could continue to shrink if they heed the call on Nov. 20, the date of this year’s Great American Smokeout. But ending tobacco use in Illinois is that proverbial two-edged sword.

Backers of the annual Smokeout say stopping smoking or dipping for a day is the first step toward a tobacco-free life. True enough, yet fewer smokers mean less tobacco tax revenue.

Healthful lifestyles versus smokers helping to balance the state’s precarious financial books is what happens when governments decide to enact sin taxes on cigarettes, or liquor, or gambling. Eventually, more of those “sinners” see the light and quit tobacco use as the government also funds smoke-free programs.

Warnings over the harmful effects of tobacco products in the U.S. began in the 1960s, culminating in 1966 when we became the first nation to require health warnings on cigarette packaging. Back then, tobacco companies would give away free mini-cigarette packs on city street corners and on airlines. GIs will tell you they got tiny packs of usually stale cigarettes in C-ration meal cartons, along with Chiclets or Wrigley chewing gum.

Anti-smoking cautions and warnings about nicotine continued to gain steam through the early 1970s. The Great American Smokeout officially began with the first one held on Nov. 16, 1977. Since then, the third Thursday in November has marked a day devoted to reducing the use of tobacco products and promoting healthy lifestyles.

Data suggests 12% of Lake County residents continue to use tobacco products. There are approximately one million smokers in Illinois, accounting for about 1% of the state’s population. Nationwide, there are an estimated 49 million smokers, close to 20% of American adults, according to the U.S. Centers for Disease Control.

In 2008, Illinois banned smoking inside public buildings, places of employment, governmental buildings, and trains and buses. There was a hue and cry from restaurateurs and bar owners when that occurred, but they now seem to be happy with that law, which curbed at least one vice.

Those remaining Illinois smokers are expected to generate some $30 million in tobacco taxes since the legislature voted to hike the state tax this year. The new taxes took effect on July 1. Tobacco retailers also saw their annual license fees double, going from $75 to $150 per year.

Cigarette taxes in Illinois jumped by $1 per pack, while taxes on vaping products, nicotine pouches and other tobacco products increased to a 45% tax, up from 15%. Cigarettes are subject to a state excise tax of $1.98 per pack of 20. Cigarettes are also subject to the state’s sales tax, about 44 cents per pack.

The average cost of a pack of cigarettes in Illinois is $7.56, depending on where one lives. It is the 12th highest in the U.S. Chicago has an additional $1.18 per pack tax on cigarettes, plus a $3 tax for Cook County, making it one of the most expensive U.S. cities to buy a pack of smokes.

The high cost of cigarettes could give one the impetus to quit smoking during the Great American Smokeout. Healthwise, the transient pleasure of smoking continues to be the leading cause of preventable deaths in the U.S.

While the number of U.S. smokers has declined for decades, smoking cigarettes or cigars can lead to 12 different cancers and increase complications of heart disease, health experts say. Smoking still causes an estimated 480,000 deaths annually.

The American Cancer Society, one of the supporters of the Great American Smokeout, states that cigarette smoking causes about three of every 10 cancer deaths, with the numbers higher in the South and Appalachia. It is believed that secondhand smoke causes nearly 34,000 premature deaths annually.

Those are some grim statistics. Physicians will tell you it’s never too late to quit smoking, which has immediate health effects and even more as we age.

Ex-smokers can testify that kicking the tobacco habit isn’t easy. Some have been known to quit cold turkey; others need a one-day-at-a-time plan with nicotine patches or gum helping them in their anti-smoking quest. Nicotine is an addictive drug.

As part of promoting a healthy lifestyle, the Lake County Health Department supports Tobacco Free Lake County and Lake County Quits, which offer tips and resources to end nicotine addiction. The American Cancer Society also offers support and counseling programs needed to stop smoking.

Quitting tobacco is beneficial at any age, health professionals continue to preach. If you’re a smoker, now is the time to take those first steps.

You’ll thank yourself with improved health and savings in your pocketbook. If you’re ready to take the smoke-out challenge, call Lake County Quits at (847) 377-8090 or go to lakecountyquits.com.

Charles Selle is a former News-Sun reporter, political editor and editor.

sellenews@gmail.com

X @sellenews

https://www.chicagotribune.com/2025/11/19/charles-selle-column-smokeout/

Column: Uncovering the mysteries of the Packers’ ‘Curly’ Lambeau

Only two weeks or so to go, two weeks until the Chicago Bears play the first of this football season’s two games against the Green Bay Packers. These will be the latest chapters in one of the sport’s greatest rivalries, stretching back to Nov. 27, 1921. That is the day of the first meeting of the Bears, then known as the Decatur Staleys, coached by George Halas, who also played in that game, and the Packers, coached by Earl Louis Lambeau, who also played in the game.

The game took place in Wrigley Field: Staleys 20-Packers 0.

Herb Gould was not there, of course, but he was a Chicago Sun-Times sportswriter for four decades, until retiring about a decade ago. During those years, he and his wife Liz regularly spent summer vacations in Door County, that heavily wooded Wisconsin peninsula jutting into Lake Michigan just north of Green Bay. Of course, he knew of the Packers’ history. But Lambeau? Not so much.

“When my wife Liz and I would be out walking or hiking, we would hear people calling their dogs, ‘Here Lambeau,’ ‘Come Lambeau,’” he says. “In time, I learned that he had moved to retire in Door County and that this is where he died. I also realized how little I really knew about this man, and so …”

He knows now, as the author of the deeply detailed and sensationally entertaining biography, “Lambeau: The Epic Life of Earl ‘Curly’ Lambeau, The Man Who Invented The Green Bay Packers” (Gonfalon Press).

At 617 pages, it displays Gould’s energy and curiosity as a researcher. But he was, for a time, a frustrated one. “By all accounts, Curly was a consummate liar,” he told me. “He would lie to your face and he was so good at it that you actually enjoyed it. It was difficult, therefore, to separate the man from the self-constricted myth.”

But Gould is able to give us a colorful portrait of the man who, in the wake of his death at 67 in 1965, compelled George Halas to say, “Without him, pro football simply wouldn’t exist.”

Gould would agree, writing, “In his prime, no one, not even George Halas, had Lambeau’s gift for spotting and developing players. When it came to public relations — to spreading the word about the fledgling NFL — Halas was skilled and dedicated, but Lambeau had a gift. Reporters sought him out in a way that made him the NFL’s most visible ambassador.”

So, what happened? How could such fame and importance fade?

“There is no simple explanation,” Gould writes. “Because the story … is complex. He was a brilliant and innovative sports executive, coach and athlete — a charismatic leader. But he also abused and deceived people who had put their trust in him. And while he was considered charming by women, he also had a troubled history as a womanizer.”

Born and raised in Green Bay, Lambeau was a talented athlete who went on to play for Knute Rockne at Notre Dame until an illness forced him to drop out. He returned to Green Bay where he and a pal founded a team they named the Packers, after the packing company that financed the effort. He was a player and coach, leading the team to championships in 1929, 1930 and 1931. After signing future Hall of Fame receiver Don Hutson in 1935, they won three more titles. He was an innovator, the first to enthusiastically and effectively use the forward pass.

Chicago Bears owner George Halas, left, and Green Bay Packers coach Curly Lambeau on Jan. 23, 1947, at a meeting in Chicago. (Ed Maloney/AP)

He was also a character, and though he would continue professional coaching and win awards (as well as the admiration of Halas) into the 1950s, his later years did not benefit from the ever-increasing popularity and financial boom that came when NFL games began to be broadcast on television.

Told against the backdrop of the times and sensitive to human failings, Gould is a smooth and compelling writer. And the book is attracting praise, such as this from Dan Pompei, acclaimed writer for the Sun-Times and Tribune and currently the senior NFL writer for The Athletic: “(Lambeau) left a massive imprint on the NFL that remains today — yet there is so much we never knew about him. Thanks to Herb Gould, all that changes now.”

Gould and his wife spent most summer vacations in Door County, which has long been a welcoming place for creative people, such as the landscape architect and conservationist Jens Jensen, who designed more than 600 parks (among ours are Columbus, Garfield and Humboldt) and was an ardent preservationist and founder of The Clearing Folk School in the county’s Ellison Bay. That is where Chicago’s Norbert Blei was writer-in-residence for three decades.

Maybe it’s something in the water, for this is Gould’s third book, after “The Run Don’t Count,” a historical novel about the 1908 Chicago Cubs, and “Victory March,” about Notre Dame’s 1988 championship. And there’s another on the way.

Gould and his wife, a lifelong nurse, love their place in Sister Bay but do escape winters for the sun in Tucson. During the summers, though, Herb began covering baseball games of the Door County League for the weekly Door County Pulse newspaper.

“This is what baseball was in the heyday of the minor leagues,” he said. “Before television created giant fan bases radiating from big cities, every town had its team. People took pride in their local guys. That’s what this league is. As embedded as it is in local tradition, it has never seemed like a tourist attraction.”

Until that book is written, the Bears and Packers are on again. The record stands at 107-95-6, and as most Bears fans are painfully aware, 24-3 since 2011. Two weeks or so until the next chapter begins, with games Dec. 7 at Lambeau Field in Green Bay and Dec. 20 here.

Herb Gould, got a prediction?

“The Bears will beat the Packers 20-17 in Green Bay,” he says. “And the Packers will beat the Bears 20-17 in Chicago. … Scribes and touts always favor the home team. But this rivalry is unpredictable.”

rkogan@chicagotribune.com

https://www.chicagotribune.com/2025/11/19/packers-curly-lambeau-book/

“What Has Become Of Us”: Rosie O’Donnell May Have Just Handed Trump A Golden Defamation Lawsuit

“What Has Become Of Us”: Rosie O’Donnell May Have Just Handed Trump A Golden Defamation Lawsuit

I have previously expressed skepticism over some defamation cases against the media brought by President Donald Trump under existing case law. However, comedian Rosie O’Donnell may have supplied the President with a another defamation case if she cannot back up sensational claims made against the President to her 2.9 million TikTok followers. She states as a fact that the President is an “adjudicated rapist” and settled child abuse cases.

O’Donnell seems to spend much of her days in a constant rave about Trump, Republicans, and the demise of the United States from her new home in Ireland. That is fine and an exercise of free speech. However, it may have crossed the line into defamation in her latest posting.

O’Donnell stated:

“Did you think it a million years that they would reelect a man who orchestrated an insurrection against the government? They would reelect that guy with all the charges of sex abuse? — the adjudicated rapist…And then I just saw this thing today about all the cases he’s settled with children, children’s families, accusations about him, that he chose to settle.”

She added:

“When are we going to be able to go, ‘We’re grown up enough to understand that this kind of deviant, psychotic, mentally ill behavior goes on at the highest level sometimes, and no matter where it goes on, it is our duty to stop it,’” O’Donnell continued in her unhinged rant…Shame, people. Shame on what has become of us.”

Notably, at least eleven months ago, O’Donnell called Trump a “rapist” and a “serial pedophile rapist.”

Trump previously sued over the claim that he is a rapist. He lost such a case against E. Jean Carroll after a judge ruled that her claim to have been raped by Trump was “substantially true.” The judge wrote: “The only issue on which the jury did not find in Ms Carroll’s favour was whether she proved that Mr Trump ‘raped’ her within the narrow, technical meaning of that term in the New York penal law.”

Nevertheless, Trump was not legally “adjudicated” to be a rapist. The addition of the word “adjudicated” could move the claim outside of mere opinion.

Even without that word, it is considered potentially defamatory to claim that Trump is, in fact, a rapist despite the earlier ruling in New York. MSNBC and the show “Morning Joe,” for example, quickly retracted a statement that Trump was a “rapist.”

The earlier denial of the defamation case certainly would help O’Donnell, but it is not dispositive. More importantly, that is not all that she said.

The second claim is that Trump settled with the “children’s families” over abuse cases.

It is not clear what the basis for this allegation is, but Reuters reported months ago about fake headlines on the Internet claiming that prosecutors were considering “child molestation charges” against Trump.

It is not clear if O’Donnell can produce support for the claim. If she cannot, it would certainly constitute “per se” defamation.

The common law has long recognized per se categories of defamation where damages are presumed and special damages need not be proven. These include: (1) disparaging a person’s professional character or standing; (2) alleging a person is unchaste; (3) alleging that a person has committed a criminal act or act of moral turpitude; (4) alleging a person has a sexual or loathsome disease; and (5) attacking a person’s business or professional reputation.

Claiming that Trump settled child abuse cases would certainly trigger a couple of these categories.

The United Kingdom is generally a better jurisdiction to bring defamation cases than the United States, which has stronger free speech and free press protections.

In the United States, any such action would have to be brought under the higher standard. In New York Times v. Sullivan, the Supreme Court established the actual malice standard, requiring public officials to shoulder the higher burden of proving defamation. Under that standard, an official would have to show either actual knowledge of its falsity or a reckless disregard of the truth. That standard was later extended to public figures.

If O’Donnell had no credible sources for this claim, it would appear to be clearly a reckless disregard of the truth.

That she said this to millions of followers only magnifies the general damages presumed in such cases.

Unless O’Donnell can argue truth as a defense with credible support for such settlements, she may have just given Trump a golden opportunity to pursue his long-time critic. There is no love lost between these two, but there could soon be a defamation action.

Tyler Durden

Wed, 11/19/2025 – 11:30

Mueren 10 presos de tuberculosis en violenta cárcel de Ecuador

Associated Press

QUITO (AP) — Al menos 10 presos murieron de tuberculosis en la Penitenciaría del Litoral, la cárcel más violenta de Ecuador, informó el miércoles el Ministerio del Interior.

En un breve comunicado, la entidad señaló que todos fallecieron por esa afección crónica, pero que “en este momento se está realizando la autopsia de ley”. Añadió que los presos murieron entre el viernes y el martes pasados.

El Servicio Nacional de Atención a Privados de la Libertad había informado previamente que hasta el 31 de julio se habían registrado 401 presos con tuberculosis en el complejo carcelario al cual pertenece la Penitenciaría del Litoral, en la ciudad de Guayaquil.

La cárcel donde se produjeron los decesos tiene una capacidad instalada para 4.519 reclusos, pero allí se encuentran ubicadas 7.187 personas, de acuerdo con cifras oficiales.

Los decesos se produjeron menos de dos semanas después de la muerte de 31 presos en un enfrentamiento en una cárcel de Machala, en el sur del país.

El organismo carcelario no ha informado la causa de los continuos episodios violentos en las prisiones, aunque autoridades de seguridad aseguraron que se trata de peleas entre bandas rivales.

Desde 2021 Ecuador afronta una creciente espiral de violencia propiciada por bandas delictivas locales aliadas con cárteles transnacionales, según las autoridades.

A inicios de año, la Comisión Interamericana de Derechos Humanos CIDH expresó su preocupación por la “persistencia de graves hechos de violencia ocurridos en las cárceles” y llamó a Ecuador a adoptar medidas para garantizar el derecho a la vida de los presos.

Según ese organismo, entre 2020 y 2024 al menos 591 presos murieron a causa de “la violencia intracarcelaria” y cientos quedaron heridos, entre ellos agentes penitenciarios.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}